Abstract

This paper examines the dynamic relationship between inflation, economic populism, and policy drift in emerging democracies. It argues that inflationary pressures—particularly unexpected inflation shocks—serve as a critical catalyst for the electoral ascension of populist parties by eroding trust in mainstream political actors and amplifying economic grievances among voters. Drawing on established theories and studies of macroeconomic populism with recent empirical evidence from cross-country electoral data, the study demonstrates that inflation surprises are systematically associated with increased vote shares for populist and radical parties. The analysis further highlights how populist electoral success in turn results in short-term market volatility. Government responses, while initially framed as redistributive or growth-enhancing, frequently contribute to policy drift—the gradual misalignment between policy objectives and outcomes due to institutional rigidity, strategic political inaction, or the persistence of outdated policy frameworks. Through comparative case studies of Hungary, India, and Brazil, the paper illustrates how the interaction between inflation and populism reshapes policy trajectories in context-specific ways, reinforcing the view that the long-term consequences of populism are highly contingent on domestic political institutions and economic structures.

Introduction

It is imperative to define the three key terms, ‘inflation’, ‘populism’ and ‘policy drift’ of this working research to understand the further empirical and conceptual relationship.

Inflation is the rate of increase in prices over a given period of time. Inflation is typically a broad measure, such as the overall increase in prices or the increase in the cost of living in a country. It is typically measured by the Consumer Price Index or the CPI. Core consumer inflation examines persistent inflation trends by excluding government-set prices and volatile items like food and energy influenced by seasonal factors. Policymakers closely monitor this measure. Conversely, calculating overall inflation for a country requires a broader index, such as the GDP deflator.

Economic Populism may be seen as an approach to economics that emphasises growth and income redistribution and deemphasises the risks of inflation and deficit finance, external constraints, and the reaction of economic agents to aggressive nonmarket policies. The paradigm of macroeconomic populism is as follows, which also explains why ‘policy drift’ occurs:

- Initial Conditions: The population, along with populist policymakers, is dissatisfied with the economy, believing it can perform better. Past stabilisation efforts have often led to moderate growth, stagnation, or depression. Additionally, uneven income distribution creates significant political and economic challenges, fueling the desire for a radically different economic approach.

- No Constraints: Policymakers reject conservative views on macroeconomic constraints, seeing idle capacity as a chance for expansion. They believe existing reserves and foreign exchange rationing allow for expansive policies without external risks. Traditional concerns about deficit finance are viewed as exaggerated. Populist policymakers argue that expansion isn’t inflationary—due to spare capacity and lower long-run costs—suggesting that spending, even with a fiscal deficit, can benefit the poorest, leading to increased demand and reduced unit costs.

- Policy Prescriptions: in light of the initial conditions described above, the populist programs emphasise three elements: reactivation, redistribution of income, and restructuring of the economy. (Dornbusch, Edwards, 1991)

The Dimensions of Populism

Source: Varieties of populism: Global Strategy Journal, 10(1)

The combined effects of Inflation and Populism lead to ‘policy drift’, the gradual divergence of a policy’s actual outcomes from its original goals, caused by the failure to update its rules or structures to match changing social, economic, or political circumstances, often due to legislative gridlock or strategic inaction by political actors.

How does Inflation lead to the ascension of Populist Parties?

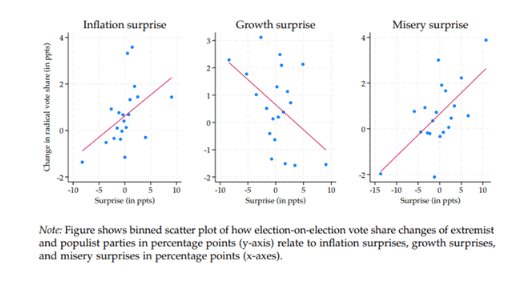

The relationship between inflation and populism is a cycle where each can cause the other, though recent evidence suggests inflation is a primary driver of modern populism. A critical study by Jonathan Federle, Cathrin Mohr, and Moritz Schularick examines just this: whether inflation surprises prompt individuals to turn away from mainstream political parties and vote for parties from the extremist and populist spectrum.

According to the study, the effect of individuals turning away from mainstream political parties and voting for parties from the extremist and populist spectrum is more prominently visible in developed economies such as the UK, France, and Germany during the post-COVID inflation. Furthermore, using a novel long-run cross-country data set spanning 76 years, 18 economies, and 365 elections, they found that the hypothesis is indeed accepted.

Correlation between Electoral Votes and Economic Conditions

Source: Inflation Surprises and Election Outcomes, Federle et al.

The analysis reveals a strong positive correlation between inflation surprises and radical party vote shares, indicating that a one-percentage-point increase in inflation surprises correlates with an approximate 0.174 percentage-point rise in support for radical parties. In column 2, growth surprises show a statistically significant negative correlation; a one-percentage-point positive growth surprise is linked with a 0.244 percentage-point decrease in radical vote shares. Additionally, when examining misery surprises, a notable positive relationship with radical vote shares is found.

These findings suggest that poorer-than-expected economic conditions tend to disadvantage centrist parties while bolstering support for radical alternatives, which often capitalise on economic dissatisfaction and propose drastic reforms. Overall, the data underscores the political ramifications of economic shocks, reflecting the theories within the economic voting literature that hold governments accountable for their economic performance, emphasising the long-term influence of such performance on voting behaviour.

Furthermore, Populist electoral affects financial markets and the economic policies of a country. A 2022 study by A. Hartwell shows Populist electoral success has minimal impact on stock market returns, primarily affecting markets via volatility. Only three countries—France, India, and the Philippines—experienced significant positive returns (with the Philippines seeing increases of 7-8%), though these effects faded quickly. Upon assuming power, returns were muted: Austria saw a slight increase around its populist government’s start, Brazil had dramatic gains of up to 12% following Bolsonaro’s inauguration, while Italy faced declines of 7-8% with the Five Star Movement. In other cases, returns varied but lacked statistical significance. Realised volatility in financial markets appears to be significantly influenced by populist electoral success across various countries, with the notable exception of Poland. The magnitude and nature of this effect vary depending on each country’s unique circumstances. In emerging markets that are accustomed to populist leadership, such as Argentina, volatility tends to rise sharply following populist victories, with notable double-digit increases even ten days post-election. Conversely, countries like Brazil, India, and Italy, as well as Austria, within a one-day window, experience more modest, single-digit increases in revealed volatility. This illustrates the complex relationship between populist political gains and financial stability, highlighting how local contexts shape these dynamics.

Case Studies

By analysing three emerging economies: Hungary, Argentina and Brazil, readers will be able to better understand how economic pressures reshape governance in emerging democracies, particularly how inflation causes populist electoral success, which in turn leads to policy drift. As Hartwell mentions, in long-term the effects of populism are country-dependent and context-dependent.

Hungary

Before 2010, Hungarian politics was dominated by the centre-left Hungarian Socialist Party (MSZP). Hungary was the front-runner in market reforms among the former socialist countries in Central and Eastern Europe, gradually liberalising its economy in the 1980s. Hungary showed relatively rapid growth in terms of GDP per capita between 1995 and 2004. However, since 2005, it has been growing more slowly than its peers. The expansive fiscal policy and the build-up of a large external debt before the worldwide economic crisis in 2008 turned Hungary into one of the most financially vulnerable countries in Europe. Between 2002 and 2010, the general government deficit either exceeded or was close to 5% of GDP. (Valentinyi 2012) It was then that a right-wing populist leader such as Viktor Orban rose to power.

When Fidesz was elected in 2010, the party faced significant challenges. Hungary was reeling from the 2008 global financial crisis, worsened by the 2010 European debt crisis. Although the European Commission, IMF, and World Bank assisted, they imposed strict conditions, leading to a 6.7% drop in GDP and declining living standards in 2009. The new government had to navigate the crisis while adhering to its pledge to avoid austerity.

In consequence, Prime Minister Viktor Orbán approached the European Commission with a request for an increased fiscal space that would allow a budget deficit jump up to 7% to allow the new government to fulfil its electoral promises, especially its tax reduction plans. Just one month after the first official bailout of Greece, however, Jose Manuel Barroso demonstratively declined Orbán’s request, claiming that in the midst of the European debt crisis, there was no room for complacency in the union, and urged the country to speed up fiscal reform (Csaba Citation2022). At the same time, the Commission expressed its concerns about the high public debt ratio (81.3%), the deteriorated net international investment position (−112.5%), and the high rate of unemployment (11%) (European Commission Citation2012).

Enjoying the political support of a large segment of society on the one hand and facing severe constraints on the other hand, Orbán and his cabinet came up with some unconventional fixes. Following the ultimatum Orbán got from Brussels in June 2010, in a rhetorical twist, the cabinet vehemently started to blame the speculative capitalism of the West and imposed extra taxes on certain sectors, including commercial banks, retail, telecommunications, media, and energy. All of these sectors were active in services and were owned mostly by foreigners. The government called on these foreign service providers to take their own part in financing crisis management.

In 2011, Hungary effectively abolished its mandatory private pension scheme, redirecting the assets of private pension funds—approximately 12% of the GDP—into the general budget. This move, executed by the Fidesz government, not only helped reduce the fiscal deficit but also concealed the immediate costs of economic adjustment through what has been termed “invisible” austerity. While the dissolution of the private pension pillar negatively impacted savers, it did not provoke significant public backlash. This lack of resistance could be attributed to a few factors: first, the costs of the pension scheme’s confiscation were not directly felt by individuals, as the impacts were expected in the form of future entitlements. Additionally, many members of the middle class were already grappling with the severe repercussions of foreign-exchange-denominated mortgage loans, which had surged due to the depreciation of the Hungarian currency. By the end of 2011, mortgage loans represented 15% of the GDP, with 70% denominated in foreign currencies, and about 20% of these loans were on the verge of becoming nonperforming. The rising costs of mortgage payments placed significant strain on thousands of families, prompting the Fidesz government to offer a below-market rate for debt repayments.

In its crisis management program, by imposing parts of the costs of austerity on foreign service providers (especially on commercial banks), on the one hand, and sheltering people from the highly negative consequences of the crisis, on the other, Fidesz very knowingly divided the society into two major groups: the “good” people who deserved to be saved by the Orbán cabinet and the corrupt elite (foreigners and their domestic allies, the previous socialist-liberal elite) who were blamed for Hungary’s failed macroeconomic management and all the financial burden that Hungarians had to carry.

Argentina

Argentina used to be among the richest countries in the world, especially in the 1920s. However, due to massive public debt, frequent state bankruptcy, and persistently high inflation, the country has wasted all of its prospects over the course of several decades.

The 2001 crisis, which was marked by collapsing output, soaring poverty, and 40 per cent inflation, produced acute political instability and discredited incumbent governments, creating conditions in which Peronist leaders again mobilised popular support through interventionist and redistributive policies. Néstor Kirchner inherited a broken economy on May 25th, 2003, after a currency crisis and with an increased poverty rate. An ideal situation for a populist government to win over the populace and implement unsustainable policies. The populist governments of Néstor Kirchner (2003 – 2007) and his wife, Cristina F. de Kirchner (2007 – 2015), will henceforth be referred to as the “Kirchner-Kirchner” administration.

The Argentine central bank did not succeed in gaining independence due to the magnitude of the fiscal deficit and the absence of institutional restraints. The treasury would receive an open transfer of liquidity from the central bank. Persistent deficit monetisation expanded the monetary base and established inflationary pressures. This represented a (policy) drift away from the institutional norm of central bank independence toward political control of monetary financing.

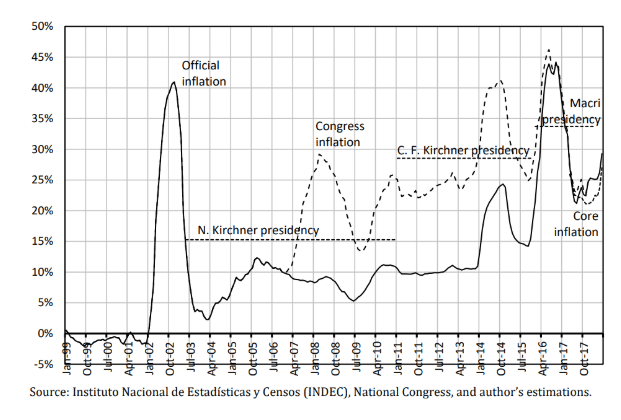

Yearly inflation and average inflation per presidency

Source: The Cost of Populism in Argentina, 2003-2015 (Cachonsky et al.)

A growing trend regarding inflation started in April 2004. Official reports of inflation started to show a downward trend in early 2006. By the end of that same year, people began doubting the authenticity and credibility of the government’s own disclosures and measures. In 2007, there was not only a rise in inflation rates, but also the government began tampering with official inflation rates. There was a whopping difference between the official figures and actual rates, and it could no longer be swept under the rug. While official inflation rates were around 10%, private estimations were more than two times higher.

This manipulation of inflation, poverty, and GDP data aligns closely with the classic macroeconomic-populist pattern described by Dornbusch and Edwards (1991), in which governments dismiss inflationary risks, weaken institutional constraints, and prioritise immediate redistribution.

In 2014, there was a notable spike in both official and private measures. This coincided with the government introducing a new CPI with a broader geographic base. Because private estimates also rose at the same time, Cachanosky (2018) argues that the spike reflected genuine inflation rather than improved measurement, indirectly confirming that earlier official figures had been understated and tampered with. Another rise in inflation occurred in early 2016, just after the Cambiemos coalition took office, but this was not due to its initial policies but because of the delayed effects of a very expansionary monetary policy implemented in the final months of the Kirchner-Kirchner administration. Inflation then fell back toward the levels seen under the Kirchners before beginning to rise again in early 2017, showing how inflationary pressures rooted in earlier populist expansion and weak institutional constraints continued to shape Argentina’s economy even after a change in government.

The Cost of Populism: Long-term governance consequences

Dornbusch and Edwards (1991), in their analysis of numerous populist regimes, found commonalities in the attitudes and disregard of those countries towards macroeconomic policies, all of which frequently result in crises. They came up with a four-phase cycle that applies to most such economies.

The first phase begins with people’s dissatisfaction with high inequality, which gives an opportunity to populists to take over and begin pursuing fiscal expansion and redistribution, often coupled with import substitution and loose monetary policy. At first, everything appears to be in order, and macroeconomic performance and policies are nothing short of successful, proving the populists to be the right choice.

In the second phase, foreign currency becomes scarce, and low inventory levels are unable to keep up with monetary and fiscal expansion. Wages continue to rise despite a notable increase in inflation. The widespread subsidies on wage items and foreign exchange make the budget deficit even worse.

In the third phase, inflation gets out of control, there is capital flight, and the economy slows. In response, populist administrations provide subsidies for travel and food, which erode the nation’s economic position and increase inflation expectations. The government then makes an effort to stabilise through real depreciation and the reduction of subsidies. Policies become uncertain, and real wages drastically decline. The government’s dire circumstances become evident.

In the fourth stage, a new administration assumes power and adopts a more conventional strategy for maintaining economic stability, frequently with assistance from the International Monetary Fund. Wages eventually stabilise at a lower level than they were at the start of the cycle after continuing to decline. However, people lose faith in the new administration and the system as a whole as a result of severe spending cutbacks without significant institutional improvements, which creates the conditions for another cycle of economic issues (Di Tella and MacCulloch, 2009).

Populism also hinders entrepreneurial action by creating regime uncertainty concerning the future stability of the pro-market institutional environment, thereby resulting in entrepreneurs anticipating a rise in transaction costs. However, entrepreneurs residing in nations with stronger checks and balances are less likely to perceive populist discourse as a threat to the future integrity of the pro-market institutional environment, because the power of the populist to pursue their agenda is perceived to be more constrained (Devinney & Hartwell, 2020).

The impact of populism is not purely economic either. Populism often destroys political institutions such as constraints on the executive, checks and balances, the rule of law, and independent bureaucratic agencies.

Conclusion

Inflation, populism, and policy drift are closely connected in emerging democracies. Inflationary pressures weaken confidence in governments and intensify redistributional tensions, making voters more receptive to populist parties that promise rapid relief from rising prices. Extensive literature examining various countries and instances of populist economies shows that such economic pressures often recenter electoral support from centrist parties to populist ones, regardless of whether they are right-wing or left-wing. Financial markets react to their ascension with high volatility and scrutiny, reflecting uncertainty about future economic strategies.

The experiences of Hungary and Argentina illustrate how these political shifts translate into concrete policy choices once populists gain power. These choices led to major institutional and economic crises with high levels of inflation even after the populist regimes ended and new governments took over.

These cases reflect broader findings in political economy research. Expansionary programs built on loose fiscal and monetary policy often lead to macroeconomic successes in the short run but ultimately end up with rising prices, capital flight, and devastating stabilisation efforts in the long run. Such cycles damage trust in public institutions and contribute to repeated political instability. The long-term consequences extend beyond macroeconomic outcomes: erosion of checks and balances, reduced autonomy of regulatory bodies, and uncertainty surrounding property rights discourage investment, particularly where institutional safeguards are limited.

Overall, the evidence highlights the central role of institutions. Where central banks, statistical agencies, courts, and fiscal rules operate with limited independence, inflation-driven populist cycles are more likely to produce lasting policy drift and governance problems. Inflation, therefore, functions not only as an economic indicator but also as a political force that reshapes elections, policy choices, and democratic performance over time.

References:

- Sergei Guriev, Elias Papaioannou. The Political Economy of Populism. Journal of Economic Literature, 2022, 60 (3), pp.753-832. ff10.1257/jel.20201595ff. Ffhal-03874305f

- Kaltwasser, C. R. (2018). Studying the (Economic) “Consequences of Populism.” AEA Papers andProceedings 108: 204–207.

- Cachanosky, Nicolas, The Cost of Populism in Argentina, 2003-2015 (September 14, 2018). 2018. MISES: Interdisciplinary Journal of Philosphy, Law and Economics

- Dornbusch, Rudiger and Sebastián Edwards. (1991a). “The Macroeconomic of Populism,” in Dornbusch, Rudiger and Sebastián Edwards (Eds.), The Macroeconomics of Populism in Latin America (Chicago: University of Chicago Press).

- Bennett, D.L., Boudreaux, C. & Nikolaev, B. Populist discourse and entrepreneurship: The role of political ideology and institutions. J Int Bus Stud 54, 151–181 (2023).

- Devinney, T. M., & Hartwell, C. A. 2020. Varieties of populism. Global Strategy Journal, 10(1): 32–66.

- Di Tella, Rafael, and Robert MacCulloch. 2009. “Why Doesn’t Capitalism Flow to Poor Countries?” Brookings Papers on Economic Activity, 285-321.

Recent Comments