1.Abstract

Credit scoring has long been a foundational tool in financial decision-making, traditionally relying on structured variables such as income, debt ratios, and repayment history to determine creditworthiness. While these conventional statistical models offered transparency and regulatory auditability, they were limited in their ability to capture complex financial behaviour and often excluded individuals and enterprises with thin or non-existent credit histories.

The shift from traditional to modern credit scoring has been driven by advancements in data availability, computing power, and analytical techniques. Artificial Intelligence (AI) and Machine Learning (ML) models now enable the use of alternative data sources, including digital transactions, mobile payments, and online behavioural data. These modern approaches significantly enhance predictive accuracy, optimise credit pricing and limits, and extend credit access to previously underserved populations.

However, this technological evolution is not without shortcomings. Increased model complexity reduces interpretability, posing challenges for regulatory compliance, transparency, and consumer trust. As credit scoring systems become more sophisticated and real-time, ensuring fairness, explainability, and accountability remains a central challenge alongside accuracy and efficiency.

2. Introduction

2.1 Key Components of Traditional Models

Credit reports provided information about the consumer or business’s demographics, insurance, and other utilities. The systematic application of the scoring method contributed to consistency in the credit applications process. Here, we assess some of the most commonly-used methods of credit scoring.

1)FICO Score

A FICO score is one of the most widely used credit scores, ranging from 300 to 850, measuring an individual’s creditworthiness. Developed by the Fair Isaac Corporation, it is calculated using payment history, credit utilisation, length of credit history, and types of credit accounts. This score plays a major role in financial decisions, influencing about 90% of lending decisions in the U.S. The overall FICO score range is between 300 and 850. Credit scores between 670 and 739 are generally seen as “good” by most lenders. In contrast, borrowers in the 580 to 669 range may find it difficult to get financing at attractive rates.

2)Statistical Methods of Credit Scoring:

1. Linear Regression:

Regression analysis is particularly useful in credit scoring because the statistical approach is easy to explain and predict risk parameters. In linear regression, the label (dependent variable or target outcome) is projected on a set of features (covariates or independent variables). Parameters that minimise the sum of squared residuals are chosen.

2. Discriminant Analysis:

Discriminant analysis is a variation of regression analysis used for classification. In default prediction, linear discriminant analysis was the first statistical method applied to systematically explain which firms entered bankruptcy, based on accounting ratios and other financial variables.

The original Altman Z-score model, developed using data of publicly held manufacturers, was as follows:

Z = 1.2X1 + 1.4X2 + 3.3X3 + 0.6X4 + 1.0X5

3. Judgement-Based Models:

Multiple methods may be employed to derive expert judgment-based models. One such method is called the analytic hierarchy process (AHP), which is a structured process for organising and analysing complex decisions. The AHP model is based on the principle that when a decision is required on a given matter, consideration is given to information and factors, which can be represented as an information hierarchy. The decision makers decompose their decision problem into a hierarchical structure of more easily comprehended subproblems, each of which can then be independently analysed.

2.2 Limitations and Pain Points

According to the 2019 Survey of Consumer Finances (SCF), about one-quarter of consumers who desired credit reported that they did not obtain any credit or as much credit as they requested.

A major impediment to obtaining affordable credit is lenders’ reliance on traditional credit scores- specifically, the FICO score and VantageScore-to assess consumers’ creditworthiness. These credit scores affect not only loan approval decisions but also the interest rates consumers pay on their loans.

For instance, traditional credit scores persistently penalise borrowers who have experienced derogatory credit events such as delinquencies, even when those events are no longer indicative of their ability to pay. Traditional credit scores may also disproportionately punish consumers from economically disadvantaged groups, who tend to experience greater difficulties obtaining their first line of credit, as both account age and length of payment history are major factors in the scores.

The trouble with relying on a few variables to represent an individual’s or business’s risk profile is that the universe is far richer, and data related to financial risk may not properly reflect the true risk picture. Traditional models can embed biases that can also ignore emerging borrowers, young borrowers or those in emerging markets, making the process less inclusive. They rely on a rigid set of criteria that might not suit a borrower’s fast-changing financial behaviour. Such information may enable, if accurate risk assessments are possible a lending decision or deny unserviced creditworthy persons access to financial services.

Case Study: Ant Financial (Alibaba Group) and the Failure of Traditional Credit Scoring for Chinese SMEs:

Traditional Chinese financial institutions historically prioritised lending to large, often state-owned enterprises for infrastructure development, neglecting consumers and small and medium enterprises (SMEs). Although SMEs contribute nearly 80% of China’s economic output, they receive only about 20% of bank credit. Limited branch penetration in rural areas and an underdeveloped credit infrastructure- covering only around 300 million individuals, less than 25% of the population- left much of the population underbanked. Rapid technological advancement and widespread smartphone adoption created opportunities for fintech firms to bridge this gap, with over 70% of consumers willing to adopt digital-only banking solutions.

2.3 Evolution Toward Data-Driven Approaches

Unlike traditional models, AI systems can adapt and learn from new data, offering more accurate and dynamic credit assessments. This technology can potentially reduce biases, improve accessibility for underserved groups, and enhance the overall efficiency of risk assessments in the financial sector. The fact that AI can be used in credit scoring also has implications with respect to financial inclusion. Using non-traditional data, AI models can provide firms with a way to assess the creditworthiness of individuals with few or no formal credit history. This expands access to credit for previously underserved populations, particularly in emerging markets.

3. AI Technologies in Credit Scoring

3.1 Machine Learning Algorithms

Machine learning revolutionises credit scoring by analysing diverse data from transaction patterns to digital footprints with superior accuracy. It outperforms traditional models by capturing nonlinear relationships, boosting prediction precision by 15–25%. This enables dynamic risk assessment, slashes approval times, and expands financial access for “thin file” consumers lacking extensive credit histories.

More recently, ensemble learning techniques, such as Random Forests and Gradient Boosting Machines (GBMs), have gained prominence due to their ability to combine multiple classifiers for improved accuracy.

Random forests

Random forests are a combination of tree predictors such that each tree depends on a sample (or subset) of the model development data (or training data) selected at random. Working with multiple subdata sets can help reduce the risk of overfitting. They are ensemble methods for regression and classification problems based on constructing a multitude of decision trees and outputting the class that may be either the mode of the classes (classification) or the mean prediction (regression) of the individual trees.

Gradient boosting

Gradient boosting is an ensemble method for regression and classification problems. It uses regression trees for prediction purposes and builds the model iteratively by fitting a model on the residuals. It generalises by allowing optimisation of an objective function. Different versions of Gradient Boosting, like XGBoost, also help in spotting subtle credit risks. Ultimately, supporting fair lending through tools like SHAP values aligning with regulations.

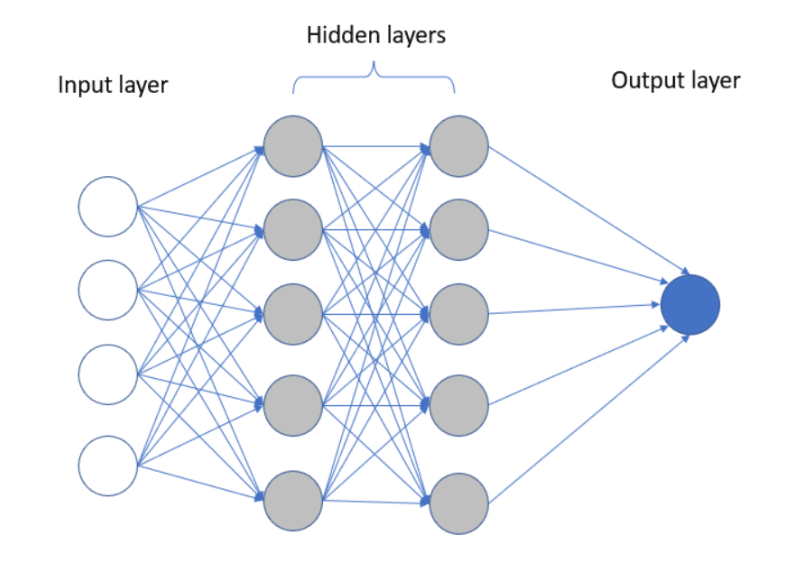

3.2 Deep Learning and Neural Networks

Deep Learning and Neural Networks mimic the human brain to process complex data through interconnected layers of weighted connections. By leveraging deep architectures, these models automatically extract hierarchical features from massive datasets without manual engineering. This enables advanced pattern recognition, such as fraud detection and speech recognition. In finance, they enhance credit scoring accuracy by transforming “messy” digital footprints into precise, data-driven predictions.

Key Components

- Neural Networks: Systems using layers and activation functions for predictions.

- Deep Learning: Advanced ANNs that learn directly from supervised data.

- Applications: Crucial for risk management, image processing, and fraud detection.

3.3 Alternative Data Integration

Alternative data refers to other information, such as news, public opinion, social media platform data and e-commerce data, that is collected and processed by credit investigation agencies and data service agencies and used for credit-granting decisions of lending institutions outside the traditional collection scope of lending information.

Application of Digital Footprint

An important source of alternative data is a customer’s digital footprint. A positive bill payment history could streamline the underwriting process, help more consumers get loans, and potentially lower mortgage rates for borrowers who might otherwise be overcharged.

Assessing Credit Through Social Network Data

Use social data to assess credit by assessing individual social networks with similar credit scores. When predicting loan default, logistic regression analysis is used to find that social media attributes have a significant impact.

3.4 Real-World Examples

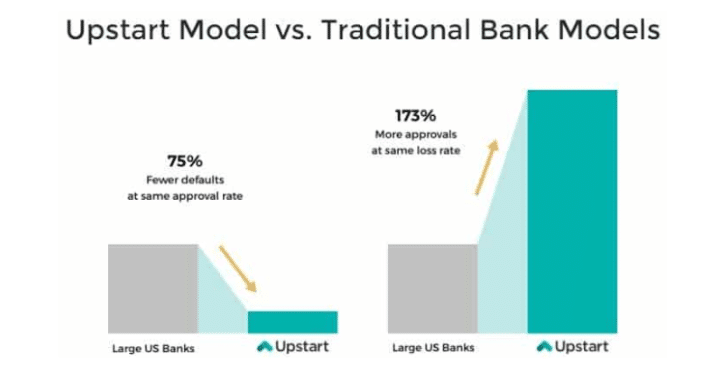

UPSTART

“Traditional credit scores leave people behind. We use artificial intelligence to expand access to reasonably priced credit.” This is how Upstart.com advertises its services to consumers. The company’s website invites visitors to choose from a drop-down menu their personal credit goal (such as refinancing or making a purchase), and to “check your rate.” Instead of narrowing the assessment of a future borrower to FICO-score criteria and past credit history, further variables are taken into account. These alternative data give a richer picture of financial capacity and likelihood to repay a loan, especially for applicants with short credit histories.

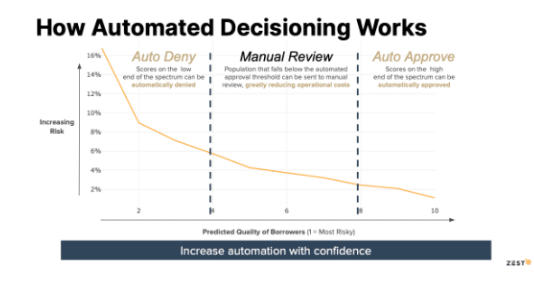

ZEST AI

Zest AI, a fintechcompany, uses machine learning models to integrate non-traditional data sources such as rental payments and education history into credit evaluations. These models have increased credit approval rates for underserved populations while maintaining low default rates. Zest AI has pioneered the integration of alternative data into credit assessments. By using machine learning models, the company includes rental payments, utility bills, and gig economy income in credit evaluations. This approach has significantly increased approval rates for low-income and minority applicants while maintaining low default rates. Their success underscores the potential of technology-driven DEI practices in addressing systemic inequities.

4. Benefits of AI in Credit Scoring

In essence, the advantages of AI in credit appraisal are manifold, offering financial institutions a powerful toolset for accelerating loan processing, improving decision-making accuracy and enhancing risk management strategies.

4.1 Enhanced Predictive Accuracy and Speed

Speed and Efficiency: AI algorithms can analyse vast amounts of borrower data in real-time, processing information from multiple sources simultaneously. This rapid analysis accelerates the credit evaluation process, allowing lenders to make faster lending decisions.

Accuracy and Predictive Power: AI algorithms excel at identifying patterns and relationships in data, enabling them to make more accurate predictions about borrowers’ creditworthiness. This enhanced predictive power enables lenders to assess credit risk more accurately, identify potential defaults and tailor loan terms to individual borrowers’ risk profiles.

Enhanced Risk Management and Decision-Making Processes: AI-powered credit appraisal enables financial institutions to enhance their risk management strategies and optimize their lending portfolios.

4.2 Case Study

JP Morgan Chase: JP Morgan Chase, one of the largest banks in the United States, implemented AI algorithms to improve credit risk assessment and loan underwriting processes. By leveraging machine learning techniques, JP Morgan Chase was able to analyze borrower’s data more efficiently, identify high-risk loans and make more informed lending decisions. As a result, the bank reported a significant reduction in loan defaults and improved overall credit quality.

Capital One: Capital One, a leading financial services company, implemented AI-powered chatbots to streamline the loan application process and improve customers’ experience. By using Natural Language Processing (NLP) algorithms, Capital One’s chatbots can interact with customers in real-time, answer questions about loan products and provide personalised recommendations based on individual financial needs. This AI-driven approach has helped Capital One increase customer satisfaction, reduce loan processing times and enhance overall efficiency.

4.3 Performance Metrics of AI Applications

Recent empirical studies confirm the effectiveness of these approaches. For example, stacked models combining Random Forest, Gradient Boosting, and Extreme Gradient Boosting classifiers have achieved Area Under the Curve (AUC) scores from 0.87 to 0.94, indicating strong predictive performance across datasets. C&R Software’s AI-driven credit risk solutions exemplify this integrated approach, leveraging heterogeneous data sources and advanced algorithms to provide accurate borrower assessments. This enables lenders to tailor credit products responsively, balancing growth opportunities with sound risk management. AI accelerates every stage of credit assessment by automating data capture, verification, and analysis, enabling onboarding to be up to 90% faster. What once took loan officers hours-or even days-to complete now happens in minutes. Practical results include lenders achieving up to 90% accuracy in credit decisions, significantly reducing errors that lead to poor approvals or missed good customers. Continuous learning from new data helps AI models adapt, enabling one bank to reduce approval steps from nine to four while maintaining rigorous risk controls and accelerating decision speed.

5. Challenges and Risks

5.1 Algorithmic Bias and Fairness Issues

Although AI-based credit models are improving predictive performance, they are increasingly criticised for producing biased outcomes that often disadvantage marginalised or protected groups. This may occur due to biased training data, unbalanced feature engineering, or model optimisation techniques that ignore fairness metrics.

While advanced models like XG Boost and Random Forests demonstrate superior predictive performance, they also pose heightened risks of algorithmic bias, particularly in disparate-impact metrics and reduced fairness scores. The regression analysis reinforces the dominant influence of variables such as credit history, loan amount, and employment status on credit decisions, yet also flags the problematic nature of other attributes (e.g., foreign worker status) that could inadvertently introduce discriminatory outcomes.

Thus, the need for a multi-dimensional AI governance strategy, one that encompasses not only performance optimisation but also fairness calibration, explainability enhancement, and continuous model auditing. As financial institutions accelerate their adoption of AI, responsible innovation must become a cornerstone of model design and deployment. Without such integration, the promise of AI in credit risk modelling may be undermined by unintentional harm, regulatory pushback, and erosion of consumer trust.

Components of algorithmic bias

5.2 Data Privacy and Regulatory Compliance

AI-driven credit scoring systems have been implicated in high-profile data security incidents, underscoring their vulnerability to cyber threats. The 2017 Equifax data breach, which compromised the personal information of approximately 147.9 million individuals, exemplifies the risks associated with centralised data repositories. Similarly, the 2022 Equifax credit score error, which resulted in millions of consumers receiving incorrect credit assessments due to a system malfunction, highlights the potential for AI-driven financial models to generate widespread inaccuracies with severe consequences for individuals.

These cases emphasise the urgent need for stringent cybersecurity measures to protect consumer information and uphold the integrity of AI-driven credit evaluations. To address these challenges, regulatory frameworks have been implemented to enforce stringent data protection measures. Legislation such as the European Union’s General Data Protection Regulation (GDPR) and the California Consumer Privacy Act (CCPA) grants individuals’ rights over their personal information, requiring financial institutions to obtain explicit consent from individuals to mitigate heightened risks of data breaches, unauthorised access, and potential misuse.

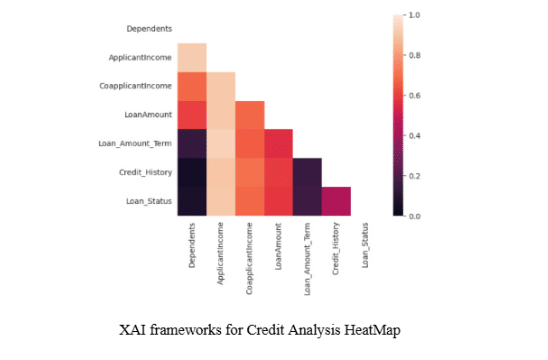

5.3 Explainability and the Black-Box Problem

Models for credit scoring based on AI frequently operate as “black boxes.” This implies that their processes of making decisions are not transparent and hard to understand. The lack of clear explanations from many high-performing ML models for loan approvals or rejections complicates banks’ ability to justify these decisions to regulators, auditors, and consumers. This absence of transparency gives rise to major ethical, regulatory, and trust-related issues.

To tackle these issues, there is an urgent requirement for Explainable AI (XAI) solutions that improve transparency, offer justifiable decision-making insights, and guarantee adherence to financial regulations. Financial institutions can connect AI-driven automation with the need for credit scoring models that are interpretable, ethical, and trustworthy by incorporating XAI techniques.

XAI frameworks for Credit Analysis HeatMap

6. Future Directions and Innovations

6.1 Explainable AI (XAI) Techniques

Explainable Artificial Intelligence (XAI) refers to methods that make machine-learning model outputs interpretable and understandable to human users. It is a core component of the Fairness, Accountability, and Transparency (FAT) framework, particularly relevant for complex models such as deep learning. XAI helps organisations build trust by revealing how models reach decisions and by identifying potential biases or errors.

- Improved decision-making: Explainable AI enhances decision-making by revealing key factors driving model predictions, enabling stakeholders to identify, evaluate, and prioritise actions most likely to achieve desired outcomes.

- Increased trust and acceptance: Explainable AI builds trust by making model decisions transparent, overcoming the opacity of traditional systems, and enabling wider adoption and effective deployment of machine learning across diverse domains.

- Reduced risks and liabilities: XAI reduces risks and liabilities by enabling regulatory compliance, ethical accountability, and auditability, thereby mitigating adverse impacts of machine learning across diverse applications and domains.

6.2 Potential for Real-Time Scoring

Real-time credit scoring and risk analysis play a crucial role in ensuring accurate lending decisions in modern financial platforms, particularly with the growing adoption of alternative financing models like Buy Now, Pay Later (BNPL). However, traditional credit scoring models often fall short because they rely on static historical financial data, which limits their effectiveness for individuals with little or no credit history and reduces responsiveness to evolving borrower behaviour.

6.3 Research Gaps and Recommendations

Implementing Strong Security Measures: Financial institutions must adopt advanced security protocols to protect customer data from breaches and unauthorised access. Regular audits and compliance checks should be conducted to ensure adherence to data protection regulations.

Enhancing Transparency: Clear communication regarding data collection and usage is essential for building customer trust. Banks should provide accessible privacy policies and obtain informed consent from customers regarding data utilisation.

7. Conclusion

Traditional credit scoring relies on structured variables like income and payment history, often excluding “thin file” consumers. Legacy systems provide transparency but struggle to capture complex patterns, leading to rigid assessments that can penalise borrowers for past delinquencies. This reliance on limited data leaves significant populations, such as SMEs in China, without adequate credit access.

Modern AI models solve these gaps by analysing “alternative data,” including digital footprints and social patterns. Techniques like Random Forests and Deep Learning enable dynamic risk assessment, boosting accuracy by 15–25% and accelerating onboarding by up to 90%. Institutions like JP Morgan Chase use these tools to reduce defaults and improve decision-making speed from days to minutes.

However, AI introduces challenges regarding “black-box” interpretability and algorithmic bias. Models may unintentionally disadvantage marginalised groups, necessitating a shift toward Explainable AI (XAI) to ensure transparency and regulatory compliance. Ultimately, the future of credit scoring depends on balancing these advanced predictive capabilities with robust governance and ethical accountability to maintain consumer trust.

8. References

- View of explainable AI in credit scoring: Improving transparency in loan decisions. Available at: https://jisem-journal.com/index.php/journal/article/view/4437/2059 (Accessed: 25 January 2026).

- IJRPR. Available at: https://ijrpr.com/uploads/V5ISSUE11/IJRPR35705.pdf (Accessed: 24 January 2026).

- Katja Langenbucher and Patrick Corcoran. Available at: https://pdfs.semanticscholar.org/ed77/860177ab254b7e03e2c0cf0a8b243c36bb5c.pdf (Accessed: 24 January 2026).

- Abstract—credit scoring is a crucial phase in the risk management process of. Available at: https://www.joebm.com/vol7/588-DE2009.pdf (Accessed: 24 January 2026).

- 12 January – March, 2024 the Journal of Indian Institute of Banking & Finance. Available at: https://iibf.org.in/documents/BankQuest/Jan-Mar2024/2.pdf (Accessed: 24 January 2026).(PDF) AI-driven risk assessment models: Revolutionizing credit scoring and default prediction. Available at: https://www.researchgate.net/publication/385074551_AI-Driven_Risk_Assessment_Models_Revolutionizing_Credit_Scoring_and_Default_Prediction (Accessed: 24 January 2026)

- Access to affordable credit is vital to consumers’ economic … Available at: https://www.kansascityfed.org/Economic%20Review/documents/9602/EconomicReviewV108N3Toh.pdf (Accessed: 24 January 2026).

- 19, K.R.J. et al. Ai credit scoring boosts lending accuracy by 85%: New Industry Study, Digital Acceleration Company. Available at: https://www.netguru.com/blog/ai-credit-scoring (Accessed: 25 January 2026).

- StanMoskovtsev (2024) Alibaba is disrupting a traditional financial services industry in China., Technology and Operations Management. Available at: https://d3.harvard.edu/platform-rctom/submission/alibaba-is-disrupting-a-traditional-financial-services-industry-in-china/ (Accessed: 24 January 2026).

Recent Comments