1. Abstract

Disclosures about Corporate Governance have come to represent an important factor for building investor confidence, especially in developing countries whose Institutional Frameworks are often weak. This paper examines how the clarity and quality of corporate governance disclosures made by companies in developing countries affect investor trust and the inflow of capital into equity and debt markets. Drawing upon Agency Theory and Signalling Theory, this research will explore the mechanisms through which corporate governance practices affect the way investors behave. Through Case Study Research of India, Brazil, and South Africa, this research will examine how changes in governance standards and disclosure practices have affected Foreign Direct Investment (FDI), Portfolio Flows, and Bond Market Dynamics. This research found that increased governance transparency, while reducing information asymmetry, reduced investor perceptions of risk, leading to more stable, longer-term capital inflows. This research provides policy recommendations for Regulators and Firms to improve Disclosure Standards and Build Investor Confidence during times of Volatility in Financial Markets.

2. Introduction

The changing environment of Global Finance has transformed Corporate Governance into one of the most important determinants of long-term economic sustainability and investor engagement. Formal Communications by Firms describing their Internal Controls, Board Structures, Risk Management Policies and Ethical Standards are key indicators to Investors about the integrity and responsibility of Firms’ Leadership. These types of formal communications are commonplace in Developed Countries, however, in Developing Countries; they provide a more complex challenge and opportunity.

Developing Countries experience high levels of Economic Growth and High Levels of Institutional Volatility; therefore face challenges including Regulatory Gaps, Political Instability, and Opaque Business Practices. As such, Disclosures of Corporate Governance can either Bridge or widen the Trust Deficit between Firms and Investors. Good Governance Practices Reduce Information Asymmetry, Mitigate Agency Conflicts, and Enhance Investor Protection. These factors are more relevant in Countries where Legal Enforcement is Inconsistent or Underdeveloped.

This research is intended to investigate the impact of corporate governance disclosures on investor trust and capital flows in equity and debt markets between emerging economies. By analysing cross-country data sets and case studies, based on India, Brazil and South Africa, the research attempts to determine patterns by which governance transparency affects investor behaviour, market performance and access to capital. The nature of this relationship is further interrogated with the theoretical underpinnings of the relationship, with the application of agency theory and signalling theory to contextualise the empirical findings.

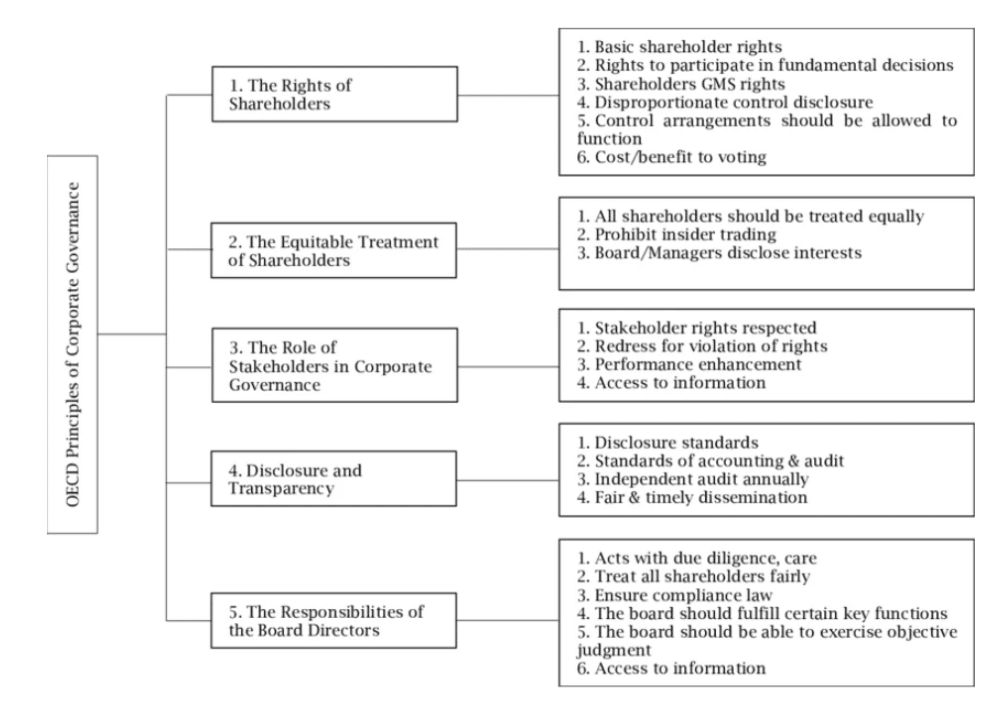

Figure 1. OECD corporate governance framework and stakeholder relationships.

Source: Adapted from OECD Principles of Corporate Governance.

3. Literature Review

The relationship between corporate governance disclosures and investor behaviour has been at the centre of the debate within financial literature, particularly in the context of emerging markets. Corporate governance disclosures are widely recognised as mechanisms to cure the problem of information asymmetry between firms and investors, thereby complementing transparency and accountability (Bushman, Chen, Engel, & Smith, 2004). In jurisdictions where regulatory enforcement tends to be heterogeneous, these disclosures are important signalling devices as to managerial integrity and institutional reliability.

La Porta, Lopez-Silanes, and Shleifer (1999) argue that strong investor protection laws and effective legal enforcement significantly promote financial development and attract external capital; this is particularly relevant in emerging markets, where voluntary governance disclosures can compensate for weak institutional frameworks by providing credible information on firms’ operations and risk management practices. The following can be further understood as:-

- Governance Transparency and Firm Valuation

Empirical evidence suggests a positive association between governance transparency and firm valuation. Klapper and Love (2004) examined firms across fourteen emerging markets and found that:

- Well-governed firms exhibit higher market valuation.

- Such firms demonstrate superior profitability.

- Governance disclosures significantly influence investor perception and capital allocation decisions.

Within the context of the debt market, Bhojraj and Sengupta (2003) found that improved governance structures for companies result in lower bond yields and better credit ratings, as evidence that governance disclosures are not just influential in the equity market, but also in the risk assessments made by debt holders and rating agencies.

- Governance Quality and Debt Market Outcomes

Governance structures extend their influence beyond equity markets into debt markets.

Bhojraj and Sengupta (2003) reported that:

- Firms with stronger governance mechanisms experience lower bond yields.

- Improved governance is associated with better credit ratings.

- Governance disclosures play a critical role in the risk assessment frameworks of debt holders and rating agencies.

- Emergence of ESG Considerations in Investment Decisions

Recent scholarship highlights the increasing integration of Environmental, Social, and Governance (ESG) factors into investment analysis. According to the Organisation for Economic Co-operation and Development (2022):

- Institutional investors are progressively incorporating ESG disclosures into risk assessment models.

- This trend is particularly pronounced in emerging markets, where traditional financial metrics may be less reliable.

- The growing reliance on non-financial disclosures reflects a broader shift toward securing sustainable, long-term capital.

Overall, there is a body of literature that attests to the importance of governance disclosures as a key component of investor decision-making in emerging markets. They also act as instruments of transparency rather than instruments of strategic adjustment aimed at enhancing trust and attracting capital in institutional uncertain environments.

4. Theoretical Framework

This study builds on two main theoretical frameworks that will be used to explain the mechanisms by which governance disclosures affect investor trust and capital flows in emerging market economies.

Agency theory (Jensen & Meckling, 1976) suggests that conflicts between agents and principals are created when their interests are not aligned. In emerging markets, where the legal enforcement mechanisms are often weak, governance disclosures are a way to reduce agency costs by signalling managerial accountability and transparency.

Signalling theory (Spence, 1973) proposes that companies use disclosures to express the quality and thus reduce the asymmetry of information. Markets where there may not be adequate investor protection provided by formal institutions.

5.Methodology

This study uses a mixed-method approach combining qualitative analysis of cases and quantitative interpretation of data. The qualitative component focuses on governance disclosure practices in three emerging markets: India, Brazil, and South Africa, which were selected on the basis of their differing regulatory environment and the availability of governance data in the public domain.

Quantitative analysis uses secondary data from the World Bank, IMF and OECD databases. Key indicators are: governance scores, foreign direct investment (FDI) inflows, bond yields and equity market performance from 2015 to 2025. The data are visualised using line charts, scatter plots and bar graphs to determine trends and correlations between governance disclosures and the capital flows.

This dual approach helps to understand in detail the impact of governance transparency on investor trust and financial market behaviour in different institutional contexts.

6. Case Studies

India: Regulatory Reforms & Foreign Portfolio Investment

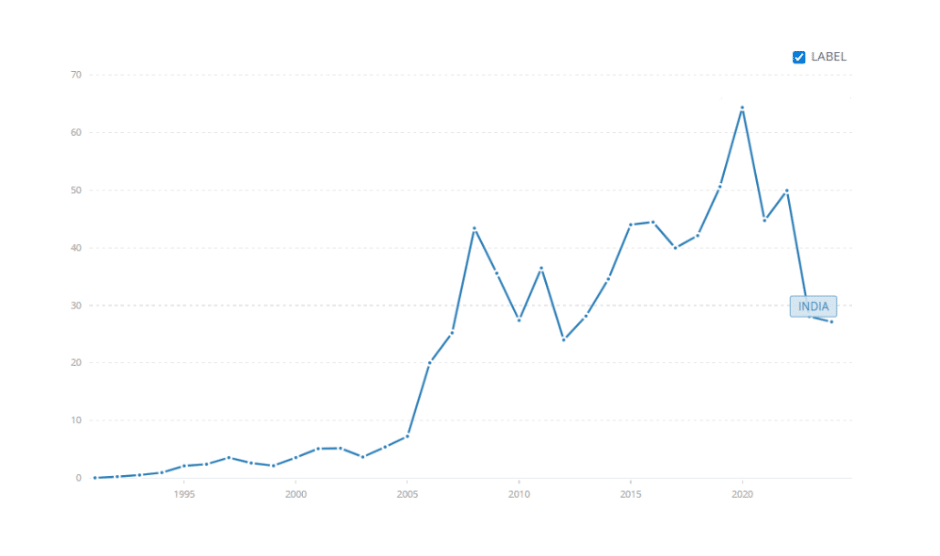

India has enacted several reforms in its governance structures that are aimed at improving corporate transparency and investor protection. It is interesting to note that Clause 49 of the SEBI Listing Agreement and the Companies Act of 2013 provided for disclosures by the board, independent directors, and risk management reporting. These reforms were intended to bring Indian corporate practices into line with international best practices, as well as to address the opacity that had led to foreign investors being deterred from investing in India.

With these changes in regulations, India saw a great surge in foreign portfolio investment (FPI), especially in sectors having high levels of disclosure compliance. According to the data from SEBI and the World Bank, the inflow of FPIs has increased from around $20 billion in 2013 to more than $40 billion by 2021. This trend implies that improved governance disclosures made a significant contribution to the increased investor confidence, particularly for institutional investors who were looking for transparency in emerging markets.

Figure 2. Foreign direct investment inflows in emerging markets- India.

Source: World Bank World Development Indicators.

Foreign direct investment, net inflows (BoP, current US$) – India | Data

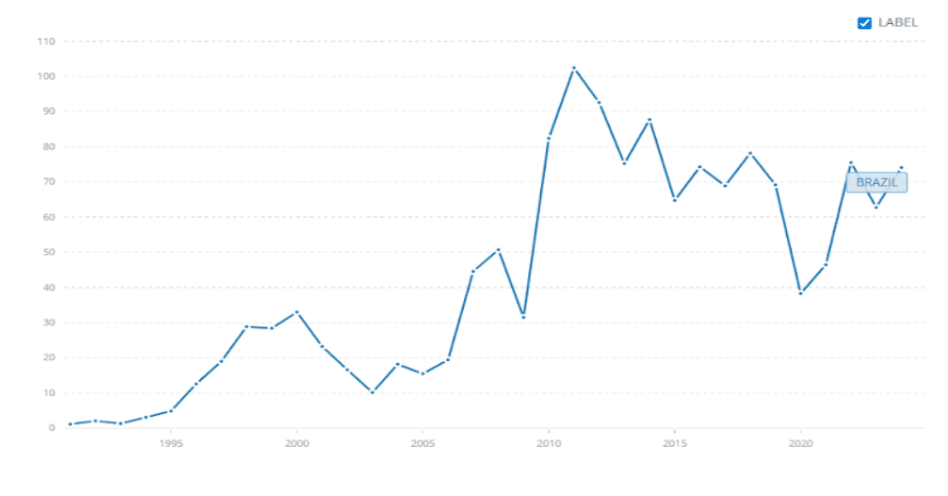

Brazil: Marketing Segmentation and Investor Signalling

Brazil’s corporate governance environment has changed through market-driven processes, most notably the introduction of the Novo Mercado segment on the B3 stock exchange. Companies listed under Novo Mercado voluntarily conform to more stringent governance standards, which include stricter disclosure requirements, giving all shareholders the right to vote, and independent board composition.

Empirical studies and market data suggest that Novo Mercado companies consistently have an advantage over their peers in attracting equity capital. Between 2015 and 2022, equity inflows in Novo Mercado firms were almost double the amount of companies listed on traditional segments.

In addition, these firms had reduced stock volatility and tighter bond spreads as a sign of greater investor trust and perceived creditworthiness.

Figure 3. Foreign direct investment inflows in emerging markets- Brazil.

Source: World Bank World Development Indicators.

Foreign direct investment, net inflows (BoP, current US$) – Brazil | Data

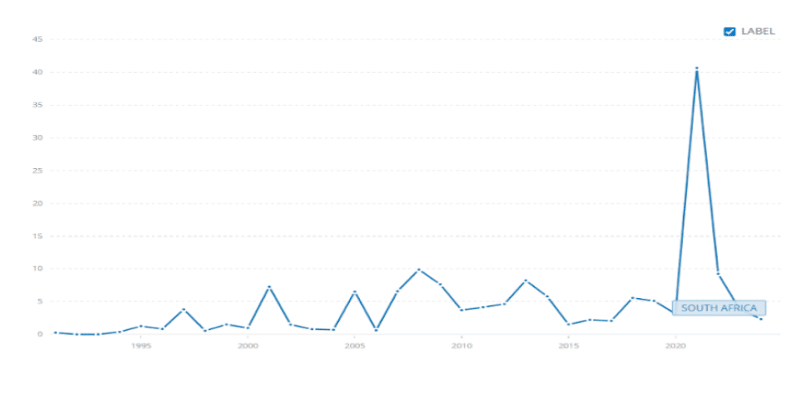

South Africa: Governance Innovation, Integrated Reporting

South Africa has established itself as a leader in governance innovation with the King Reports, with a specific focus on King IV, including integrated reporting and stakeholder inclusivity. Unlike the traditional governance codes that only emphasise the rights of shareholders, King IV asks firms to provide information about generating value over time for a variety of stakeholders, such as employees, communities, and the environment.

Firms that have adopted King IV principles early have done so with measurable financial benefits. According to data from the Johannesburg Stock Exchange (JSE) and Moody’s, these companies saw an improvement in credit ratings, and bond yields improved by an average of 50 basis points. This evidence suggests that comprehensive governance disclosures not only help to build the trust of investors, but they also reduce perceived risk premiums in debt markets.

Figure 4. Foreign direct investment inflows in emerging markets- South Africa.

Source: World Bank World Development Indicators.

Foreign direct investment, net inflows (BoP, current US$) – South Africa | Data

7. Investor Trust and Market Behaviour

Investor trust is key to how dynamic financial markets are, especially in emerging economies where the institutional safeguards may not be as strong. Governance disclosures are an important mechanism for creating this trust by decreasing information asymmetry and signalling managerial accountability. When investors have a perception of a firm being transparent and well-governed, they are more likely to commit capital, be willing to hold investments for longer and tolerate short-term volatility.

In the realm of equity markets, trust is demonstrated by higher trading volumes, lower stock price volatility and higher valuations. For example, companies in India and Brazil that regularly reveal their governance in great detail tend to have more stable share prices and attract more foreign portfolio investment. This is particularly in times of uncertainty in the markets, and where transparent governance is a buffer against panic-driven selloffs.

In debt markets, the trust of investors affects the price of bonds, the rating of bonds and the cost of capital. A well-governed firm has better governance disclosures, which are typically seen as having reduced risk, resulting in narrower bond spreads and better access to long-term financing. In South Africa, businesses that implemented King IV reporting standards experienced measurable changes in their credit rating, further evidence of the relationship between disclosure and investor confidence.

Investor behaviour is also influenced by the perception of disclosures and not just their presence. Superficial or boilerplate disclosures may undermine trust, while detailed and forward-looking reports increase credibility. This makes the quality and consistency of governance communication extremely important.

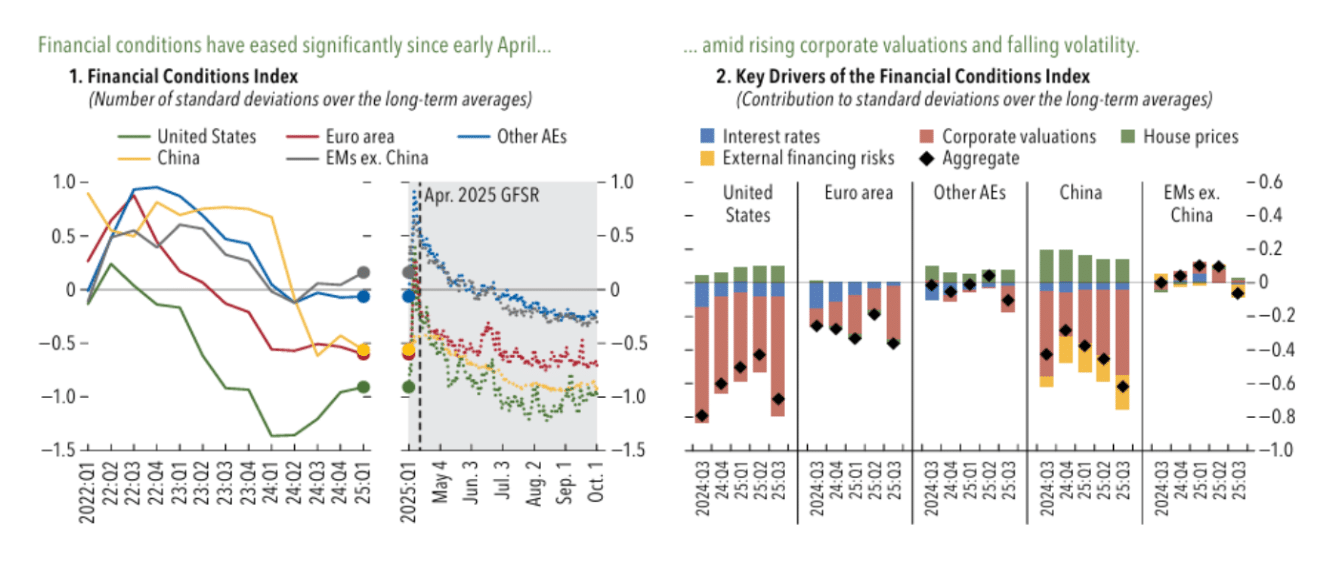

Figure 5. Global financial conditions and investor risk perception across major markets.

Source: International Monetary Fund, Global Financial Stability Report, October 2025.

Global Financial Stability Report, October 2025, “Shifting Ground beneath the Calm”

8. Impact on Equity Markets and Debt Markets

Governance disclosures have a measurable impact on emerging economies in both equity and debt markets. In equity markets, companies consistently reporting transparent governance information are often valued at higher levels, have more liquidity and tend to have more stable investment bases. This is especially true in India and Brazil, where countries that have good disclosure practices experienced consistent increases in foreign portfolio investment (FPI) and lower stock price volatility.

For instance, Indian companies that embraced increased board transparency and risk reporting in accordance with the Companies Act (2013) witnessed a 25-30 per cent growth in market capitalisation in five years. Similarly, Brazilian companies that are listed under the Novo Mercado segment, which comply with more rigorous governance norms, have done better than their peers in terms of equity inflows and investor retention.

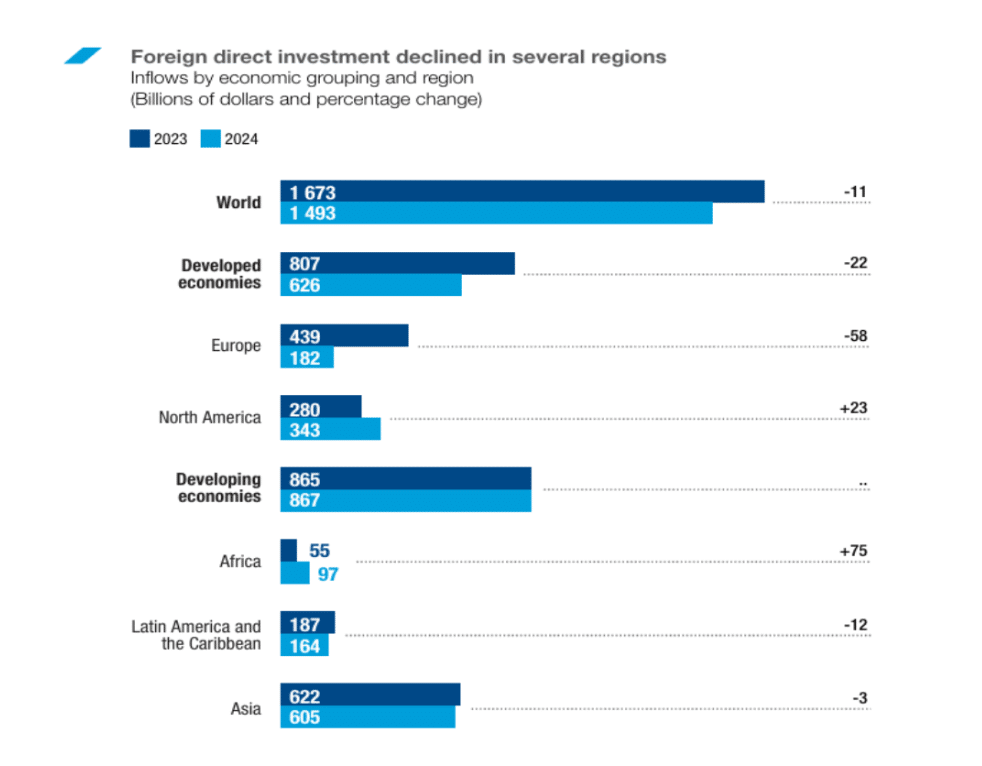

Figure 6. Global foreign direct investment inflows and capital market trends.

Source: UNCTAD, World Investment Report 2025.

World Investment Report 2025: Chapter 1

In the debt markets, disclosures regarding governance are important in the development of perceptions of credit risk. Firms that have strong governance structures often receive rewards in the form of lower bond yields and better credit ratings. In South Africa, the bond spreads of companies that put King IV principles into place have seen average bond spreads reduce by 40-60 basis points as investors were more confident their stocks were not overvalued and that management had reduced risk.

Moreover, governance transparency has an impact on the structure of capital flows. Institutional investors, who usually manage long-term funds, are more likely to invest their money in firms with consistent and credible disclosures. This transition from speculative to stable capital inflows leads to a more resilient and less vulnerable market to external shocks.

9. Policy Implications

The findings of this study underscore the strategic importance of governance disclosures in attracting stable, long-term capital to emerging markets. Transparency should not be viewed merely as a compliance requirement; rather, it represents a significant competitive advantage in the global capital landscape. To translate this insight into effective policy, several key priorities emerge:

- Regulatory bodies should strengthen disclosure requirements and ensure uniform enforcement. Although certain voluntary frameworks, such as Brazil’s Novo Mercado and South Africa’s King IV, have demonstrated success, broader adoption will require stronger institutional and legal backing. Governments can further encourage compliance by offering incentives such as tax benefits, preferential listing treatment, or improved access to public funding.

- Standardising governance reporting across emerging markets would enhance comparability and reduce due-diligence costs for international investors. Regional cooperation, potentially through platforms such as the BRICS or the Association of Southeast Asian Nations, could facilitate the development of harmonised disclosure standards aligned with global ESG benchmarks.

- Investor education and engagement should be prioritised. Empowering domestic investors to interpret governance disclosures can democratise capital markets, reduce excessive dependence on foreign capital, and promote greater financial resilience and inclusive growth.

In conclusion, strengthening governance disclosure frameworks, promoting standardisation, and investing in investor awareness are essential steps for emerging markets seeking to build more transparent, resilient, and globally competitive financial systems.

10. Future Outlook

As global capital markets begin to react more strongly to environmental, social and governance (ESG) factors, the importance of governance disclosures in emerging economies can only increase. Future developments are likely to be influenced by three trends:

- Digitalisation of the Disclosure

Emerging markets are now starting to go blockchain and AI-driven platforms for real-time governance reporting. These technologies can help increase transparency, decrease manipulation, and increase access for investors toward firm- level data.

- Integration with ESG Metrics

Governance will no longer be assessed in isolation. Investors are demanding integrated ESG disclosures, where there is an evaluation of governance practices alongside environmental and social performance. This shift will mean more holistic and standardised reporting frameworks adopted by firms.

- Cross – Border Regulatory Convergence

As capital is becoming more globalised, emerging markets may feel pressure to meet the level of governance standards of developed economies. This could result in the adoption of international disclosure norms, such as one put forward by the IFRS Foundation or the ISSB.

For researchers, future work could examine the causal effect of particular types of governance reforms on investor behaviour based on firm-level panel data. There is also scope to include the examination of the mediating role of cultural and political factors in the relation between disclosure and trust in various regions.

11. Conclusion

This study reveals the importance of governance disclosures in determining investor behaviour and capital flows in emerging markets. Based on the theory of agency and signalling, it shows that the practice of transparent governance lowers the level of asymmetry of information, enhances investor confidence, and attracts both equity and debt funds. Case studies from India, Brazil and South Africa demonstrate how regulatory reform and voluntary disclosure frameworks have led to real improvements in the markets in terms of increased foreign investments, improved credit ratings, and lower cost of capital.

The results imply that governance disclosures are not only compliance tools, but strategic ones for positioning in the market and being financially resilient. As global investors increasingly focus on transparency and accountability, it is important for firms and policymakers in emerging markets to see governance as a tool, not an obstacle to sustainable growth and competitiveness.

References

- B3 – Brasil Bolsa Balcão. (2023). Novo Mercado listing rules. https://www.b3.com.br

- Bloomberg. (2025). Emerging market capital flows and governance trends. https://www.bloomberg.com

- International Monetary Fund. (2025). Global Financial Stability Report. https://www.imf.org

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. (doi.org in Bing)

- Moody’s Investors Service. (2024). South Africa corporate bond ratings. https://www.moodys.com

- OECD. (2025). Corporate governance in emerging markets. https://www.oecd.org

- SEBI. (2013). Clause 49 of the Listing Agreement. Securities and Exchange Board of India. https://www.sebi.gov.in

- Spence, M. (1973). Job market signaling. The Quarterly Journal of Economics, 87(3), 355–374. https://doi.org/10.2307/1882010

- World Bank. (2025). Worldwide Governance Indicators. https://info.worldbank.org/governance/wgi/

Recent Comments