Introduction

1.1 Growth and Current Investing Landscape

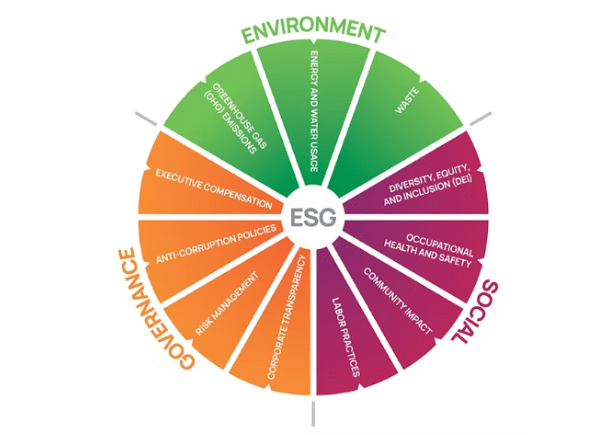

Environmental, social and governance (ESG) investing incorporates non-financial factors into investment decisions alongside traditional financial analysis. This approach has grown rapidly around the world as investors increasingly consider how companies manage environmental challenges, treat employees and communities, and maintain ethical governance. ESG criteria help assess a firm’s long-term sustainability and ethical impact, which can improve risk management and performance. The environmental component focuses on issues such as climate change, carbon emissions, resource use, waste, and pollution. The social aspect covers labor practices, human rights, health and safety, diversity and community engagement. Governance relates to board structure, executive compensation, anti-corruption policies, and corporate transparency.

Globally, the ESG investing market has expanded significantly. In 2023, the market size was estimated at around USD 25.10 trillion, and it is projected to grow to approximately USD 79.71 trillion by 2030 at an annual growth rate of about 18.8 percent, reflecting rising public demand for sustainable investment options and greater awareness of environmental and social issues. North America held the largest share of this market in 2023, and institutional investors accounted for the majority of ESG investments in that year.

1.2 ESG Investing in India

India has also witnessed notable growth in ESG investing in recent years. Although the Indian ESG market is still developing relative to global markets, it is expanding rapidly. Estimates suggest that India’s ESG investing market generated around USD 1.22 billion in revenue in 2024 and is expected to reach over USD 4.10 billion by 2030, with an annual growth rate of about 23.3 percent. This trend reflects rising interest among both institutional and retail investors.

Several factors are driving the increased adoption of ESG investment in India. A young and impact-conscious entrepreneurial culture is creating solutions in clean technology, climate resilience, and accessibility. Global capital flows and international investor mandates place greater importance on sustainability metrics. Government policies and regulatory clarity, including enhanced sustainability reporting standards, encourage alignment with ESG principles. Additionally, changing consumer preferences, particularly among younger generations, favour brands that prioritise environmental and social responsibility.

India’s rapid economic growth, combined with these ESG drivers, has helped move ESG investing from a niche concept toward a mainstream investment strategy. Regulatory initiatives by the Securities and Exchange Board of India (SEBI), including mandatory sustainability reporting frameworks for listed companies, have increased transparency and accountability, further supporting ESG integration in corporate practices.

1.3 Historical Context and Market Trends

ESG investing evolved from earlier ethical and socially responsible investing, which originally focused on excluding “harmful” industries. Over time, sustainability and corporate responsibility gained prominence, particularly following global environmental summits and the development of international frameworks such as the United Nations Principles for Responsible Investment. In the past decade, ESG factors have become central to investment strategies for major asset managers and institutions, supported by regulatory developments, improved reporting standards, and greater awareness of long-term environmental and social risks.

Public awareness of environmental and social issues, including climate change and social justice movements, has also contributed to the growing demand for investments that align with individual values while contributing to broader sustainable outcomes. This combination of market growth, regulatory momentum, and investor interest underscores the expanding role of ESG in global and Indian financial markets.

2.Financial Analysis of ESG Investments in India

2.1 ESG performance vs Financial Returns

In India, companies with consistently high ESG scores often show more stable cash flows and better long-term risk-adjusted returns. This is because ESG practices help in building up the company’s trust with the public. Considering tighter governance under ESG rules in the past year, a company that complies well with the rules can also actually benefit from them :

- Lower cost of debt– This is due to the presence of green bonds and sustainability-linked loans

- Higher foreign investment– To get global funds, companies have to go through multiple ESG screens. Companies that are actually approved can reap the benefits in the form of high foreign investment and improved access to capital.

- A good ESG score also leads to valuation premiums for companies. Valuation premiums represent the additional price investors pay for a stock or business above its intrinsic or book value, signalling high market confidence, strong growth potential, or strategic value. So, core ESG pillars are very much correlated with higher price-to-earnings ratios, which maximise shareholders’ wealth.

- During a time of market stress or volatility, ESG-focused Indian companies are less affected. This can be attributed to the various government incentives to boost these companies. Some examples would include Infosys and Tata, which are discussed further.

- Another important factor to take into consideration while looking at the ESG returns relationship is the sector under consideration. In IT, FMCG and pharma, there is a strong positive relationship between the two. In sectors such as energy and metals, short-term profitability conflicts with ESG due to the fact that these sectors require heavy investment themselves. But long-term investments are increasingly rewarded if made consciously.

While it is true that initial costs in ESG investments are extremely high, the long-term result is that they provide companies with is also non negligible.

All these points reflect one fact that ESG returns are highly correlated with financial returns due to better risk mitigation, capital efficiency and support of loyal investors.

As regulations tighten and global capital becomes more ESG-driven, this alignment is likely to strengthen further, making ESG not just an ethical choice but a financially material one.

3.Case studies

3.1 Infosys

Being one of the most trusted and reputed companies of India comes with a responsibility to fulfil certain criteria in the ESG department as well, and Infosys does this job well.

Their investments in ESG are reflected in the environment of the country. Some environmental outcomes of Infosys’s ESG investments are-

- Carbon Neutrality

- Infosys has achieved carbon neutrality across Scope 1, 2, and 3 emissions for the sixth consecutive year in FY25.

- The ESG report shows absolute reductions in greenhouse gas emissions compared to baseline scenarios: Infosys reduced Scope 1 & 2 GHG emissions by 75% and Scope 3 by 24.1% relative to 2020 targets through operational and clean energy investments.

- Infosys’ on-site solar plants generated 77 million kWh, and 77.7 % of electricity consumed in Indian operations came from renewable sources.

- Lake Rejuvenation Projects

- Infosys has implemented 11 lake rejuvenation projects in India, leading to an increase of ~4.3 billion litres of water storage capacity through partnerships with local stakeholders.

- Integration of Community and Biodiversity

- Long-term carbon offset and community energy programs benefit over 270,000 rural families via clean cookstoves and biogas systems. This leads to improved livelihoods and the use of cleaner fuels.

- Thousands of saplings are planted as part of agroforestry initiatives, contributing to carbon sequestration and biodiversity.

All of these efforts lead to outcomes that do not just improve the company’s ESG score but also lead to the betterment of the environment and the people. These investments lead to results that are tangible and that will benefit generations to come.

3.2 Tata group

Tata is perhaps the most widely known and beloved company in India, and its ESG outcomes show why. The company repeatedly invests for the better, and some examples of this are evident in its ESG Databook-

- Tata Consumer has invested in shifting its energy mix toward renewable energy sources and aligning with Tata Group’s broader ‘Project Aalingana’ net-zero roadmap.

- Over 60 % of direct energy needs are now met by renewable energy, which directly reduces fossil fuel use and associated carbon emissions.

- Year-on-year increase in renewable vs non-renewable energy use in FY25 (renewables ~270,824 MWh vs non-renewables ~248,224 MWh)

- Reduced energy intensity by ~15% despite business expansion.

- Tata Consumer tracks and changes packaging materials to reduce environmental impact, including recycled and certified inputs.

- 23,980 metric tonnes of waste recycled or reused in FY 2024-25 — significantly higher than waste disposed of.

- High percentages of sustainable packaging:

- 90 % of wood/paper fibre packaging from recycled/certified material

- 95 % of metal packaging is from recycled/certified material

- 100 % sustainable glass packaging

- Water Positivity Index of 2.2 indicates more water replenished than consumed in specific contexts. Community water projects and recharge initiatives contribute to increased groundwater and better local water security (e.g., Project Jalodari)

- Implementation of ISO 14001 Environmental Management Systems across operations. 75 % of company units have certified EMS, promoting standardised environmental performance.

All of these outcomes are a testament to the fact that thoughtful and conscious ESG investments can lead to huge positive outcomes in the long run. These outcomes are mutually beneficial, both to the nation and the company. They earn company tax benefits and a good reputation for the nation, and a better environment.

4.Policy and Regulatory Implications

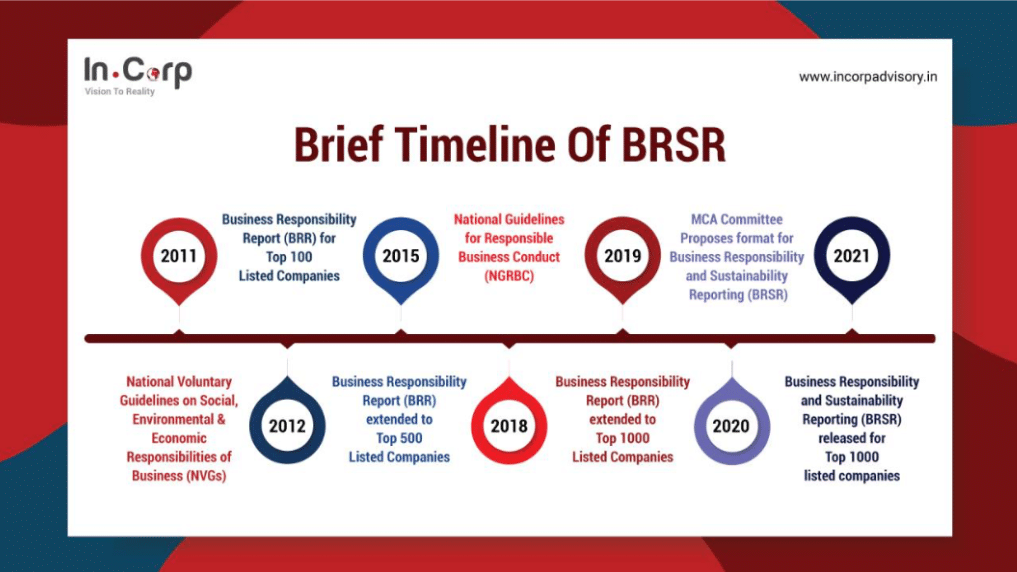

4.1 Effectiveness of India’s ESG disclosure requirements

ESG compliance refers to the mandate for companies to disclose how they impact the environment, society, and governance (ESG) in a transparent and accountable way.

In 2025, SEBI strengthened India’s ESG framework by introducing BRSR Core under the revised SEBI BRSR 2025 guidelines. The new mandate requires companies to disclose standardised, verifiable, and comparable data on key parameters such as carbon emissions, workforce diversity, ethical conduct, and board-level accountability.

By improving data credibility and consistency, BRSR Core enhances investor confidence while aligning Indian corporates with global sustainability benchmarks, making them more competitive and credible for international investors and stakeholders.

Source: Ascentium Incorp: https://www.ascentium.com/in/blog/brsr-a-new-avatar-of-esg-reporting/

Under the new BRSR ( Business Responsibility and Sustainability Reporting ) guidelines, companies are required to provide detailed information under the following parameters-

- Environmental Metrics-

Provide information regarding the company’s carbon footprint, energy efficiency, waste management, water conservation, and biodiversity protection.

- Social Metrics-

The social disclosures focus on responsibility to people and society, requiring companies to report on: diversity and inclusion, labour rights, employee welfare, CSR initiatives, and community engagement

- Governance Metrics-

Governance disclosures address ethical leadership, compliance, and data protection, including: board independence, the company’s risk management, ethics & anti-corruption policies, data security & privacy.

These requirements encompass every aspect of the company, be it the welfare of employees or the carbon emissions by a factory. Since this initiative was passed just in 2025, it is difficult to determine its overall effectiveness. But looking at its actual requirements, one could imagine that it would bring a big improvement in ESG inspection in the future.

Indian ESG policies fill the space that bridges domestic regulations with international climate governance initiatives ( Paris Agreement ). They embed international climate priorities within the domestic structure, making India more integrated into global sustainability.

4.2 Incentives for Green Finance

“Green finance” is used to describe financial investments and products, including loans, which have the purpose of funding environmentally sustainable initiatives, such as renewable energy, energy efficiency, and pollution reduction. It is expected to help develop a green, resilient, and low-carbon economy by funding initiatives that have positive environmental and economic benefits.

There are various incentives available for companies promoting green finance, some of which are written below:

-The Government of India and SEBI have enabled the issuance of sovereign and corporate green bonds. Sovereign Green Bonds, in particular, have helped in private investment by setting benchmarks and improving investor confidence in India’s green finance market.

– Provision of accelerated depreciation, tax holidays, and exemptions in duties for projects based on renewable energy and clean technology. All of this is expected to boost the post-tax returns of the investment in clean energy and green technologies.

– Introduction of the Indian Carbon Market (ICM) creates incentives for emissions reduction by enabling companies to monetise verified carbon savings. Over time, this can unlock private capital for decarbonisation projects across sectors.

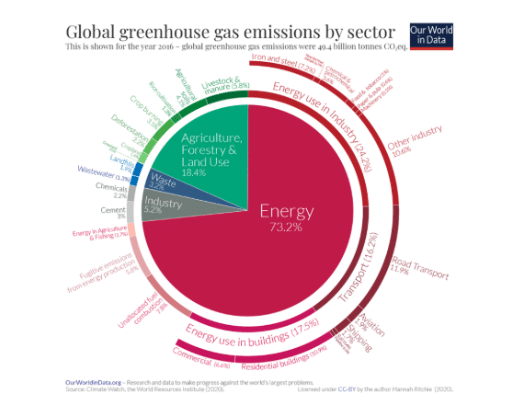

5.Measuring Environmental Outcomes

Source: Our World Data: https://ourworldindata.org/ghg-emissions-by-sector

5.1 Low-Risk ESG Firms (High ESG Performance / Top Performers)

- Proactive decarbonization: Tend to exhibit lower and declining carbon intensity (Scope 1 and 2) due to early investment in energy efficiency and renewable energy.

- Comprehensive Scope 3 reporting: More likely to measure, disclose, and set targets for Scope 3 (supply-chain) emissions, which often account for over 90% of total emissions.

- Internal carbon pricing: Frequently use internal carbon pricing to guide capital allocation toward low-carbon technologies.

- High-quality data and assurance: Adopt structured auditing and assurance processes for emissions data, improving transparency and reliability.

- Climate-positive targets: Increasingly move beyond net-zero commitments to set climate-positive goals, aiming to remove more CO₂ than they emit.

5.2 High-Risk ESG Firms (Low ESG Performance / Poor Performers)

- Reactive and compliance-driven: Emission trends are primarily shaped by regulatory compliance rather than voluntary, long-term strategies.

- Lagging decarbonization: Often struggle to reduce Scope 1 emissions, especially in hard-to-abate sectors with limited capital expenditure.

- Higher emissions intensity and greenwashing risk: Tend to have higher emissions per unit of revenue and face greater scrutiny over sustainability claims.

- Short-term mitigation focus: Prioritise immediate, low-cost actions to manage reputational risk instead of systemic decarbonization.

- Limited transparency: Face challenges in providing consistent ESG disclosures, resulting in data gaps for investors.

ESG risk ratings are numerical scores that assess the extent to which a firm is exposed to and manages environmental, social, and governance risks. These ratings help capture long-term sustainability issues such as energy use, greenhouse gas emissions, worker safety, and board structure that are often not reflected in traditional financial reviews but can have material financial impacts over time. Investors use ESG risk scores as a complement to conventional financial analysis to gain a more comprehensive view of a company’s resilience and long-term prospects. According to widely used methodologies, ESG risk scores are typically reported on a scale from 0 to 100, where a lower score indicates less unmanaged ESG risk and a higher score indicates greater unmanaged ESG risk. Scores are grouped into risk categories such as negligible (e.g., 0–9.99), low (10–19.99), medium (20–29.99), high (30–39.99), and severe risk (40 and above), with firms in the negligible and low categories generally considered more effective in handling ESG issues relative to their peers. Companies such as KeySight Technologies, RELX, and Accenture exhibit negligible risks.

Thus, corporate environmental outcomes using firm-level indicators such as greenhouse gas emissions intensity (Scope 1, 2, and, where available, Scope 3), energy mix, and disclosure quality, which together capture how firms manage environmental risks with long-term financial implications.

OUTCOMES

The relationship between ESG performance and environmental outcomes is commonly examined using quasi-experimental econometric frameworks, including propensity score matching to compare ESG-aligned firms with otherwise similar non-ESG firms, and panel fixed-effects models to control for unobserved firm-specific and time-invariant heterogeneity. These approaches aim to isolate the effect of ESG-related investment and governance practices on environmental performance while mitigating selection bias. Although firm-level environmental data remain partially constrained by disclosure limitations and proprietary access, the convergence of findings across matched-sample and panel-based studies supports the view that ESG-oriented firms achieve superior environmental outcomes through proactive decarbonization, improved transparency, and long-term capital allocation toward sustainable technologies. Accordingly, ESG performance serves not merely as a reputational signal, but as a meaningful indicator of firms’ capacity to manage environmental risks and enhance sustainability-adjusted value creation over time.

6.Challenges in ESG measurements and impact attribution

There has been a substantial rise in ESG investing over the past decade. In the United States, inflows into sustainable funds increased sharply from around $5 billion in 2018 to more than $50 billion in 2020, before rising further to nearly $70 billion in 2021. However, Morningstar reports that sustainable fund inflows dropped significantly to approximately $3.1 billion in 2022, marking the lowest level of inflows since 2015. This decline is largely attributed to adverse market conditions, including rising interest rates, higher oil prices, and increasing inflation.

Source: Isomatrix: https://www.isometrix.com/blog/esg-kpi/

At the same time, the slowdown in ESG investment has also been linked to growing skepticism regarding the effectiveness and credibility of ESG strategies. Concerns have emerged around whether ESG investing genuinely delivers meaningful environmental and social outcomes, as well as whether current reporting and evaluation practices provide sufficient transparency.

Several key challenges are frequently highlighted in discussions around ESG measurement and investing:

Greenwashing: Greenwashing refers to situations where companies or investment products portray themselves as more environmentally or socially responsible than they truly are. Critics argue that some firms make overstated or superficial sustainability claims to appeal to ESG-focused investors without implementing substantive changes.

Lack of standardised metrics: A major challenge in ESG assessment is the absence of uniform reporting standards. The lack of consistent metrics and frameworks makes it difficult to compare ESG performance across firms, sectors, and regions in a reliable manner.

Data quality and reliability: Sceptics raise concerns about the accuracy and completeness of ESG data. Issues related to inconsistent reporting practices, limited verification, and differing rating methodologies can weaken the reliability of ESG scores and reduce investor confidence.

Ethical concerns: Questions have also been raised about the ethical integrity of some ESG investments. Critics point out that certain ESG funds may include firms involved in controversial activities, calling into question the actual social and environmental impact of these investments.

Regulatory challenges: Differences in ESG regulations and disclosure requirements across jurisdictions create additional challenges. Without clear and enforceable standards, the risk of misrepresentation and inconsistent ESG practices remains significant.

While scepticism surrounding ESG practices has increased, some strong proponents argue that ESG investing has the potential to promote positive environmental and social change. As the ESG framework continues to develop, ongoing efforts aim to improve transparency, data quality, and reporting consistency.

To support the continued progress of ESG investing, strengthen investor confidence, and reduce market fragmentation, greater emphasis is needed on addressing these challenges. This includes improving consistency and transparency in ESG reporting, aligning disclosures with financial materiality, and promoting best practices in benchmarking and fund reporting.

According to a 2020 OECD report, advancing ESG practices requires coordinated efforts from policymakers, financial market participants, and other stakeholders. The report highlights five priority areas for improvement: consistency and quality of core ESG metrics, financial materiality of disclosures, fair treatment of large and small issuers, transparency of ESG scoring methodologies, and clear labelling and communication of ESG investment products.

In summary, strengthening ESG practices at a global level requires collaborative action across the financial ecosystem. Improving comparability, transparency, and credibility in ESG measurement remains essential for ensuring that ESG investing effectively supports sustainable outcomes.

7. Findings and discussions

Measurement and Economic Relevance of Environmental Outcomes

Corporate environmental outcomes are commonly measured using standardised ESG disclosures, including emissions intensity, energy mix composition, and water usage indicators reported in sustainability reports and ESG databases. Although differences in disclosure quality and coverage remain a limitation, these metrics are widely applied in academic research and investment analysis, making them suitable for cross-firm comparison (OECD, 2020). Beyond their measurability, these indicators carry clear economic relevance. Lower emissions intensity reduces exposure to environmental regulation, carbon pricing, and reputational risk. A higher share of renewable energy supports long-term cost stability and energy security, while efficient water use strengthens operational resilience, particularly in regions facing water scarcity. As a result, improved environmental performance can reduce long-term risk and support firm valuation and investor confidence, indicating that ESG-linked environmental outcomes are financially meaningful rather than purely symbolic.

8. Theories and Results

Stakeholder Theory and Environmental Performance: Stakeholder Theory provides a useful framework for understanding how environmental outcomes are integrated into corporate decision-making. The theory emphasises that firms operate within a network of stakeholders whose interests extend beyond shareholders alone. In the ESG context, this includes communities affected by environmental externalities, employees exposed to workplace and environmental risks, customers concerned with ethical production, and boards responsible for overseeing long-term impacts. Each stakeholder group has distinct expectations, requiring firms to balance competing demands through responsible engagement and governance. While shareholders may prioritise financial returns, other stakeholders value environmental protection, fair treatment, and social responsibility. Firms that proactively address environmental concerns enhance their legitimacy and long-term sustainability by aligning corporate actions with stakeholder expectations. Strong environmental performance among high-ESG firms is consistent with this perspective, as it reflects deliberate efforts to manage stakeholder relationships and reduce environmental harm.

Risk Management, Cost of Capital, and ESG: Risk Management Theory further explains the link between ESG engagement and firm performance. ESG-oriented firms are better positioned to identify and manage risks related to environmental regulation, social backlash, and governance failures. By proactively addressing these risks, firms reduce the likelihood of costly disruptions, regulatory penalties, and reputational damage. Investors respond to lower perceived risk by demanding lower risk premiums, which can translate into a reduced cost of capital (Krüger, 2015; Albuquerque et al., 2019). Improved environmental performance therefore, contributes to more stable cash flows and lower uncertainty. From this perspective, ESG activities function as a risk-mitigation mechanism rather than a discretionary cost, reinforcing the economic rationale for integrating environmental considerations into corporate strategy.

Thus, taken together, standardised environmental indicators, stakeholder considerations, and risk management mechanisms provide a coherent explanation for why higher ESG performance is associated with stronger environmental outcomes. Environmental improvements measured through emissions, energy use, and resource efficiency reflect both strategic stakeholder engagement and proactive risk mitigation. These linkages support the view that environmental performance is closely tied to long-term value creation and financial stability.

References

- ESG report | 2024-25. Available at: https://www.infosys.com/sustainability/documents/infosys-esg-report-2024-25.pdf

- Tataconsumer. Available at: https://www.tataconsumer.com/sites/g/files/gfwrlq316/files/2025-09/Tata_Consumer_ESG_Handbook_09_09_25.pdf

- Patodiya, S. et al. (2025) ESG compliance in India: SEBI BRSR rules, Maheshwari & Co. Available at: https://www.maheshwariandco.com/blog/esg-compliance-in-india/

- (No date a) ESG report | 2024-25. Available at: https://www.infosys.com/sustainability/documents/infosys-esg-report-2024-25.pdf

- Namdev, K. (2025) Top companies list with high ESG risk rating scores, SG Analytics. Available at: https://www.sganalytics.com/blog/top-companies-with-high-esg-risk-rating-score/

- (2025) https://journals.sagepub.com/doi/10.1177/09721509221129910.

- ESG trends from 2025 and what to expect in 2026 (no date) Donnelley Financial Solutions (DFIN). Available at: https://www.dfinsolutions.com/knowledge-hub/blog/esg-trends-2025-and-what-expect-2026#:~:text=Key%20ESG%20Trends%20That%20Shaped%202025&text=One%20of%20the%20most%20defining,change%20and%20greenhouse%20gas%20emissions. Team, T.I. (no date) Environmental, social, and governance (ESG) investing: What it is & how it works, Investopedia. Available at: https://www.investopedia.com/terms/e/environmental-social-and-governance-esg-criteria.asp (Accessed: 26 January 2026).

- authorsalutation:|authorfirstname:Nitesh|authorlastname:Mehrotra|authorjobtitle:Consulting Partner, S. and C., authorsalutation: |authorfirstname:Damandeep Singh|authorlastname:Ahluwalia|authorjobtitle:EY India Climate Change and Sustainability Services Associate Partner|authorurl:https://www.ey.com/en_in/people/damandeep-singh-ahluwalia and authorsalutation:|authorfirstname:Heena |authorlastname:Khushalani|authorjobtitle:Partner, C.C. and S.S. (no date) As ESG reporting becomes mainstream, complex challenges persist, EY. Available at: https://www.ey.com/en_in/insights/climate-change-sustainability-services/as-esg-reporting-becomes-mainstream-complex-challenges-persist (Accessed: 26 January 2026).

- Yellow, S. (no date) Challenges and opportunities to ESG investing, 2Future Holding – Meet The Future. Available at: https://www.2future.co/post/esg-investing (Accessed: 26 January 2026).

- Stakeholder theory in ESG → term (1970) Pollution. Available at: https://pollution.sustainability-directory.com/term/stakeholder-theory-in-esg/ (Accessed: 26 January 2026).

- The Relationship Between ESG Performance and Cost of Capital in Listed Companies (no date) https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5261740. Available at: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5261740.

Recent Comments