India’s startup success over the last decade has relied heavily on apps and software-led businesses like marketplaces, fintech, and edtech. A promising trend is the rise of deeptech, which includes startups rooted in scientific research and engineering. This includes areas like semiconductors, aerospace, robotics, batteries, medtech, and industrial AI. This article looks at the global origins of the deeptech concept. It also documents India’s adoption and its economic effects so far. Additionally, it analyzes why many Indian startups have focused on apps and considers whether and how India can shift towards growth driven by innovation. By using recent funding reports, government announcements, and interviews with founders and investors, the piece identifies challenges such as patient capital, manufacturing, talent, and regulatory issues. It also outlines possible solutions, including consistent policies, collaborations between industry and academia, and mixed financing. The conclusion provides recommendations for policymakers and founders, along with specific opportunities that India can pursue as a first mover.

1) The rise of deeptech -> meaning, global origins and economic shifts

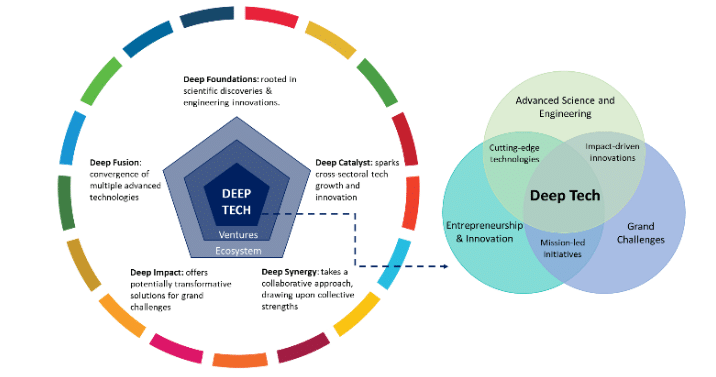

What is “deeptech”

Deeptech startups are based on scientific or engineering breakthroughs. They need ongoing research and development, specialized talent, prototypes, lab or manufacturing facilities, and longer paths to market. Examples include semiconductor design and production, satellite launch vehicles, advanced battery chemistry, medical diagnostic devices, robotics and industrial automation, and chemical/materials innovations. Unlike consumer apps, which are quick to build and grow, deeptech requires investment, diverse teams, and close cooperation with industry, regulators, and research institutions. According to MIT REAP (Regional Entrepreneurship Acceleration Program), deeptech firms differ because they “push the limits of human capability using complex technologies rooted in research”

When the term emerged and which countries progressed first

The term “deep technology / deeptech” formed in the investor and research communities during the 2010s. It describes startups that go beyond just software. Europe and the United States, particularly Silicon Valley, Boston, and Israel, were early leaders in deeptech due to strong links between universities and industry, venture funding aimed at long-term projects, clusters of advanced manufacturing, and translating defense and space research into commercial applications. From the 2000s to the 2010s, China quickly advanced in hardware and manufacturing scale. The US, with its government labs, universities like MIT and Stanford, and specialized funding, arguably moved fastest in commercializing deeptech across various sectors, including biomedical devices, semiconductor intellectual property, and aerospace startups. (See comparative analyses and market reports in sources below.)

Economic & market shifts linked to introduction of Deeptech globally

Global introduction of deeptech has brought about major economic and market changes. These are marked by high capital needs, longer development times, and the creation of specialized job roles.

Economic and Market Shifts

Deeptech’s global growth is driven by industries such as AI, quantum computing, robotics, biotech, advanced materials, and semiconductors. Markets have seen increased investment. Deeptech sectors now represent around 20% of venture capital globally, a rise from 10% a decade ago. The commercial impact is immense. AI alone is expected to add $13 trillion to the global economy over the next decade. Countries like the US, China, and Europe are investing heavily through industrial policies to build local capabilities in chips, batteries, and clean technologies. There is a strong focus on local manufacturing and intellectual property capabilities to reduce supply chain vulnerabilities.

Global Venture Capital Growth in Deeptech

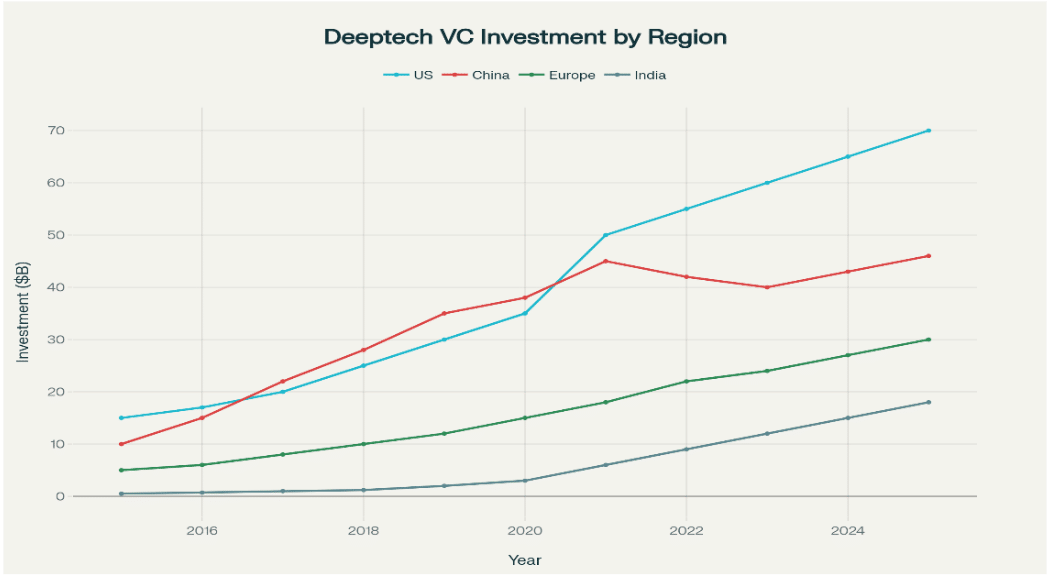

Venture capital investment in deeptech sectors has grown rapidly, increasing from less than $35 billion globally in 2015 to over $160 billion by 2025. The United States is at the forefront of this growth, supported by strong connections between universities and industries, along with government funding for research and development. China saw its peak during 2018 to 2021, while the European Union provided consistent support through policy. India’s contribution, though smaller, shows the fastest growth rate. This reflects its shift from software services to innovation-led manufacturing and research and development centers.

Shift in Workforce Skills and Job Impact

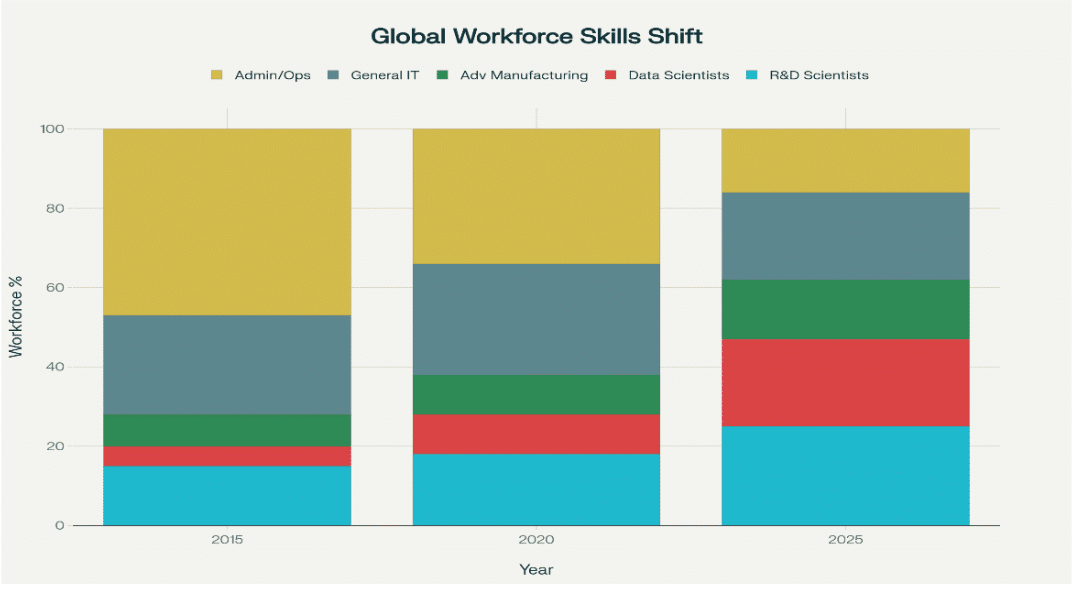

The introduction of deep tech has changed the workforce by increasing the demand for skilled professionals in R&D, engineering, advanced manufacturing, data science, and AI. Global trends show a rapid need for upskilling. For instance, AI-driven automation is changing roles for knowledge workers like scientists and engineers. This brings some risks of job displacement but also creates new, complex positions. The future workforce will need ongoing reskilling and flexibility as the demand for digital skills rises in sectors beyond technology, such as healthcare, finance, manufacturing, and retail.

Talent shortages in deep tech fields, including quantum computing, AI, robotics, and biotech, have led to competition for skilled workers, especially in North America and Europe. Companies are looking for younger, lower-cost talent while facing challenges in maintaining a pool of experienced professionals. Upskilling programs in education and industry aim to close these gaps and prepare workers for digital transformation and new roles that require both specialized knowledge and tech skills.

2) Rise of deeptech in India -> adoption, timing, economic consequences & pioneers

When deeptech started rising in India

India’s deeptech adoption picked up speed in the late 2010s and gained strong momentum from 2020 to 2025. Two key factors made this happen: (1) a new group of technical founders from leading engineering and research institutes, and (2) government policy support and mission-level programs, especially the India Semiconductor Mission and Semicon events. The government’s efforts led to high-profile SEMICON India events in 2024 and 2025, along with several approvals for semiconductor projects.

Financial and economic consequences so far

The financial and economic impact of deeptech introduction in India has become increasingly important, though it comes with specific challenges and opportunities.

Financial and Economic Impact

Funding Growth and Economic Contribution: Deeptech startups in India have seen rising investments, with funding growing by 78% in 2024, reaching about $1.6 billion. By 2030, deeptech is expected to add around $350 billion to India’s GDP. This shows its growing role in economic growth and innovation-driven development.

Job Creation and Skill Development: Deeptech ventures generate high-skilled jobs in R&D, engineering, manufacturing, and AI sectors. While job creation per dollar spent is lower than in consumer tech, deeptech has a significant multiplier effect through building manufacturing ecosystems and enhancing export capabilities. This improves long-term job quality and wages.

Export and Strategic Independence: Deeptech supports higher-value exports, such as semiconductor components and space technology. This aligns with India’s goals for strategic self-reliance (Atmanirbharta). Government initiatives like the India Semiconductor Mission aim to lessen import dependency and bolster domestic manufacturing and innovation.

Specific Advantages India Offers

Large Engineering and Technical Talent Pool: India boasts a vast number of engineers and scientists from top institutes, providing essential specialized skills for deeptech sectors.

Cost Advantages: Compared to developed economies, India offers affordable R&D, prototyping, and manufacturing. This can speed up product development and scaling.

Large Domestic Market for Pilots: India’s extensive and varied domestic market provides unique benefits for testing and improving deeptech solutions before they scale globally.

Government Policy Support: Recent government efforts, particularly the India Semiconductor Mission and growing fiscal incentives, show a strong commitment to developing the deeptech ecosystem.

Specific Disadvantages and Challenges India Faces

Scarcity of Patient Capital: Deeptech startups struggle to secure long-term series A+ funding required for lengthy R&D cycles. Venture capital generally favors faster returns in consumer tech, leading to funding gaps for deeptech.

Infrastructure and Incubation Deficiency: Many public R&D labs lack incubation facilities or collaboration with startups. Infrastructure issues, including limited advanced manufacturing testbeds and inadequate digital infrastructure, hinder growth.

Talent Drain and Specialized Skill Gaps: Despite having a large talent pool, there is a shortage of highly specialized skills in emerging fields like quantum computing and AI. Brain drain to more developed ecosystems further limits the availability of experienced deeptech professionals.

Regulatory and Market Readiness Issues: India deals with complex regulations and lacks specific compliance frameworks for emerging technologies. This slows down market adoption. Deeptech solutions often advance quicker than the market is ready for, creating uncertainties for investors.

Is India late, and can it recover lost time?

In many deeptech areas, such as advanced semiconductor fabs and aerospace manufacturing, India is behind the US, China, and the EU. However, being late to enter the market is not a death sentence. India can use its strengths: a large pool of engineering talent, lower costs for assembly and manufacturing, a sizable domestic market, and recent policy initiatives. Recovery will depend on ongoing policy support, including incentives and procurement, focused funding for Series A+ rounds, and the development of manufacturing/testbeds and university spinout programs. PM Modi’s comments at SEMICON and several project approvals for 2024-2025 demonstrate a commitment to policy and funding that could shorten the catch-up period if implemented consistently.

Why the sudden rise, and who are the pioneers, and what do they say?

Why is this happening now? There is a mix of policy changes, returning entrepreneurs and founders, specialized funds, the global push to diversify supply chains, and a surge in demand for AI and hardware. Pioneers include Agnikul Cosmos (Srinath Ravichandran), Skyroot Aerospace (Pawan Kumar Chandana), Pixxel, and Bellatrix in the space sector; a new wave of chip-design startups and battery/EV tech companies; and earlier medtech firms like Niramai and SigTuple. Founders often mention legacy institutions like ISRO and IITs as key.

3) Can startups move beyond apps?

In recent years, India’s startup scene has been mostly led by major consumer app-based companies, but a rising group of deeptech startups is also starting to emerge. Notable app-based startups include Flipkart, Ola, Zomato, Swiggy, Paytm, Byju’s, PhonePe, and Dream11. These companies have several things in common. They focus on addressing large-scale problems faced by Indian consumers using technology platforms. They use software-driven network effects and benefit from India’s growing internet and digital payments infrastructure. Their business models emphasize rapid growth, relatively low capital needs, and fast routes to market. By adopting platform economics, these startups can effectively make money while expanding their user base both nationally and internationally.

In contrast, India’s emerging deeptech startups like Agnikul Cosmos, Skyroot Aerospace, Pixxel, and Bellatrix Aerospace in the space sector, as well as chip-design, battery, and medtech firms such as Niramai and SigTuple, represent a different type of business. These startups are built on scientific research and need substantial capital, specialized talent from various fields, and longer development times. They also share some common traits, such as strong ties with universities and industries, using institutions like ISRO and IITs, a focus on product and IP-driven innovation, and active participation in government initiatives like the India Semiconductor Mission. While deeptech startups create high-value exports and develop strategic technologies, app-based startups achieve quick consumer adoption and generate significant job growth in operations and service roles. Together, these startups showcase India’s diverse innovation landscape in terms of speed, scale, and technological depth.

Why major startups in India are app-based

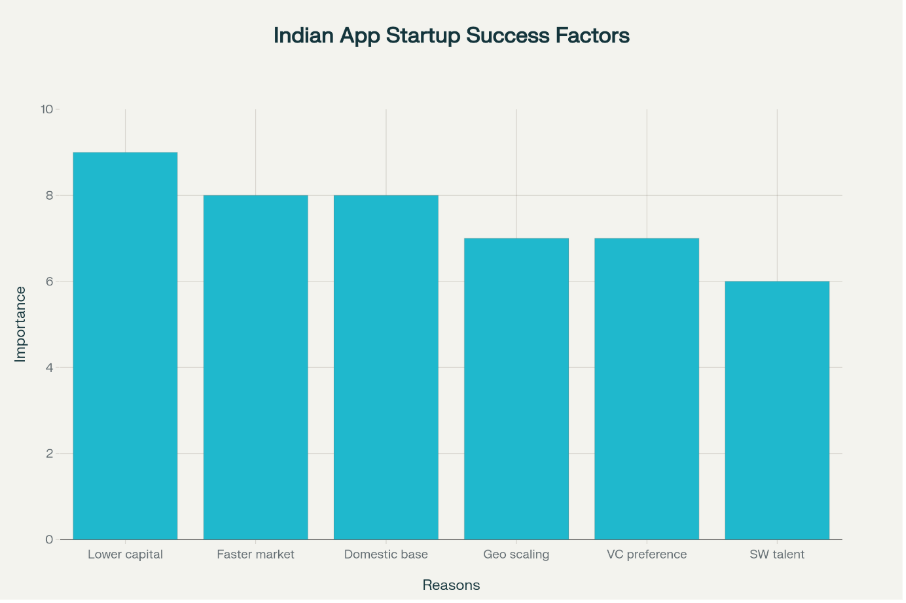

The main reasons include lower capital needs, quicker time to market, a large domestic consumer base that apps can serve quickly, easier geographic expansion across regions, venture capital’s preference for investments that offer faster returns, and a talent pool that mainly focuses on software engineering. These factors create a strong environment that supports consumer app startups more than capital-heavy and longer-lasting deeptech ventures.

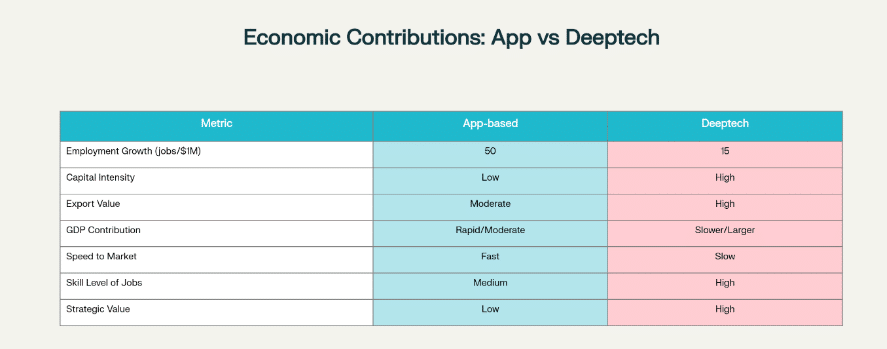

Economic Contributions comparison

Key data points include:

Employment growth: Apps generate around 50 jobs for every $1 million invested, while deeptech creates about 15. This illustrates that deeptech requires more capital but offers fewer jobs initially.

Capital intensity: App startups need less capital, allowing them to scale quickly. In contrast, deeptech requires a high upfront investment in research and development and manufacturing.

Export value: Apps contribute moderate value mainly through software as a service and consumer-facing services. Deeptech startups, however, generate higher export value with hardware components and advanced tech products.

GDP contribution: App startups influence GDP by scaling quickly and gaining consumer acceptance, while deeptech contributes more substantial value per company over time through durable industrial capabilities.

Speed to market: Apps reach the market more quickly, benefiting from shorter software development cycles. Deeptech, on the other hand, requires extensive research and development and regulatory approvals.

Skill level: Jobs in deeptech are more specialized, focusing on research, engineering, and manufacturing. In contrast, app jobs tend to be medium-skilled, involving operations and customer service.

Strategic value: Deeptech startups hold significant strategic importance because they relate to technological sovereignty and industrial independence, while apps have a lesser strategic impact.

Manufacturing of advanced components, like chips and sensors, takes place locally. This includes hardware productization for robots, drones, and launch vehicles. Industrial AI is embedded into manufacturing. There are also medtech devices and diagnostics, along with climate tech hardware such as batteries and electrolyzers. Essentially, these are product and IP-driven firms, not just focused on software.

How new ideas will affect the economy and sustainability

Economic impact: increased GDP share from manufacturing and exports, better trade balance on components, growth of higher-skilled labor markets.

Environmental and social sustainability: it depends on the sector. For example, battery and hydrogen technology can help reduce carbon emissions in transport if the sources are sustainable. However, manufacturing processes need to control pollution and waste. Responsible scaling and regulation are necessary. Deep tech can also promote social inclusion by providing affordable diagnostics and clean energy solutions for rural areas if it considers local limitations. India’s Deeptech Ecosystem: Barriers and Opportunities

Barriers and opportunies for deeptech led growth

Barriers

Lack of Patient Capital:

Deeptech startups require long-term investment for research and development and prototyping.

Indian venture capitalists prefer quick returns, focusing on software and consumer tech.

This funding gap limits growth and commercialization.

Weak Manufacturing and Supply Chains:

There is a limited number of semiconductor fabs, precision manufacturing, and testing facilities.

A heay reliance on imports raises costs and slows product development.

The absence of local ecosystems makes it hard for hardware-driven startups to scale.

Regulatory Complexity:

Overlapping and unclear regulations exist in sectors like healthcare, aerospace, and clean energy.

Lengthy approval and certification processes slow down innovation.

Inconsistent policies discourage startups from joining regulated industries.

Low Translational R&D Funding:

There is a weak link between academic research and commercialization.

Limited mentorship, funding, and technology transfer ways hinder progress.

Many lab innovations do not turn into market-ready products.

Opportunities

Vast Domestic Market for Pilots:

India’s diverse population creates a large testing ground for deeptech solutions.

This allows for rapid iteration and the development of scalable, affordable technologies.

Government as a Key Buyer:

Public sector demand in defense, healthcare, and smart cities encourages early adoption.

Programs like the India Semiconductor Mission and Atmanirbhar Bharat increase confidence and funding.

Government procurement provides early revenue and helps validate technology.

Current stance of government, public and job market and what’s being done

Current Stance of Government

The Indian government is actively supporting deeptech innovation through specific policies, programs, and initiatives.

Strategic Policy Initiatives: The government launched flagship programs like the India Semiconductor Mission to enhance domestic manufacturing in semiconductors and electronics. The SEMICON India events (2024-2025) highlight the importance of developing the deeptech ecosystem, with public announcements and approvals of major semiconductor projects. PM Narendra Modi’s speeches focus on achieving 100% local electronic manufacturing and aim for strategic self-reliance (Atmanirbharta).

Fiscal and Procurement Support: The government offers incentives such as subsidies, tax breaks, and early procurement commitments in sectors like defense, healthcare, and public utilities. These measures aim to boost demand for local deeptech solutions. Long-term funding programs targeting translational R&D and manufacturing testbeds are also being created.

Skilling and Talent Development: There are initiatives to train engineers and technicians for deeptech industries, with collaborations between leading institutes (IITs) and industry players. Vocational training geared toward manufacturing roles is expanding to meet the need for skilled workers.

Public and Investor Awareness

Public and investor awareness of deeptech’s potential for innovation-driven growth and technological independence is growing. Specialized deeptech funds like Yali Capital’s ₹893 crore AIF highlight increasing interest from private investors, despite market fluctuations.

Venture capitalists and corporate investors are setting up dedicated funds to back scalable deeptech startups, marking a shift from traditional consumer tech-focused portfolios.

Regional innovation hubs, particularly in Chennai, Bengaluru, and Hyderabad, are attracting investments and nurturing an emerging ecosystem through partnerships between academia and industry.

Job Market Dynamics

Jobs in deeptech are increasing, focusing on highly skilled labor, including R&D engineers, manufacturing specialists, systems integration experts, and AI scientists.

Although deeptech creates fewer jobs per dollar invested compared to consumer app startups, it offers high-value, sustainable employment with better pay and opportunities for technology leadership.

The key challenge is to close the skill gap and address geographic concentration by expanding vocational retraining and building inclusive regional innovation clusters.

There is rising industry demand for practical experience and translational skills in new tech fields, prompting institutions and policymakers to work together on updating curricula and creating hands-on training programs.

What’s Being Done

Regulatory Reforms: Efforts are underway to streamline compliance processes and speed up approvals for deeptech products, especially in regulated areas like medtech, aerospace, and clean energy.

Infrastructure Development: Plans for national testbeds, ESDM (Electronics System Design and Manufacturing) parks, and fab clusters are being developed to give startups access to modern production and testing facilities.

Blended Finance Vehicles: New financing models that combine grants, equity, and debt are being promoted to tackle the long R&D timeline challenges and attract patient capital.

University Spinout Strengthening: Programs designed to encourage technology commercialization from academic research, including incubation support, mentorship, and industry partnerships, are gaining traction.

New Deeptech Ideas India Can Use or Develop Locally

1.Low-Cost Satellite Subsystems and Small Launcher Services

India can use ISRO’s decades of experience in space technology to create affordable satellite and launch solutions for the global smallsat market, which is expected to grow quickly.

Startups like Agnikul Cosmos and Skyroot Aerospace are already leading the way with local small launch vehicles, making satellite deployment cheaper for research institutions, startups, and developing nations.

By encouraging private involvement, shared launch facilities, and export-friendly policies, India can become a global center for low-cost satellite services.

2. Chip Design and Packaging

India can boost innovation in AI accelerators, IoT chips, and energy-efficient processors by concentrating on local chip design and packaging.

Working with global semiconductor companies and providing incentives through Special Economic Zones can help build domestic design and testing ecosystems.

Creating chip intellectual property at home will strengthen India’s role in the global semiconductor market and reduce dependence on imports.

3. Battery Chemistry and Recycling

India’s climate and varied mobility needs require local battery chemistries that work well in high temperatures, last longer, and ensure safety.

Focused research and development in cell manufacturing, solid-state batteries, and recycling systems can help India become self-sufficient in energy storage technologies.

Building a circular system for battery reuse and recycling will also tackle sustainability issues and open new industrial opportunities.

4.Affordable Medical Diagnostics and AI Imaging Solutions

With a large population and limited access to healthcare, India has great potential for low-cost, AI-powered diagnostic technologies.

Startups like Niramai (AI-based breast cancer screening) and SigTuple (AI pathology analysis) show how deeptech can offer early, scalable, and affordable healthcare.

Expanding these technologies for large-scale disease screening (like tuberculosis, diabetes, and retinal disorders) can transform public health delivery.

5. Industrial Automation and Robotics for Manufacturing SMEs

Many small and medium enterprises (SMEs) in India’s manufacturing sector remain largely unautomated, which hampers productivity and competitiveness.

Developing affordable industrial robots, IoT-enabled machinery, and AI-based quality control systems can help SMEs modernize without significant investment.

Supporting local robotics startups and incorporating automation solutions through government initiatives like Make in India can lead to significant productivity improvements and create new deeptech markets.

How India can gain first-mover advantage and current stance

Where first-mover advantage is realistic: low-cost satellite services, specialized chip IP for low-power edge devices aimed at emerging markets, affordable medtech for population screening, and industrial robotics for small and medium-sized enterprises. India’s domestic market offers a chance to test ideas locally before exporting them.

Current stance: India is shifting from making policies to approving projects. Many semiconductor projects were announced for 2023 to 2025. Additionally, domestic funding for deep tech is increasing. Success will depend on how well India keeps up the momentum and establishes itself as a leader in specific areas. (PM India)

Conclusion

Realistic verdict: India’s deeptech moment has come, but it is still in its early stages. Policy signals and initial funding are promising. However, transitioning from an app-focused ecosystem to innovation-driven growth needs patient capital, expanded manufacturing, applied R&D, and ongoing procurement support.

Top recommendations: (1) build national testbeds and manufacturing parks (ESDM/fab clusters); (2) scale translational grants and matched co-investments; (3) create blended finance vehicles to support long R&D cycles; (4) use government procurement to assure demand for early deeptech products; (5) strengthen university spinout ecosystems and vocational retraining for manufacturing jobs. With focused execution, India can advance beyond apps to an ecosystem that produces both quickly growing consumer successes and deeptech companies, leading to wider innovation-driven economic growth.

Recent Comments