Abstract

Silver holds a remarkable dual identity in the global economy, serving both as a vital industrial material and a time-tested store of value. This paper explores the growing forces behind the surge in silver demand in recent years, with particular attention to India’s position as one of the world’s largest consumers of the metal. Drawing on secondary data from industry reports, commodity exchange records, and macroeconomic indicators, the study analyses the structural and cyclical shifts that are reshaping silver markets globally. The findings show that industrial demand, driven by solar energy, electric vehicles, artificial intelligence hardware, and advanced electronics, now accounts for nearly 59% of global consumption, creating supply deficits that mining output alone cannot resolve. At the same time, silver’s reputation as an inflation hedge, its affordability compared to gold, and rising ETF participation have strengthened its investment appeal, pushing prices higher and attracting even more demand in return. These developments carry meaningful implications for commodity markets, for investors weighing portfolio decisions, and for policymakers in import-dependent economies like India, where silver is woven into both financial strategy and cultural tradition.

1. Introduction

Silver retains strong intrinsic value due to its unique physical and chemical properties, making it a critical industrial input in the modern economy. Yet its economic importance extends well beyond industry. For thousands of years, silver has served as money and a store of value across civilisations, and it continues to occupy a hybrid position in the modern economy, one that is deeply embedded in both manufacturing and financial markets.

This dual nature has placed silver at the centre of growing attention in recent years. Growth in AI, data centres, renewable energy, grid expansion, automotive electrification, semiconductors, and healthcare equipment has embedded silver deeply into modern manufacturing. At the same time, silver has long been regarded as a reliable hedge against inflation, currency depreciation, and periods of financial instability, making it an increasingly strategic asset for both individual and institutional investors.

This paper examines the key forces driving the surge in silver demand, exploring its industrial significance, investment appeal, and the supply constraints that have contributed to persistent market deficits. The sections that follow provide a conceptual and economic background of silver, an analysis of Indian and global demand trends, a discussion of industrial and investment drivers, and an assessment of the risks and future outlook for the market.

2. Conceptual and Economic Background of Silver

2.1 Silver as an Industrial Metal

Silver has the highest electrical and thermal conductivity among all metals, along with strong reflectivity, corrosion resistance, and natural antimicrobial properties. These qualities allow silver to perform reliably across millions of electrical cycles and are difficult to replicate without efficiency losses.

As a result, silver is extremely difficult to substitute in high-performance applications. Alternatives such as copper and aluminium do not match its conductivity or reliability, often causing higher resistance, heat loss, and reduced performance, outcomes that are unacceptable in semiconductors, AI hardware, and advanced circuit boards. Silver is essential in solar photovoltaic cells for efficient electricity transfer and in electric vehicles and charging infrastructure for power electronics and battery management systems. Its antimicrobial properties also make it indispensable in medical devices, where safety and effectiveness are critical.

Positioned at the core of green and energy-transition technologies, silver faces sustained long-term demand growth. Combined with supply constraints, rising industrial usage has contributed to persistent market deficits and upward pressure on prices.

2.2 Silver as a Financial and Investment Asset

For over 6,000 years, dating back to around 700 BC, silver has been used as money and a store of value across civilizations. In India during the 1980s, silver functioned less as a luxury and more as household financial security, with families storing wealth in coins and ornaments and farmers monetising silver during droughts. Between 1983-84 and 1990-91, silver prices rose steadily from ₹3,506 per kg to ₹6,760 per kg, delivering annual growth of approximately 10-12% and reinforcing its role as a long-term store of value.

Unlike gold, which is primarily held as a reserve asset and macroeconomic hedge, silver occupies a hybrid economic position. While gold remains the benchmark for wealth preservation and stability, silver offers greater affordability and higher growth potential. However, silver’s smaller and less liquid market also makes it more price-sensitive and volatile compared to gold.

Silver has long been regarded as a reliable hedge against inflation, currency depreciation, and periods of financial instability. Research indicates that silver tends to have a relatively low correlation with equities and bonds, which improves portfolio diversification and supports better risk-adjusted returns. As a result, silver is increasingly seen not merely as a speculative asset but as a strategic long-term investment. From a performance perspective, silver has delivered a CAGR of around 8.5 percent between 1983 and 2025. At this rate, an investment of ₹1 lakh in 1983 would have grown to approximately ₹50.5 lakh by December 2025, based purely on price appreciation. Unlike gold, silver’s investment demand is further supported by ETF inflows, retail participation, and industrial stockpiling during supply constraints.

3. Indian Trends in Silver Demand and Supply

3.1 Composition of Global Silver Demand

Silver’s distinctive physical properties such as exceptional conductivity, corrosion resistance, malleability, and ductility make it a perfect fit for industrial use across various domains. Therefore, it is no surprise that industrial applications account for approximately 60% of silver demand. Silver is predominantly required in electronics such as switches, circuit boards, and semiconductor chips, and it also has a very significant role in EV production, requiring around 25–50 grams per vehicle. Silver usage in photovoltaic cells used in solar panels has increased in global demand from 4% in 2016 to nearly 17% today. With growth in industrial demand, the silver sector in India is strategically gaining significance.

Silver’s bright shine and white lustre make its jewellery not only affordable but also attractive, especially in India, which accounts for 40% of total global silver jewellery demand. Jewellery contributes to roughly 18% of silver demand. Demand in this segment remains robust even during economic hardships because of its affordability compared to jewellery made from more expensive metals like gold, particularly in rural India.

Silver, being a safe haven asset, attracts investments, and investments in the form of coins and bars account for nearly 18% of silver demand, with expectations of continued growth. Along with the silver jewellery category, India also leads the silverware segment, accounting for more than half of global demand for traditional silverware.

Post-pandemic, overall demand for silver has soared by 80%, driven by an unprecedented combination of industrial expansion, energy transition, and intensified investor interest. Demand is expected to expand further in the coming years due to global uncertainties, geopolitical tensions, and inflationary fears.

3.2 Supply Structure and Constraints

Compared to growing demand, silver production remains limited. Silver is recovered both as a co-product and as a by-product. The metal is largely obtained as a by-product during the refining of lead, zinc, copper, and gold ores.

Silver supply in India and globally shows high inelasticity in the short run due to its by product nature, with over 70 percent sourced from base metals. As a result, supply cannot respond quickly to demand surges, leading to persistent deficits amid rising demand from green technology, electric vehicles, and electronics. Higher silver prices do not immediately lead to increased output, as mining decisions depend on base metal production rather than silver prices. Recycling provides some support but cannot fill large supply gaps in the short term. India, as one of the world’s largest consumers and with over 80 percent import dependence, faces shortages and high premiums when global supply tightens, as seen in late 2025.

In the long run, supply remains constrained because new mine development typically takes 5 to 10 years and is subject to regulatory, environmental, and financing challenges. Declining ore grades at existing mines further limit output growth. As a result, a structural deficit, where demand exceeds new supply and recycling, is expected to persist with no major new capacity in sight.

Silver’s recent price rally has been driven by tight supply and geopolitical uncertainty. Supply pressures intensified after the United States added silver to its critical minerals list in November 2025, triggering stockpiling and pushing US inventories to 531 million ounces by September. China’s export restrictions on rare metals added to availability concerns, causing physical shortages in key pricing centres such as London. Rising investor interest and strong inflows into Indian silver ETFs, reaching ₹5,342 crore in September, further increased demand for physical silver and reinforced upward pressure on prices.

4. Industrial Drivers of Rising Silver Demand

4.1 Electronics and Electrical Systems

Silver is the most electrically conductive metal, a property that makes it indispensable to modern electronics and electrical systems. Nearly all electronic devices contain some quantity of silver, ranging from everyday consumer products such as light switches, mobile phones, televisions, and computers to advanced systems like supercomputers used for artificial intelligence. Silver’s ability to conduct electricity efficiently, reliably, and over long operating lifespans creates a strong barrier to substitution, even during periods of elevated prices. As a result, demand for silver in electronics and electrical applications has grown steadily, increasing by approximately 4 percent annually to reach a record 13.2 million kilograms in recent years.

Although often invisible to end users, silver plays a central role in enabling the functionality and durability of modern electronic devices. It is widely used in membrane switches that respond to minimal pressure while maintaining performance over years of repeated use. These switches are found in products such as computer keyboards, microwave ovens, televisions, and household appliances. Silver is also used in printed circuit boards, where it appears in conductive inks and films that create smooth and efficient electrical pathways. These pathways allow devices to become smaller, faster, and more powerful while maintaining reliability.

Beyond consumer electronics, silver is a critical component in radio-frequency identification (RFID) tags, which are widely used in inventory management, theft prevention systems, electronic toll collection, and keyless entry technologies. Advanced technologies such as plasma display panels and the rapidly expanding 5G mobile network also rely on silver to achieve the high conductivity required for speed, stability, and signal reliability.

Rising digital infrastructure further amplifies silver demand. Data centres have become a backbone of cloud computing, artificial intelligence, and digital services. Over the past two decades, global IT power capacity has expanded sharply, driving increased demand for servers, networking equipment, and electrical systems that incorporate silver. As governments across major economies prioritise digitalisation and offer incentives to expand data centre capacity, silver’s role in supporting the digital economy continues to deepen.

4.2 Renewable Energy and Green Technologies

Renewable energy and green technologies represent the fastest-growing segment of industrial silver demand. Among these applications, solar photovoltaic technology is the most significant. Almost every solar panel contains silver, which is used as a conductive paste to transport electricity generated by solar cells. The share of solar energy in total industrial silver demand has risen sharply, increasing from around 11 percent in 2014 to nearly 29 percent by 2024. Although manufacturers continue to reduce silver intensity through technological improvements, silver remains the most efficient and reliable conductive material for photovoltaic applications.

Global commitments to renewable energy targets reinforce this demand. Large-scale solar installation programs, particularly in regions such as the European Union, are expected to support sustained silver consumption well into the next decade. Even as subsidies decline in some markets, ambitious capacity targets and falling solar costs ensure continued expansion, structurally anchoring silver demand within the global energy transition.

Electric vehicles (EVs) and electrification further strengthen silver’s strategic importance. EVs require significantly more silver than traditional internal combustion engine vehicles, as silver is used in battery management systems, power electronics, electrical contacts, and charging infrastructure. On average, electric vehicles consume between 25 and 50 grams of silver per unit, representing a substantial increase compared to conventional vehicles. As vehicle electrification accelerates globally, EVs are expected to become the primary driver of automotive silver demand, supported by parallel investments in charging networks.

Silver also plays a role in energy storage technologies, including silver-zinc and silver-oxide batteries. These batteries offer high energy density, durability, and long shelf life, making them suitable for specialised applications. While lithium-ion batteries currently dominate the market, growing interest in sustainable and recyclable energy storage solutions could expand silver’s future role. Together, renewable energy, electric mobility, and electrification create long-term structural demand, positioning silver as a core metal in the green energy transition.

4.3 Medical and Chemical Applications

Silver’s antibacterial and chemical properties have been recognised for centuries, but their relevance has increased significantly in modern healthcare. Silver is toxic to bacteria while remaining largely harmless to human cells, making it highly effective in preventing infections. Silver ions penetrate bacterial cell membranes and disrupt vital biological processes, enabling silver to combat even antibiotic-resistant bacteria.

As a result, silver has become an essential material in wound care and infection control. It is widely used in burn treatments, wound dressings, and topical ointments to reduce infection risks. Numerous medical devices, including catheters, respiratory equipment, and surgical instruments, are coated with silver to minimise bacterial buildup. In orthopaedics, silver coatings are applied to artificial bones and implants to improve patient safety and reduce post-surgical complications.

The post-pandemic period has further highlighted silver’s importance in healthcare and sanitation. Rising healthcare-associated infections and growing antibiotic resistance have renewed interest in silver-based solutions, including silver nanoparticles and antimicrobial coatings. These developments have expanded silver’s applications beyond traditional medical uses into hygiene products, sanitation systems, and healthcare infrastructure. As global healthcare systems increasingly prioritise infection control and resilience, medical and chemical applications are expected to remain a stable and growing source of industrial silver demand.

5. Investment Demand and Financial Appeal of Silver

5.1 Silver as an Inflation Hedge

Inflation and Precious Metals Demand

Inflation increases demand for precious metals as investors seek value preservation; silver’s use in solar panels, EVs, and AI, and now as a U.S.-China critical mineral, boosts it beyond gold’s monetary focus. China’s 2026 silver export policy curbs tighten inelastic supply, while India’s import of around 60% sustains high consumption despite festive demand.

Silver During Currency Depreciation

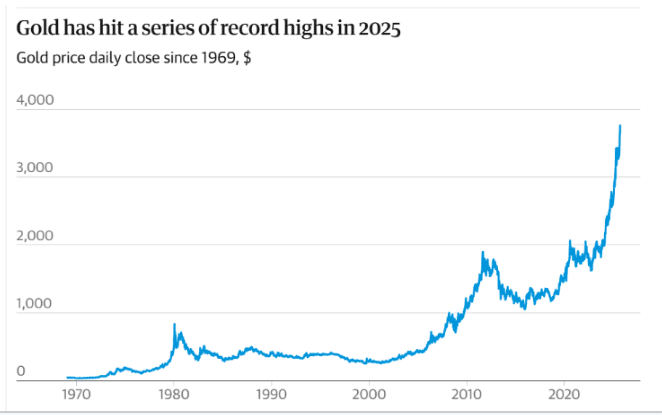

Depreciating currencies increase silver’s appeal, with rupee-dollar shifts raising import costs and prices. Silver has outperformed gold in 2025 amid debasement and industrial shortages, mimicking commodity crises. Central bank actions, like RBI’s $19B gold addition and PBOC buys, reflect a growing preference for metals as a safe option.

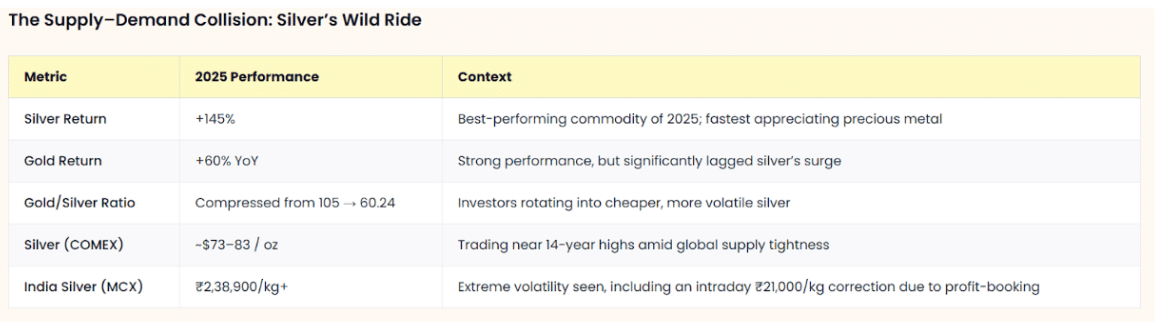

Comparative Performance

Silver excels in the short term in high-inflation areas, delivering 1,546% returns in the 1970s and surpassing gold in 2025 through industrial demand. Gold provides reliable long-term hedging, hitting $4,200+ amid tariffs and rate cuts. Stocks like Nifty/Sensex offer growth but higher volatility, underperforming gold’s consistent 63% returns. Real estate outperforms gold 85% over five-year periods with stability. Silver complements gold’s safe-haven status but trails real estate overall.

Source: Discovery Alert Precious Metals History

5.2 Investment Vehicles and Market Access

Silver Investment Vehicles

Silver ETFs, coins, and bars have surged globally, and record coins/bars demand amid industrial booms. Silver’s lower entry cost (₹200-300/unit vs. gold’s ₹6,000+) enhances retail access via MCX futures, while institutions pile in, yielding 210% ETF returns yearly.

Gold-Silver Ratio Dynamics

India’s MCX follows global gold-silver ratio moves, it jumps when the rupee weakens, then settles back with festival buying. Silver’s ups and downs work both ways: big wins in good times, sharp falls in bad. Common strategies involve ratio arbitrage which means buying silver when the ratio is low relative to gold and mean reversion trades based on their 0.8 correlation. MCX futures support these, subject to margin requirements and contract expiries.

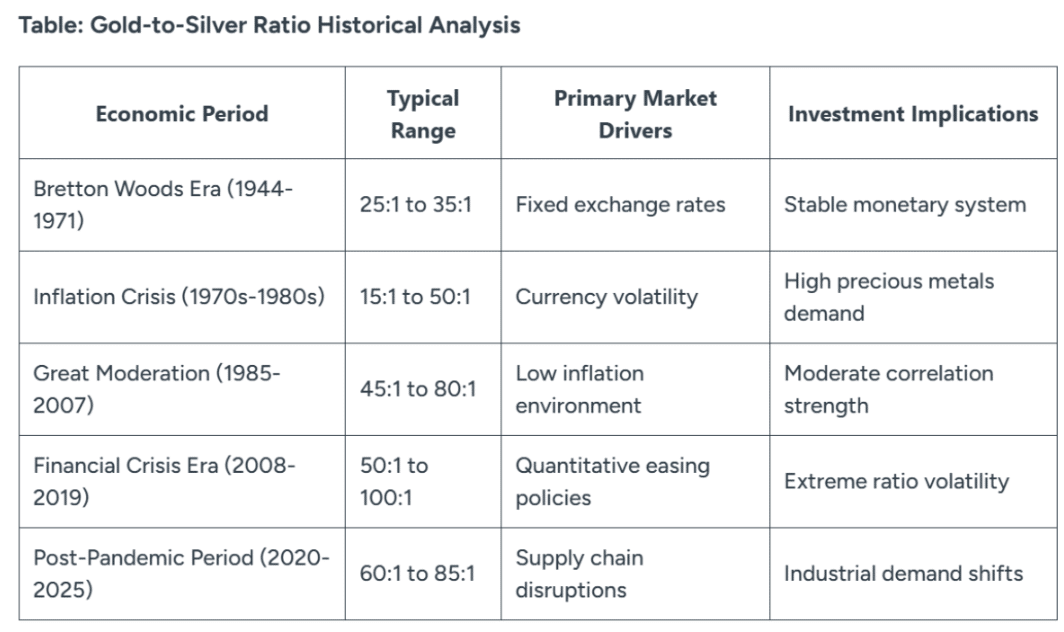

5.3 The Gold-Silver Ratio: Theory and Application

Definition and economic significance

The gold-silver ratio is just how many ounces of gold it takes to buy one ounce of silver, think of it like a price tag comparison. It usually sits between 40-80 over time. When it climbs above 80, silver often looks like a bargain compared to gold. Things like mine output (silver mostly comes as a side product), factory needs, and big money moves push it around. It’s a quick way to read market mood.

Historical trends

Worldwide, it shot to 120 in the 2020 COVID mess, then eased back to the 70s by 2025 as silver got squeezed by low supply. In India, MCX sees the same: jumps when the rupee slips, then calms with Diwali and wedding buys.

Silver’s higher volatility

Silver swings harder than gold, great for big wins like in 2025, but it hurts more when things drop.

Portfolio diversification implications

At high ratios, overweighting silver can enhance risk-adjusted returns by 5-10%, complementing gold’s stability.

5.4 India’s Precious Metals Market Landscape

5.4.1 Market Structure and Demand Patterns

India’s precious metals market reached USD 63 billion in 2024, and it is projected to grow at a 12.2% annual rate to USD 126 billion by 2030. Gold accounts for around 70% of this market, while silver is growing the fastest at 15%. Urban consumers prefer investing in gold ETFs and bars, but those in rural areas, who make up two-thirds of the population, lean towards silver jewelry. Seasonal demand spikes occur during Diwali, weddings, and other auspicious days, boosting demand by up to 40%. South India represents a large share of this demand.

Source : World Gold Council

5.4.2 Gold-Silver Investment Dynamics in India

Gold remains popular due to its cultural importance as wedding jewelry and its role as a hedge against inflation. However, younger investors are increasingly turning to silver. Retail participation in silver was up 7% in the first half of 2025, and imports soared by 431% as returns outperformed gold. Silver, often called “the people’s metal,” attracts middle-income groups because it is more affordable. Households generally invest 10-15% of their portfolios in precious metals overall.

Source: World Gold Council

5.4.3 Financing Against Precious Metals

The gold loan sector grew to over ₹1 lakh crore in FY25. The organized market is expected to reach nearly ₹1.5 lakh crore in FY26, with a 4% annual growth rate. Key players in this space include banks and NBFCs like Muthoot. These loans typically offer 75-85% loan-to-value ratios, with interest rates between 8% and 15% and terms ranging from 6 to 36 months. Silver is not often used for collateral due to price fluctuations and limited acceptance, leading to lower loan-to-value ratios. However, there is potential for specially designed silver-backed products.

5.4.4 Regulatory and Tax Framework

A flat 3% GST applies to both gold and silver, with an additional 5% on making charges. A 15% import tax raises domestic prices. Sovereign Gold Bonds offer tax-free maturity benefits, but there is no equivalent for silver. Mandatory hallmarking helps ensure purity and build consumer trust. MCX and SEBI provide strong oversight for futures trading and commodity markets.

6. Interaction Between Industrial and Investment Demand

6.1 Supply Squeeze Concept

Silver is increasingly being pulled in two directions at once. On one side, industrial demand is rising sharply, driven by sectors such as solar energy, electric vehicles, AI servers, and advanced electronics. These industries consume silver in large, non-negotiable quantities, often through long-term procurement contracts. As a result, a significant portion of available supply is diverted away from investment markets, tightening liquidity on exchanges like COMEX and reducing visible inventories.

By 2025, the silver market had recorded five consecutive years of supply deficits. Total demand stood at approximately 1.17 billion ounces, while supply lagged behind by nearly 500 million ounces. This persistent imbalance has created an environment of structural scarcity rather than a short-term disruption.

As supply tightens, prices rise, attracting more investor interest. Exchange-traded funds (ETFs) see higher inflows, and central banks such as India. begin increasing their exposure to precious metals. This creates a feedback loop: higher prices encourage investment demand, which further strains already limited supply.

Source: Supply Squeeze Gold Money

Crucially, this squeeze is not easily resolved. Silver mining cannot scale up quickly because the majority of silver is produced as a by-product of mining for metals like copper, lead, and zinc. Even when prices rise, miners cannot immediately increase output. Recycling also offers limited relief, as recovery rates are slow and existing above-ground stockpiles have largely been exhausted.

On top of these constraints, China’s export restrictions and the accelerating global transition toward green energy are likely to sustain pressure on silver supply. Together, these factors suggest that the current supply squeeze is structural in nature and likely to persist well into 2030.

Source: China Export Tariffs Fidyaa

6.2 Macro-Financial Linkages

Macroeconomic policy, particularly interest rate decisions by the US Federal Reserve, plays a crucial role in silver price movements. When the Fed cuts rates, real interest rates, defined as nominal rates adjusted for inflation, tend to fall. Lower real rates reduce the opportunity cost of holding non-yielding assets like silver, making them more attractive to investors.

In 2025, markets began pricing in rate cuts even before they occurred. Ahead of the first 25-basis-point cut in September, when rates were at a peak of 5.33%, expectations of easing had already pushed gold toward $2,600 per ounce, while silver remained range-bound around $35 due to persistent inflation concerns. However, after three consecutive cuts brought US rates down to the 3.5-3.75% range by December 2025, real rates turned negative. Silver surged past $62, while gold climbed above $4,200.

Real rates matter because they represent the trade-off between holding silver and earning returns from bonds. When real yields fall or turn negative, silver becomes relatively more attractive, leading to sharp increases in demand.

India’s monetary policy operates in a similar, though more muted, manner. A 25-basis-point rate cut by the Reserve Bank of India (RBI) to 5.25% in December 2025 triggered a rally in gold and silver by lowering borrowing costs and improving affordability.

Globally, US policy has a far greater influence. The Fed’s rate cuts were a key driver behind silver’s 120% surge in 2025. While RBI cuts have a smaller impact due to lower rate volatility, they still stimulate domestic demand, particularly during festival seasons when silver consumption can rise by nearly 40%. Silver’s price responds strongly because it sits at the intersection of industrial necessity and investment demand, amplifying the effects of both global and local monetary shifts.

7. Challenges, Risks, and Market Limitations

7.1 Supply-Side Challenges

Silver mining runs into serious issues because about 70-80% of it comes as a byproduct when digging for copper, zinc, or lead ores. That means supply depends more on demand for those base metals than for silver itself.

Starting a new mine takes a long time, typically 10-15 years from discovery to production, which we call the “gestation period.” So, when prices shoot up, we can’t quickly boost output to match.

On top of that, environmental regulations are getting stricter in major producers like Peru and Mexico. Emission controls, water usage limits, and waste disposal rules are hiking costs by 20-30%. The push for ESG standards is delaying projects further, keeping global supply tight even with 2025’s 500 million ounce deficit.

7.2 Price Volatility and Speculation Risks

Silver prices jump around a lot because of big bets by investors. In 2025, hedge funds and ETFs put in over $5 billion. This helped push prices up 120%, while COMEX storage (a US exchange’s stockpile) fell 40%. Small investors get hurt bad silver moves 1.5 times more than gold, so if gold drops 30%, silver can fall even harder and wipe out money borrowed to buy it.

MCX silver futures give big leverage (using small money to control lots, like 5-10 times your cash). But risks are huge, daily price caps at 4%, and switching contracts costs 1-2%. MCX swings 25-35% a year, more than COMEX’s 20-30%, because of rupee ups and downs.

Traders must deposit 7-12% of the contract value upfront as margin, which ties up capital. During low trading volumes, bid-ask spreads widen to 2-5%, increasing costs.

Global events such as US Federal Reserve policy pauses or Chinese tariffs often trigger sharp overnight price moves. Since MCX opens at 9 AM IST, these create gap risks. For instance, a December 2025 Fed signal propelled silver prices up by ₹10,000 per kg, surprising market participants.

7.3 Technological Substitution and Recycling

Research is finding ways to cut silver use, like copper alternatives in solar panels (down 10% per panel since 2020) and graphene in electronics. Silver remains key for EVs and 5G due to top-notch conductivity (lets electricity flow easily); substitutes lag 5-10 years behind.

Recycling eases demand pressure, meeting 20-25% of needs (up from 15% in 2020) from jewelry scrap and industrial recovery. India recycles 30% domestically, but global rates top out at 90% max due to high collection costs. It softens shortages but doesn’t fix them fully.

7.4 Emerging Market-Specific Risks (India Focus)

India imports a lot of silver, around 80 to 90 percen,t which is about 3,000 to 4,000 tonnes every year. This is putting a strain on the balance of payments in India, especially when the value of the rupee is falling. In the year 2025 the bill for importing silver was really high it was over 3 billion dollars. The Securities and Exchange Board of India or SEBI for short made some changes to the positions, on the Multi Commodity Exchange or MCX. They increased the lot sizes by 20 percent, which is making it harder for people to trade silver on the MCX.

Source: Gold and Silver Rally, Reuters

8. Future Outlook and Economic Implications

8.1 Market Outlook

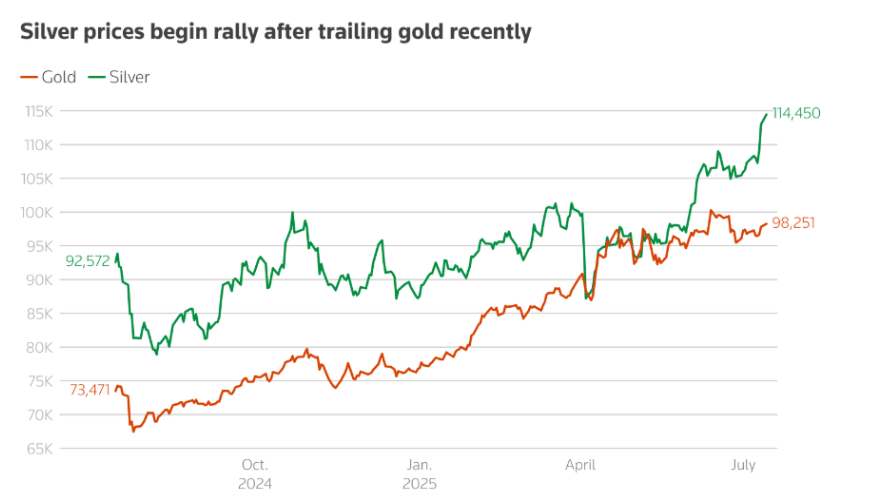

Silver demand continues to accelerate, outpacing stagnant global mine production and creating potential supply shortages. Executives warn that without intervention, constraints could intensify as industrial use dominates. While the provided sources focus more on investment and recycling, broader trends point to sustained pressure from electronics and renewables, positioning silver as a high-return asset nearly doubling gold’s gains over the past year.

8.2 Implications for Investors

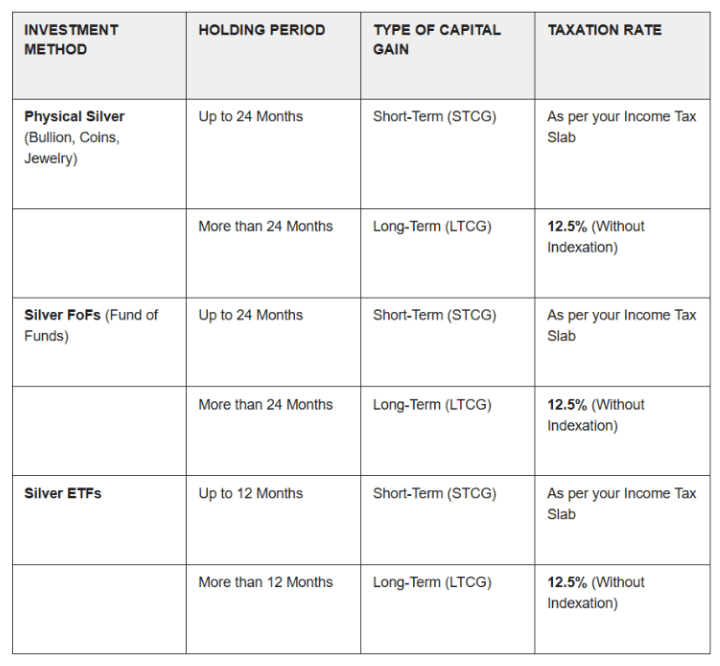

Silver has delivered a stronger risk-return profile than gold, with global prices rising around 130-140 percent over the last year compared to gold’s price rising by roughly 75 percent. This has drawn investor interest looking for opportunities to catch up at relatively lower entry levels. From a tax perspective, long-term investors benefit by holding physical silver for more than 24 months, which qualifies for long-term capital gains tax at 12.5 percent. Short-term traders often prefer MCX futures due to higher volatility, but these gains are taxed as per income slabs under short-term capital gains.

In India, buying physical silver such as coins, bars, or jewelry attracts 3 percent GST on purchase, along with 5 percent GST on making charges in the case of jewelry. Physical holdings also involve storage and insurance costs, which do not apply to paper-based options. Silver ETFs are taxed like equity mutual funds, with long-term gains applicable after 12 months. The image attached below explains this.

Source: Zerodha Fund House- How silver is taxed in India (Jan 23rd, 2026)

8.3 Gold-Silver Dynamics in Indian Financial Markets

Silver is emergingly being viewed as “new gold” for investors who missed earlier rallies. Its higher recent returns have encouraged substitution, particularly among price sensitive investors. Digital platforms such as MMTC-PAMP’s gold and silver offerings on Amazon and Flipkart have made access easier, while traditional demand through jewelry and loan markets continues.

8.4 Monetary Policy and Precious Metals Outlook

Expectations around US Federal Reserve rate cuts could further support silver prices, as lower rates usually boosts industrial metals and investment demand. In India, the RBI’s accommodative stance helps sustain interest in precious metals as portfolio hedges. Persistent inflation in emerging markets encourages allocation to real assets, strengthening silver’s appeal. There is no wealth tax on silver holdings, although large positions remain subject to disclosure requirements.

9.Conclusion

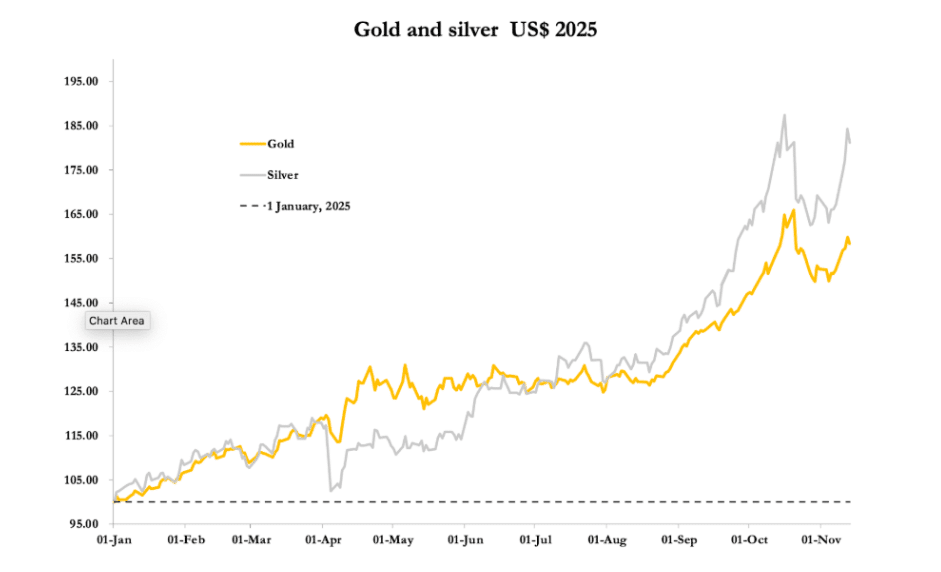

Silver has evolved from a purely monetary relic into one of the most strategically important commodities of the modern economy. A review of the evidence suggests that silver’s role is expanding on multiple fronts simultaneously as an indispensable industrial input powering the green energy transition, AI infrastructure, and advanced electronics, and as a financial asset offering inflation protection, portfolio diversification, and accessible investment for millions of retail participants. In emerging markets like India, silver occupies a uniquely democratic position, bridging rural households seeking affordable wealth storage and urban investors chasing higher returns than gold can offer. Its five consecutive years of supply deficits, persistent structural shortfalls, and 120% price surge in 2025 collectively signal that this is not a cyclical phenomenon but a long-term realignment of supply and demand fundamentals.

Yet, there is no consensus that silver is a risk-free opportunity. Rigorous analysis reveals genuine vulnerabilities: its by-product supply structure means production cannot respond swiftly to demand spikes, leaving markets chronically tight. Price volatility amplified by speculative flows, leverage, and currency movements can be punishing for retail investors, particularly those using MCX futures without adequate risk management. India’s heavy import dependence, high taxation, and underdeveloped silver-backed financial products further limit its accessibility and efficiency as an asset class.

In sum, silver is arguably one of the most compelling but complex investment and industrial commodities of the current decade. It empowers green technology, supports financial inclusion through affordable investment, and offers superior near-term returns relative to gold but it equally demands caution around volatility, over-leverage, regulatory gaps, and speculative excess. For investors and policymakers alike, the lesson is one of balance: integrate silver into diversified portfolios and industrial strategies, but within a framework that accounts for its structural risks. Future developments, such as technological substitution research, expanded recycling infrastructure, broader silver-backed financial products, and clearer regulatory frameworks offer meaningful promise in making silver’s gains more durable and broadly accessible. Continued monitoring of supply chain dynamics, particularly against the backdrop of US-China geopolitical competition over critical minerals, will be essential. Silver’s story ultimately underscores a broader truth: a commodity sitting at the intersection of industrial necessity and financial speculation can generate extraordinary value, but realising that value sustainably requires informed strategy, sound regulation, and a long-term perspective.

References

- Chacko, K. (2026). India gold market update: Enduring demand strength. Goldhub (World Gold Council Insights), January 16, 2026. World Gold Council. https://www.gold.org/goldhub/gold-focus/2026/01/india-gold-market-update-enduring-demand-strength

- Baker Steel Capital Managers LLP. (2026, January 21). Outlook 2026 – Miners in the spotlight: Are we at the start of a multi-year upcycle for commodities? https://www.bakersteelcap.com/2026/01/21/outlook-2026-miners-in-the-spotlight-are-we-at-the-start-of-a-multi-year-upcycle-for-commodities/

- CEIC Data. (2025). China’s decade of gold purchases as bullion keeps breaking records. https://info.ceicdata.com/chinas-decade-of-gold-purchases-as-bullion-keeps-breaking-records

- FXStreet. (2025, September 16). How will Fed rate cuts impact gold and silver? Hint: Pay attention to real interest rates. https://www.fxstreet.com/analysis/how-will-fed-rate-cuts-impact-gold-and-silver-hint-pay-attention-to-real-interest-rates-202509161325

- GoldSilver. (2026). Fed cuts rates as silver soars past $62. https://goldsilver.com/industry-news/goldsilver-news/fed-cuts-rates-as-silver-soars-past-62/

- GoodReturns. (2024, December 5). Gold rate in India rallies; silver price falls as RBI slashes repo rate. https://www.goodreturns.in/news/gold-rate-in-india-rally-silver-price-today-falls-as-rbi-slashes-repo-rate-on-december5-check-22k-24-1474481.html

- Strategic Gold. (n.d.). Gold and U.S. interest rates. https://www.strategicgold.com/white-papers/gold_and_us_interest_rates.pdf

- TradingKey. (2026). 2026 silver physical squeeze: Strategic asset outlook. https://www.tradingkey.com/analysis/commodities/metal/261487879-2026-silver-physical-squeeze-strategic-asset-tradingkey

- Upstox. (n.d.). Understanding the relationship between silver rate and interest rates. https://upstox.com/learning-center/online-trading/understanding-the-relationship-between-silver-rate-and-interest-rates/article-1324/

- World Gold Council. (2025, November). China gold market update: October’s unseasonable strength. https://www.gold.org/goldhub/gold-focus/2025/11/china-gold-market-update-octobers-unseasonable-strength

- Zerodha Fund House. (2026). How is silver taxed in India: ETFs, FoFs and physical silver? zerodhafundhouse.com

- KPMG. (2024). Energy transition investment outlook. assets.kpmg.com

- Vajiram & Ravi. (2025). Why silver soared 160% in 2025: Key drivers behind the silver price rally.vajiramandravi.com

- The Silver Institute. (n.d.). Silver in industry. https://silverinstitute.org/silver-in-industry/

- The Silver Institute. (2024). Silver is a highly strategic asset for institutional investors seeking diversification and risk reduction. silverinstitute.org

- The Silver Institute. (2025). Silver demand forecast to expand across key technology sectors. silverinstitute.org

- IndiaGraphs. (2025). Silver price history in India. indiagraphs.com

- Achintya Financial Services. (8 Aug 2025). Comprehensive analysis on silver. Achintya Comprehensive Analysis on Silver Report

- The Silver Mountain. (2025). The future of silver in the energy transition. https://www.thesilvermountain.nl/en/silver/the-future-of-silver-in-the-energy-transition

- Lansdown, A. B. G. (2007). A review of the use of silver in wound care: Facts and fallacies. British Journal of Nursing Monograph. https://pmc.ncbi.nlm.nih.gov/articles/PMC2364932/pdf/MBD-01-467.pdf

Recent Comments