Abstract

The Indian Banking Sector has always been a vital part of the country’s growth and financial stability. However, the recent rise in the number of financial frauds in this sector has raised serious questions on corporate governance, regulatory oversight, and risk management practices of both Banking and Non- Banking Financial Institutions. The High Profile Examples of Yes Bank, DHFL and IndusInd Bank reveal the structural weakness in the Indian banking sector. The purpose of this essay is to examine the origins, trends, and subsequent effects of financial fraud in India’s banking industry. The Reserve Bank of India’s (RBI) role in preventing banking frauds and evaluating the efficacy and efficiency of regulatory reforms implemented following the frauds is also highlighted in the article. In order to restore depositor confidence and protect financial stability, the study identifies policy measures that are focused on bolstering board independence, tightening auditor and rating-agency accountability, and improving early-warning systems.

Introduction

The banking sector is a central driver of India’s economic expansion. Empirical studies consistently find a positive relationship between banking depth and GDP growth, with the expansion of bank credit and financial inclusion initiatives contributing to India’s real growth rates of around 7 per cent in recent years. However, this growth‑enabling architecture is increasingly strained by systemic vulnerabilities: between FY 2023–24 and FY 2024–25, the Reserve Bank of India (RBI) recorded tens of thousands of fraud cases annually, with reported fraud amounts reaching approximately ₹13,930 crore in FY 2023–24 and surging to about ₹34,771 crore in FY 2024–25 based on the date of reporting. High‑value loan frauds, evergreening of stressed assets, and weak due diligence have been identified as key contributors to stressed assets and non‑performing loans. These loopholes not only impose high fiscal and quasi‑fiscal costs through recapitalisation but also undermine depositor confidence and impair the banking sector’s

ability to sustain inclusive, stable economic growth over the long run.

Concept of Financial Fraud in Banking

Financial fraud is a kind of financial crime involving the misuse of a financial institution or the services provided by it to steal money or assets. The most common types of fraud include Identity Theft, i.e., stealing personal data, loan fraud using fake documents, and phishing or online scams.

Understanding these criminal tactics is essential because, in the banking sector, fraud is formally classified as a critical component of operational risk. Although the terms ‘fraud’ and ‘operational risk’ tend to overlap, there is a distinct difference between them. Where operational risk refers to a broad category that includes losses from failed internal processes, systems, or human errors, Fraud is a specific, intentional subset of operational risk, where rules are broken for personal gain.

Modus Operandi of Banking Frauds in India

The modus operandi of banking frauds in India has shifted from simple theft to “financial engineering” and sophisticated digital exploitation. As of 2024–2025, the RBI reports a paradoxical trend: while the absolute number of fraud cases has decreased, the total value involved has nearly tripled to over ₹36,000 crore, driven by high-value corporate defaults and complex digital scams.

- Credit and Advances Fraud: Advances-related fraud remains the most lethal category, accounting for over 70% of the total value of fraud in Public Sector Banks and a significant portion in private lenders.

- Fund Siphoning via Shell Companies: This is the hallmark of the DHFL and Yes Bank cases. Borrowers create a web of hundreds of shell companies (e.g., DHFL’s “Bandra Books”, which allegedly managed 2.6 lakh fake loan accounts). Funds are disbursed to these entities as “loans,” only to be laundered back to the promoters for personal use or to buy luxury assets.

-

- Loan Evergreening (Zombie Lending): When a borrower is about to default, the bank provides a new loan to that same borrower or a related entity. This “fresh” money is immediately used to pay the interest on the old loan, keeping it “performing” on paper.

- Indirect Evergreening: A more sophisticated 2024–2025 trend involves using Alternative Investment Funds (AIFs). Banks invest in an AIF, which then invests in the “distressed” borrower. This masks the direct link between the bank and the bad loan, bypassing the RBI’s NPA classification rules.

- Technological & Cyber Frauds: Digital scams now comprise 81% of cases by volume, with phishing, UPI frauds, and malware siphoning funds rapidly. Insider trading leverages cyber tools, like IndusInd executives allegedly trading shares pre-accounting disclosure amid derivative lapses. Rise of “mule accounts” and API exploits in digital lending amplifies risks, demanding AI-driven monitoring.

- AI and Deepfakes: Scammers now use voice cloning and AI-generated video to impersonate senior bank executives or family members. In 2025, cases were reported where “Deepfake Video KYC” was used to open fraudulent accounts or authorise massive wire transfers.

DHFL CASE STUDY

One of the largest Financial Frauds in Indian history, the Dewan Housing Finance Corporation Limited (DHFL) scam, shows how shell companies and fake records can be used to trick the entire financial system.

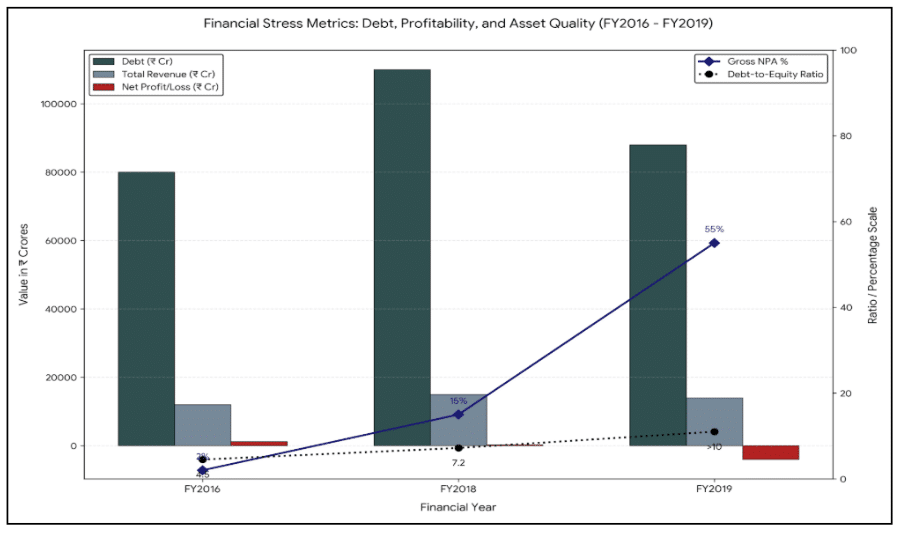

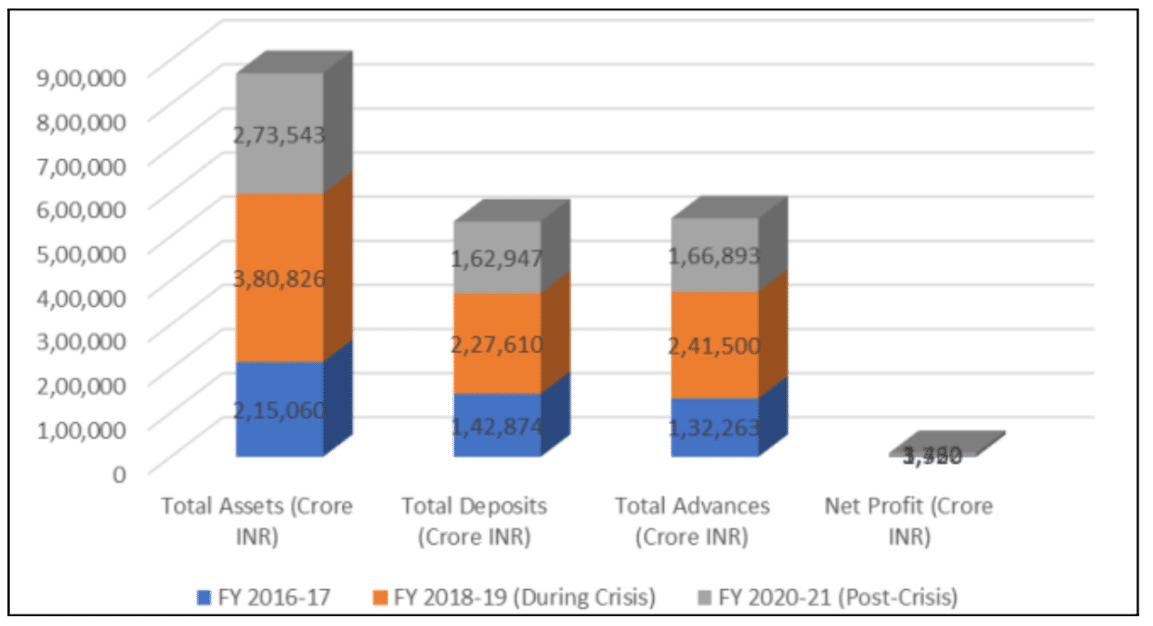

Background- Dewan Housing Finance Corporation Limited(DHFL), incorporated in 1984, was registered under the Companies Act 2013 as a non-banking financial company. DHFL mainly provided home loans to middle-class and poor families in rural and semi-urban areas. Being an NBFC (Non-Banking Financial Company), it didn’t just use its own money; it borrowed billions from big banks (like SBI and Union Bank) and took deposits from regular people to lend further. In the year 2017, DHFL was regarded as one of the most successful housing finance companies with its AUM (asset under management) valued at ₹1.01 trillion.

How the Fraud Worked- The Fraud came to light in 2019 when Cobrapost, a small media company, revealed evidence-backed allegations against DHFL. It reported a massive financial scam to the tune of over ₹31,000 crore, which was executed through a clever but illegal plan:

- The Fake Bandra Branch: The promoters, the Wadhawan brothers, created a fake, “ghost” branch in their computer system that didn’t exist in reality.

- 2.6 Lakh Fake Borrowers: They entered the names of over 2,60,000 people who supposedly took small home loans. Many of these were people who had already paid off their loans years ago.

- The Siphoning: While the books showed money going to thousands of regular people, the cash was actually being funnelled into 87 shell companies, meaning fake companies with no real business, owned by the Wadhawans.

- Round Tripping: Once the loan was given to these shell companies, the money from a shell entity’s bank account would later flow to DHFL-owned entities. This is termed round-tripping. The money was then used to buy private properties in Sri Lanka, India, Dubai, etc., give donations to political parties, and sometimes sent back to DHFL to show that “loans were being repaid.”

(Source – “The DHFL Scam: A Case of Regulatory Failure” (The Management Accountant Journal, 2025, 60(5), 44–49)

Why Did No One Catch It?- The fraud went on for nearly a decade (2010–2019), but still didn’t catch someone’s attention because of the following reasons-

- Rating Agencies: They kept giving DHFL a “AAA” rating, the highest safety score, until just weeks before the collapse.

- Auditors: The people supposed to check the accounts failed to flag that the “Bandra Branch” was a fiction.

- Governance: The Wadhawan brothers held so much power that they could easily bypass internal checks.

The Collapse and Consequences- The exposure of the scam had the following repercussions-

- It not only led to a huge fall in DHFL stock prices, but the entire stock market suffered.

- Since the fraud had seriously affected the company’s liquidity position, the depositors weren’t able to withdraw their own hard-earned money.

- Other banks have invested around $3 billion in DHFL, which was later on, was misappropriated by the company, leading to huge losses for the lenders who ultimately house the money of the common public.

Conclusion – The huge financial fraud made people doubtful of parking their surplus funds in banks and NBFCs. The overall credibility of the whole Financial System suffered a setback. The case reemphasised the need for proper checks and audits by the government in this sector. Also, it is needed to make sure that directors and promoters are more accountable than before and have transparent working. All those wrongdoings that paved the way for the fraud need to be rectified to once again instil the public’s faith in the Indian Financial System.

YES BANK CASE STUDY

Context and prelude to the crisis- Since its founding in 2004, Yes Bank has established itself as a rapidly expanding private sector bank with a robust corporate lending franchise. Under Rana Kapoor’s leadership, Yes Bank took small steps in building its corporate lending segment and focused on sectors like real estate, Internet Banking, Mobile Technologies, Pharmaceuticals, Renewable energy, Electricals, and Media (Ayush Kumar, 2021). This led to rapid growth, but at the same time, the bank was vulnerable to financial volatility as it had overexposed itself to risky clients. Although the bank initially reported strong profitability and asset quality, RBI inspections later discovered that exposures were heavily concentrated in stressed corporate groups and that non-performing assets (NPAs) were being underreported.

Fraud mechanism: The relationship between Yes Bank and DHFL

The relationship between Yes Bank and DHFL is widely viewed by investigators as a classic “kickback” scheme involving a massive exchange of favours. In 2018, despite clear warning signs that DHFL was struggling financially, Yes Bank invested roughly ₹3,700 crore into the company’s short-term debt. Shortly after this investment, DHFL “returned the favour” by granting a ₹600 crore loan to DOIT Urban Ventures, a private firm owned by the family of Yes Bank’s co-founder, Rana Kapoor. The CEO’s dishonest “this-for-that” transactions and careless, high-risk lending were the main causes of Yes Bank’s crisis. The bank’s management disregarded risks and used false reporting to conceal growing losses. Financial stability and regulatory trust ultimately collapsed as a result of this poisonous combination of lax oversight, concealed bad loans, and ineffective internal controls.

(Source – Yes Bank crisis timeline (Himanshi et al. 24). From the International Journal of Management and Commerce.)

Investigation and consequences

The Central Bureau of Investigation (CBI) and Enforcement Directorate (ED) claim that the ₹600 crore loan to DOIT Urban Ventures was secured by agricultural land whose actual value was significantly less than the inflated valuation used to support the sanction. This indicated quid-pro-quo behaviour rather than true lending, making the loan practically unsecured and commercially unjustifiable. Further probes traced additional suspicious transactions involving real‑estate developers and group companies. ED statements on the case refer to total “proceeds of crime” of around ₹4,300–5,500 crore connected to the Yes Bank–DHFL nexus, reflecting the scale at which funds were allegedly diverted from legitimate banking to fraudulent channels. The RBI superseded Yes Bank’s board, appointed an administrator, and placed a moratorium on the bank on March 5, 2020. Withdrawals were initially limited to ₹50,000 per depositor. The Government of India and RBI then notified the Yes Bank Reconstruction Scheme 2020. Under this plan, State Bank of India (SBI) and several other domestic banks injected fresh equity of around ₹10,000 crore, with SBI taking up to 49% stake subject to a minimum 26% holding for at least three years.

Need and Significance of the Study-In the banking sector, the Yes Bank crisis revealed severe deficiencies in risk management, anti-money laundering (AML) compliance and corporate governance in the banking sector. Learning from the root causes of the crisis, including lenient lending to low-quality borrowers, weak in-house checks, and slow-moving regulatory action, is also key to being more-focused.

INDUSIND BANK CASE STUDY

Unlike the other two case studies with a classic promoter- bank quid pro quo, this financial fraud is more about accounting manipulation, compliance failures, and weak internal control.

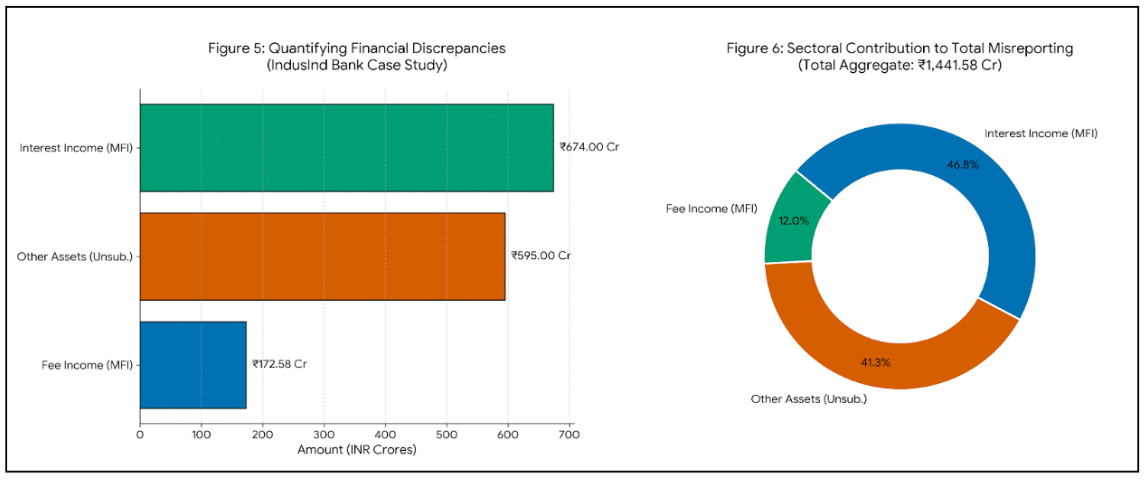

In the financial year 2025, the internal audits and whistleblower complaints revealed that INDUSIND, India’s fifth-largest private bank, suspected a severe internal fraud involving senior executives, marked by an accounting discrepancy of ₹2,600 crore and a quarterly loss of ₹2329 crore.

The Roots of the Crisis– Back in 2021, Bharat Financial Inclusion Ltd. (BFIL), its subsidiary, was reported as masking the true status of stressed loan accounts. A “Technical Glitch”, as per the bank, led to the disbursement of 84000 loans without the customer’s consent. As per the allegations, the bank resorted to “Ever-Greening” to present a cleaner loan book amid the COVID-19 pandemic. Though the bank claimed a technical error, later the internal investigation revealed that the pressure to achieve aggressive growth rates was one of the reasons.

Deepening Financial Irregularities

The problem took a bigger face in the year 2025 when the regulatory audits revealed-

1) Forex Hidden Losses:- It was discovered that nearly Rs 1979 crore loss from trading in foreign exchange was kept hidden for years.

2) Income Inflation:- To make the bank look more profitable, nearly Rs 846 Crores was overstated in the interest.

(Source – “Bajaj Broking.” IndusInd Bank Reports Suspected Fraud Involving Rs.1,442 Crore in FY25)

Leadership and Regulatory Fallout

The scandal led to a massive shake-up. As a result, the Reserve Bank of India (RBI) and the Serious Fraud Investigation Office (SFIO) had to step in. Furthermore, the revelation of these window-dressed accounts led to the resignation of many top-level executives, including CEO Sumant Kathpalia.

Current Status of Customers

As of 2026, the bank has been forced to clean its books. Though this has led to a drop in the bank’s profitability, RBI ensured the bank remains liquid, meaning individual savings and deposit accounts remain safe. The focus has shifted to “Rajiv Anand’s” new leadership to restore trust through stricter auditing.

Impact of Banking Frauds on the Economy

Banking fraud in India is not merely a balance sheet issue; they are macroeconomic shocks that reverberate through the lives of citizens and the stability of the national economy.

- Impact on Depositors and Investor

The most immediate victims of banking fraud are the retail depositors and small-scale investors.

- Liquidity Freeze: Depositors often lose access to their own savings for months. Even with the DICGC insurance limit of ₹5 lakh, those with larger life savings (pensioners, SMEs) face devastating capital loss.

- Investor Wealth Erosion: Fraudulent revelations lead to a “blood bath” in the stock market. For example, during the IndusInd and Yes Bank crises, market capitalisation worth billions was wiped out in days, hurting retail shareholders and mutual fund investors.

- Impact on Financial Stability

- Systemic Risk & The “Provisioning Trap”: RBI rules require banks to set aside 100% of the stolen amount to cover losses (called “provisioning”). In 2025, with ₹18,674 crore flagged as fraud, that’s billions of rupees locked away in a “safety vault” instead of being lent out. Because of the credit multiplier, every ₹1 lost to fraud can mean ₹8–10 less available for public loans.

- The “Credit Squeeze” on Industry: Scared of being blamed for future “legacy frauds,” bankers become overly cautious. This “Credit Squeeze” makes it incredibly difficult for honest businesses (especially small ones) to get funding. Growth stalls because the system prioritises “playing it safe” over fueling the industry.

- Loss of Public Trust in Banking Institutions

Trust is the “intangible collateral” of the banking sector. Once breached, the damage is long-lasting.

- Flight to Safety: Frequent frauds in the private sector (like the IndusInd accounting discrepancies) trigger a “flight to safety,” where depositors panic and move funds to the “Too Big to Fail” Public Sector Banks (PSBs). This creates an unhealthy imbalance in the market.

- Fiscal Burden on Government and RBI

The state eventually becomes the “lender of last resort,” and the taxpayer often picks up the tab. When private safeguards fail or public assets are looted, the financial vacuum is filled by the public exchequer.

- Recapitalisation Costs: Since the government owns Public Sector Banks (PSBs), it is responsible for their health. When these banks lose billions to fraud (like the ₹25,667 crore lost recently), the government pumps in fresh cash. This “new” money often comes from taxpayer funds.

- Indirect Recapitalisation (The “White Knight” Burden) – Sometimes, instead of giving cash directly, the government asks a healthy state-owned institution to “save” a failing private bank. How it works: A strong entity is forced to buy shares in a weak, fraud-hit bank. The Burden: This protects the banking system, but it weakens the “White Knight” (the saviour), as they are now tied to a sinking ship.

Role of RBI and Regulatory Framework

Formed in 1935, RBI is the primary watchdog of the Indian financial system that ensures banks operate safely to protect depositors’ money.

It supervises using a Risk-Based Supervision (RBS) approach, i.e., more resources are allocated to the institutions with high risk profiles. The higher the risk, the closer the supervisory attention.

The Prompt Corrective Action (PCA) framework is designed to help a bank when it shows signs of financial ill health, to prevent it from collapsing. If a bank’s financial health, indicated by factors like NPAs or Capital, deteriorates, RBI imposes certain restrictions like stopping dividend payments, restricting branch expansions, limiting high-risk lending, etc., on the bank to prevent major failure.

1. The RBI is closing the “detection lag”

- Early Warning Signals (EWS): Banks must now use automated “smoke detectors” built into their systems to catch red flags instantly.

- The 14-Day Rule: Any fraud over ₹25 lakh must be reported to the RBI within two weeks.

- Right to be Heard: Following a 2025 mandate, 122 “legacy” fraud cases (totalling over ₹18,000 crore) were re-examined. This ensures transparency by giving borrowers a fair chance to explain themselves before being labelled “fraudulent.”

2. Banking Laws (Amendment) Act, 2025

This law was passed to clean up how banks are managed:

- “Fit and Proper” Directors: The rules for who can lead a bank have been tightened to stop corporate “insiders” from having too much influence.

- Tenure Limits: Non-executive directors can now serve a maximum of 10 years to ensure fresh, independent oversight.

- Substantial Interest: The threshold for what counts as a “major” financial stake was raised from ₹5 lakh to ₹2 crore, modernising a limit that hadn’t changed since 1968.

3. Digital Payments Intelligence (DPIP)

Launched in 2025, the DPIP is a national AI network. It doesn’t just look at numbers; it looks at behavioral biometrics. If a transaction happens with a “typing rhythm” or “navigation flow” that doesn’t match yours, the system flags it as a potential hack before the money is even sent.

Conclusion

The rise of financial fraud in India’s banking sector stems not merely from rogue individuals but from entrenched structural incentives, like lax oversight in rapid digital expansion, and institutional weaknesses in both scheduled banks and shadow banking entities. Cases like DHFL’s ghost-branch loan fabrication, Yes Bank’s collusive lending nexus with borrowers, and IndusInd’s internal microfinance manipulations collectively expose a fraud spectrum spanning NBFC opacity, inter-institutional dependencies, and accounting deceit. Sustainable banking growth in India will require more than just technological innovation. It demands a delicate balance between digitalisation and deep regulation. Moving forward, the focus must shift from “recovery” to “prevention”, leveraging AI-driven surveillance and transparent governance to ensure that India’s path toward a $10 trillion economy is built on a foundation of trust, rather than a bubble of hidden risk.

References

Moneylife (2022), “IndusInd Bank’s Rs1,520 Crore Shock: Accounting Flaw or Governance Failure?”, Moneylife Magazine. Available at: https://www.moneylife.in/article/indusind-banks-rs1520-crore-shock-accounting-flaw-or-governance-failure/76636.html

Case-study style analysis: “Yes Bank crisis: A case study on lapses in anti‑money‑laundering and internal controls” (Management Journal, 2025).

https://managementjournal.in/assets/archives/2025/vol7issue2/7015.pdf

DHFL fraud and gatekeepers: “DHFL Fraud Uncovered: It’s Time to Make the Gatekeepers Pay” (Once in a Blue Moon, 2025).

https://onceinabluemoon2021.in/2025/07/30/dhfl-fraud-uncovered-its-time-to-make-the-gatekeepers-pay/

NIBM Working Paper, “Bank Frauds in India” – conceptual overview, RBI data analysis, fraud typologies, and causes within Indian banks.

https://www.nibmindia.org/static/working_paper/NIBM_WP35_DRSL.pdf

“Corporate Governance Failure: An Overview of the New Generation Bank Fraud – Yes Bank Case”, IJRTI, 2025 (focus on governance lapses and impact).

https://www.ijrti.org/papers/IJRTI2504206.pdf

IJNRD article, “Analyzing Bank Frauds in India” – empirical discussion of major loan fraud cases, modus operandi (diversion of funds, forged statements), and control failures.

https://ijnrd.org/papers/IJNRD2409177.pdf

“An Empirical Study on Indian Banking Scams by Top Business Holders” discusses big-ticket borrower frauds, political influence, and weak supervision.

https://www.icommercecentral.com/open-access/an-empirical-study-on-indian-banking-scams-by-top-business-holders.php?aid=92211

Recent Comments