Introduction

The global financial system is changing dramatically with the rise of digital money, which serves as both a complement and an alternative to traditional fiat currencies. What was once a niche interest for tech enthusiasts has now become a primary concern for policymakers, central bankers, and major international organizations. Cryptocurrencies, stablecoins, and central bank digital currencies (CBDCs) are altering the conversation about money’s nature, the role of banks, and the level of sovereign control over economies.

This change is fueled by technological advancements, shifting social attitudes, and global competition. As barriers to instant, borderless transactions disappear, national governments face new challenges to financial oversight.

At the heart of these developments is a simple yet significant question: Does the rise of digital money ultimately strengthen or weaken central bank power? Addressing this question requires a clear understanding of monetary sovereignty, careful evaluation of the risks and opportunities posed by private digital currencies, and thoughtful consideration of how CBDC development fits into this new landscape.

Central banks now find themselves in a world where private innovation can quickly change consumer behavior. The rapid global acceptance of digital money is prompting authorities to rethink their control models.

Policymakers must urgently adjust regulations and institutional frameworks to maintain monetary stability. The outcome of these efforts will have lasting effects beyond just the monetary realm.

Understanding Monetary Sovereignty

Monetary sovereignty means a country’s ability to manage its own currency, independently set monetary policy, and regulate the money supply within its borders. This sovereignty is a key part of governmental power, enabling states to shape economic conditions and ensure overall economic stability.

Historically, central banks have maintained this authority by using policy tools like interest rate changes, liquidity injections, and foreign exchange market interventions. These actions directly affect inflation, stimulate economic activity, and help during crises.

For example, the U.S. Federal Reserve’s significant interest rate cuts during the 2008 financial crisis, or the Reserve Bank of India’s strategic actions to manage the value of the rupee, highlight the essential role of central banks in managing national economies.

This economic power also supports broader state sovereignty by ensuring control over cross-border transactions, protecting against foreign shocks, and promoting national economic goals.

However, the rise of digital currencies has raised concerns about whether central banks can maintain control over the creation and circulation of money, especially as alternative mechanisms gain ground. As societies become more interconnected and money circulates beyond physical borders, maintaining monetary sovereignty becomes more complex for policymakers.

The Advent of Private Digital Currencies

The first significant challenge to monetary sovereignty in the internet age appeared with cryptocurrencies like Bitcoin and Ethereum. These digital assets operate outside traditional banking systems, relying on cryptography and distributed ledger technology rather than central authorities.

Their global availability and independence from national regulations draw users in countries facing inflation or unreliable fiat money. They offer anonymity, lower barriers to entry, and the ability to bypass conventional financial regulations.

However, this very independence also brings serious risks. The volatility of these cryptocurrencies undermines their reliability as stable units of account, causing uncertainty for businesses and consumers. As cryptocurrencies become more popular, central banks may struggle to regulate the money supply and practice effective monetary policy.

Stablecoins have emerged to address some of these volatility issues, aiming to provide tokens tied to sovereign currencies like the U.S. dollar or euro. Despite this, their widespread use could still lead to regulatory confusion and, in some instances, replace government-issued money with alternatives managed by private entities.

Technological advancements like cryptocurrencies and stablecoins have empowered private organizations to issue financial instruments, a function traditionally reserved for governments.

This shift changes the dynamics of money creation, raising questions about accountability, regulatory oversight, and the long-term stability of the financial system.

Central Bank Digital Currencies (CBDCs)

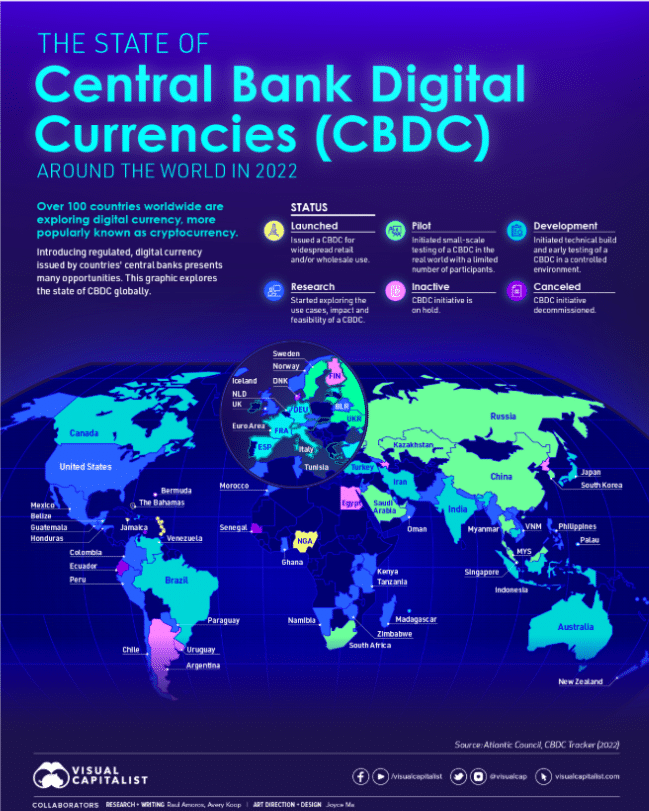

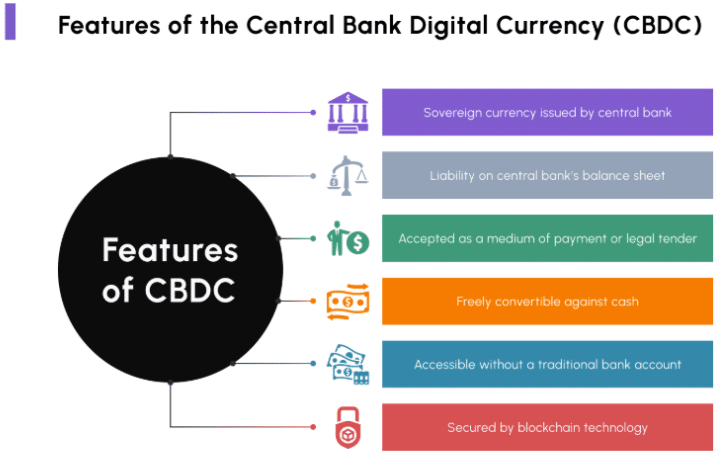

In response to the growing popularity of private digital currencies, governments around the world are quickly developing central bank digital currencies (CBDCs). Unlike decentralized cryptocurrencies, CBDCs are official digital forms of state currency, maintained and controlled directly by central banks.

These currencies aim to offer the convenience, efficiency, and speed of modern payment technologies while retaining the trust and stability of government-backed money. CBDCs can be programmed, allowing for new approaches to monetary interventions and improved policy effectiveness.

Developed countries primarily see CBDCs as ways to enhance payment systems, decrease reliance on private intermediaries, and protect monetary independence amid rapid digital change. In contrast, developing countries view CBDCs as key tools for improving financial inclusion and providing banking services to unbanked populations.

Several examples illustrate this trend: China’s digital yuan (e-CNY) is already operational in multiple provinces, establishing China as a leader in digital currency strategy. Nigeria’s eNaira aims to provide financial access to a wide segment of its cash-dependent population. The European Central Bank’s Digital Euro initiative represents a cautious yet determined effort to keep the euro significant in a changing global financial environment.

More than just technological advancements, CBDCs signify strategic decisions by central banks to remain relevant and effective in an era of rapid innovation. Their implementation is widely viewed as necessary to maintain public trust and reinforce state authority in a digitizing world.

Beyond domestic consequences, widespread CBDC adoption could create new standards for cross-border transactions and change how money flows globally.

Implications on Central Bank Power

The rise of digital money complicates traditional central bank authority. CBDCs allow central banks to provide digital cash directly to the public, eliminating intermediaries and boosting both efficiency and transparency in monetary operations.

A direct digital currency system can enhance central banks’ ability to monitor transactions, enforce negative interest rates, and target specific policy outcomes. Increased transparency enables authorities to trace funds and potentially prevent unlawful activities.

However, these digital currencies also introduce new risks. If individuals or businesses shift large amounts of bank deposits into CBDCs, commercial banks may struggle to attract funds for lending, increasing the risk of financial instability or credit shortages. In times of economic stress, quick digital withdrawals could suddenly cause bank runs, heightening systemic risks.

CBDCs must be carefully designed to balance the perks of direct access and oversight with the need to maintain banks’ roles in creating credit. Central banks will need to oversee these changes closely, ensuring digital innovation does not inadvertently harm overall financial stability.

Ultimately, the impact of digital money on central bank power will rely on its design, adoption speed, and integration with existing economic systems. Coordinated regulation and adaptable policy frameworks are crucial for managing these evolving dynamics.

Global Competition and Monetary Sovereignty

Digital currencies are ushering in a new era of global economic and geopolitical competition. The U.S. dollar maintains a dominant position in international trade and finance, and the fact that most stablecoins are pegged to the dollar enhances its influence in the digital sphere.

Simultaneously, countries like China are promoting their digital currencies, like the e-CNY, to advance national interests and boost currency influence in international trade. The pilot program for e-CNY has already processed over 1.8 trillion yuan (about USD 250 billion), showcasing China’s ambition to influence the future of global payments.

Innovative payment systems, such as the mBridge project initiated by central banks in China, Hong Kong, Thailand, and the UAE, highlight the potential for new infrastructure that sidesteps traditional systems like SWIFT. These efforts aim to reduce dependence on Western-dominated financial systems and create more resilient networks for international payments.

If these alternative networks gain traction, they could diminish the power of established monetary authorities and disrupt the existing order in global finance. Currency blocs might form around dominant CBDCs, changing trade flows, investment patterns, and international relations.

In essence, digital currencies are not simply technical tools, but also instruments of geopolitical strategy. Countries that successfully create trusted and widely accepted digital currencies could strengthen their monetary sovereignty, while others might lose control to privately or foreign-regulated currency systems.

Challenges and Risks

Digital currencies offer significant potential, yet their implementation comes with unique challenges and risks.

Cybersecurity is a major concern, as these systems rely entirely on secure digital infrastructure. Breaches or hacking incidents can quickly damage public trust and disrupt the economy. Financial stability is another issue; if funds shift too rapidly from commercial banks to CBDCs, this could hinder lending and negatively affect investment and economic growth.

Privacy concerns must also be considered. While CBDCs enhance transparency, they might enable governments to monitor all transactions, raising worries about surveillance and citizens’ rights. Implementation must strike a balance between oversight and protecting privacy.

Digital exclusion presents a barrier as well. Many individuals in developing countries lack access to smartphones or the internet, limiting their ability to engage in digital currency systems. For instance, Nigeria’s eNaira has reached less than 1% of the population, demonstrating the challenges of driving meaningful adoption.

These risks emphasize that digital money signifies more than just a technological advancement; it marks a shift in how money functions in society. Thoughtful planning and strong policy design will be key to ensuring success and avoiding destabilization or inequality.

The Road Ahead

The future of digital currencies will hinge on central banks’ ability to manage innovation wisely and proactively. Active pilot projects are underway worldwide, testing how CBDCs can be safely integrated into current financial systems. Lessons learned from early adopters, such as China’s digital yuan or India’s e-rupee, which has seen ₹1,000 crore worth of transactions in two years, are informing policy discussions.

Success will rely on building strong public trust, ensuring fair access for all citizens, and maintaining the stability of financial markets. Without these safeguards, risks like bank disintermediation, rapid crises, or loss of confidence could overshadow potential gains.

Balancing technological innovation with solid economic management and clear communication is essential to keep digital money accessible and secure for diverse communities.

Central banks must also work together internationally to prevent cross-border disruptions and protect monetary sovereignty.

If policymakers find the right balance, digital currencies could enhance efficiency, lower costs, and promote financial inclusion. If they fail to do so, the risks of instability and weakened sovereignty could increase swiftly.

Conclusion

Digital money is fundamentally transforming global finance. Cryptocurrencies and stablecoins challenge the dominance of state-issued currencies, while CBDCs reflect central banks’ determined efforts to adjust and assert control. The future trajectory of these changes remains uncertain.

If managed effectively, digital currencies could improve the efficiency and inclusivity of monetary systems, reinforcing central bank authority in a rapidly changing world. On the other hand, poor management could weaken monetary sovereignty, increase inequality, and empower private or foreign-controlled currency systems.

The final result will depend on the political choices and strategic decisions made by governments and central banks today.

Looking ahead, the future of monetary sovereignty will depend on institutions’ ability to guide innovation while protecting stability, equity, and independence.

References

- Bank for International Settlements. (n.d.). Central bank digital currencies: foundational principles and core features. https://www.bis.org/publ/d85.htm

- International Monetary Fund. (2019, September 26). From stablecoins to central bank digital currencies. https://www.imf.org/en/Blogs/Articles/2019/09/26/from-stablecoins-to-central-bank-digital-currencies

- European Central Bank. (2020). Report on a digital euro. https://www.ecb.europa.eu/pub/pdf/other/Report_on_a_digital_euro~4d7268b458.en.pdf

- International Monetary Fund. (2019). The rise of digital money (Working Paper No. 19/?). https://www.imf.org/en/Publications/WP/Issues/2019/07/12/The-Rise-of-Digital-Money-47097

- World Economic Forum. (2020). Global stablecoin policy framework. https://www.weforum.org/reports/global-stablecoin-policy-framework

- People’s Bank of China. (n.d.). Digital currency electronic payment (DC/EP). https://www.pbc.gov.cn/en/3688110/3688183/index.html

- Central Bank of Nigeria. (2021). eNaira design paper. https://www.cbn.gov.ng/Out/2021/CCD/eNaira%20Design%20Paper.pdf

- International Monetary Fund. (n.d.). Global Financial Stability Report. https://www.imf.org/en/Publications/GFSR

- Bank for International Settlements. (2021). Annual economic report 2021. https://www.bis.org/publ/arpdf/ar2021e3.htm

- Bank for International Settlements. (2021). Central bank digital currencies: A framework for assessing why and how. https://www.bis.org/publ/work976.pdf

- Yu, S., & Zhu, H. (2021). Session 3 paper — digital finance and macroeconomics. Bank of England. https://www.bankofengland.co.uk/-/media/boe/files/events/2021/july/chief-economists-workshop/session-3-paper-yu-zhu.pdf

Recent Comments