What are Corporate Debt Markets?

Corporate Debt Markets are financial markets where businesses raise funds by offering investors debt instruments in exchange.

The securities, including bonds, debentures, commercial papers, etc., are issued to the investors in return for periodic interest payments and the principal amount at maturity.

Role of Corporate Debt Markets in the financial ecosystem

Revisiting the Mexican Debt Crisis of 1982 where the corporate debt market came into play: During the 1970s, to fund infrastructural development, Mexico and other Latin American countries took on substantial debt from international banks. Since the funds were borrowed in foreign currency, majorly U.S. dollars, it caused deep economic trouble for Mexico to pay back the loan when the oil prices crashed, affecting their major revenue source, and U.S. interest rates surged. The appreciation of the U.S. dollar in the early 1980s made it even more difficult for Mexico to repay its debts, instigating a domestic and an international crisis.

This pushed Mexico to seek alternative funding avenues to restructure its economy, resulting in the emergence of corporate debt markets.

Corporate debt markets allow companies to raise capital for their projects, funding expansion and acquisition, by selling bonds to a wider pool of domestic and international investors instead of turning to banks and foreign loans for borrowing.

This not only helps companies access capital in a diversified way, offering flexibility with interest rates, maturity, and repayment structure, but it also helps companies in longer-term financing and mitigate exchange rate concerns.

COVID-19 PANDEMIC

The pandemic triggered major disruptions in the financial ecosystem and the global economy. This led to significant instability in corporate debt markets and fostered new trends and structural shifts within the market post-pandemic.

Corporate Debt Markets- Pre-Pandemic Landscape

Cheap Borrowing

Before the Covid-19 pandemic, interest rates were low. This reduced the cost of borrowing and loans for businesses and helped them raise capital for expansion, growth, and refinancing old debts.

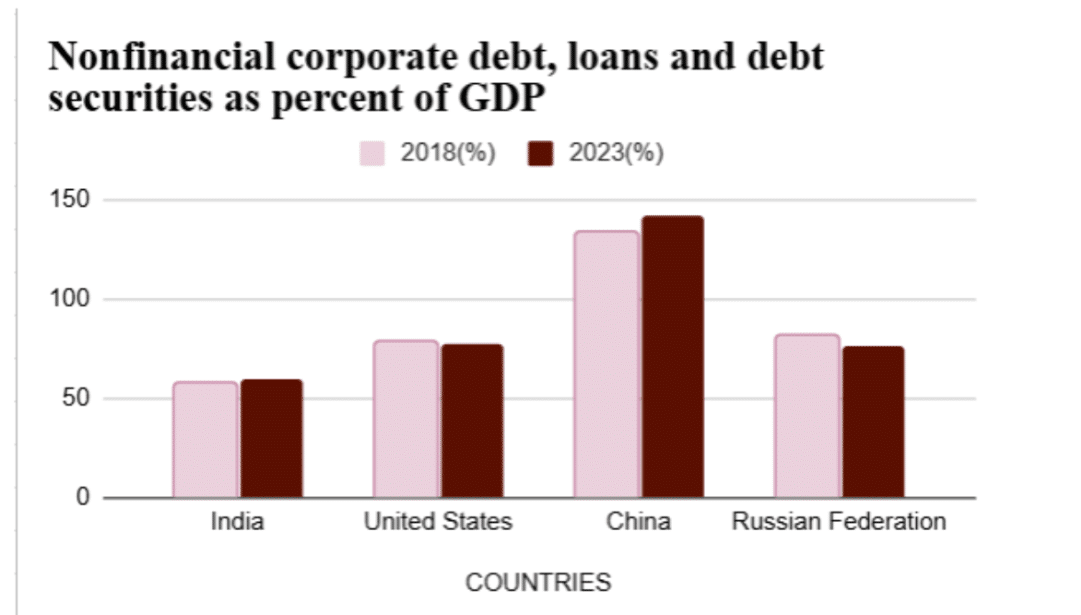

Rising Corporate Debt Levels

In developed economies like the U.S. and Europe, companies took on substantial debt, some to an extent that could be risky if their revenues declined. In many nations, corporate debt was growing faster than the economy.

Investors Loving Corporate Bonds

Investors desired better returns than low-interest savings accounts and hence preferred corporate bonds. Since investors were willing to take risks for higher returns, even riskier bonds became popular.

Prominence of Emerging Markets

Companies in developing countries like India, Brazil, and South Africa also began to raise capital through bonds. In order to mitigate exchange rate concerns, many businesses issued bonds in their local currency.

Covid-19 Pandemic Shock: Pandemic-Induced Disruptions in Corporate Debt Market

Liquidity Crunch

Imagine walking into a bank where everyone is trying to withdraw their money at once- the panic is real. That’s exactly what happened to businesses that relied on corporate debt.

Concerned about the uncertainty, investors pulled their funds from riskier assets, like corporate bonds, and transferred them to safer alternatives, leaving companies cash-strapped.

Increased Borrowing Costs

The cost of borrowing skyrocketed in such uncertain times. Since investors sought higher rates to take on the risk, companies that needed loans were suddenly faced with exorbitant interest rates and many businesses could not afford to climb the skyscraper-high cost of borrowing.

Defaults and Downgrades

With no income coming in due to lockdowns, many companies fell behind on their debt repayments. This caused bankruptcies and credit downgrades. As their credit ratings fell, securing new loans became more challenging.

Behavioral Disruptions: The Flight to Quality

In a state of panic, investors turned to government bonds for safety instead of the perilous realm of corporate debt. Companies that needed to borrow had fewer choices and the borrowing market became almost non-existent.

Panic in Credit Markets

Imagine the panic that would arise if you were attempting to purchase tickets for a concert that was already sold out!

As investors rushed to protect their own interests, companies needing credit were shut out and those depending on corporate debt suddenly found themselves nowhere to turn.

Surge in Credit Spreads

Credit spreads- the extra cost companies pay compared to government bonds, skyrocketed like never before.

Default Risks

A Domino Effect- a situation where one event triggers a chain reaction of similar events that successively affect one another.

Particularly for sectors like tourism and aviation, the default risk started to grow. When companies were unable to pay off their debts, the dominoes began to fall. As the number of defaults increased, the harder it became for others to escape the same fate.

From Crisis to Stability: Post-Pandemic Recovery

Post-pandemic, not only was there a recovery, but also a reinvention, and this development is still influencing how corporate debt will develop in the future. With the cresting of tumultuous financial markets, governments and central banks were left with little alternative but to intervene, thereby laying the groundwork for eventual recovery.

Phase 1: Immediate Response (2020-2021)

(A) Government Intervention

The corporate debt market was at the brink of collapse when the world went into lockdown. But in a classic crisis-response mode, governments across the globe sprang into action. As a result, central banks cut interest rates to historical lows, unleashed massive stimulus packages, and initiated bond purchases in order to inject liquidity into the markets.

For example, the U.S. Federal Reserve moved swiftly to introduce stabilization measures for the debt market that amounted to bringing interest rates nearly to zero and, on top of that, launching various bond-buying programs.

The government also provided loan guarantees and credit facilities so that the companies could have access to the vital funds they needed to survive difficult times. These initiatives created the stability needed to revive investor confidence.

(B) Dominance of Superior Companies

Who thrived in that havoc? Not every business was able to secure the necessary funding. Only those able to maintain good credit ratings, notably from tech, pharmaceuticals, and healthcare, could really raise any money. They reveled in the opportunity where risk-averse investors flocked to safe bets and issued bonds at extremely low rates to cushion their balance sheets.

Phase 2: Stabilization and Recovery (2021-2022)

(A) Rebounding Investors’ Confidence

As the world gradually opened its doors again, the corporate debt market was in tow. The vaccines were rolled out successfully and economies stabilized at a consistent pace. The hope of investors who had been holding caution in their hands revived in seeing the corporate debt market regain momentum. We saw a rise in bond issuance, especially from businesses that had done fairly well throughout the pandemic.

The first movers in the fray were the tech, e-commerce, and healthcare companies. They issued bonds to finance growth, acquisition, and innovation. These companies were not recovering- they were thriving in the new normal. What we saw was a change: the market didn’t just stabilize; it rose, with new opportunities in view.

(B) Increased borrowing- Why Companies Prefer Short-Term Debt?

This new optimism, however, did not lead to reckless borrowing. Companies leapt at the opportunity to take advantage of record-low rates, but they were careful to maintain that perspective, understanding the fragility of the global financial framework. Businesses continued to raise debt, but now with a twist; they desired short-term debt more than the long-term bonds. Why?

The companies wanted flexibility to pivot in case the future was uncertain. With businesses protecting themselves from erratic market shifts, short-term debt maturities became the norm.

Phase 3: Structural Adjustments (2022 onwards)

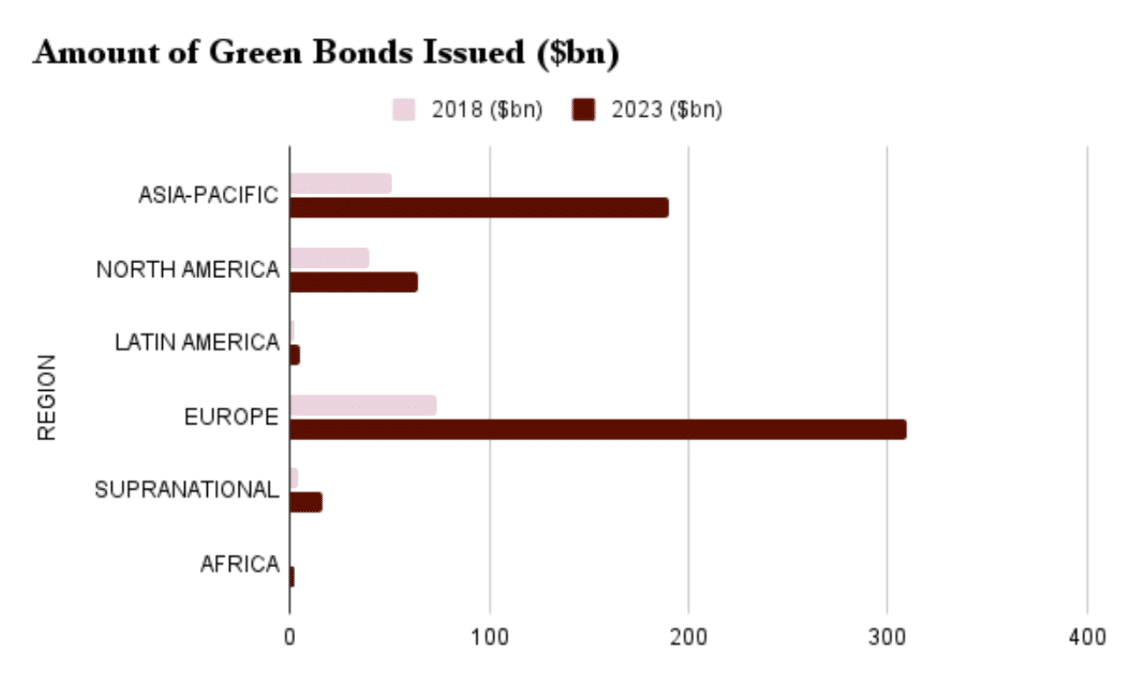

(A) Rise of ESG (Environmental, Social, Governance) Bonds

The real game-changer, however, came with a shift in investor values. Investors sought out businesses that adhered to sustainability and social responsibility as the pandemic underscored their crucial importance. ESG bonds are issued to fund projects that prioritize social justice, environmental sustainability, and sound governance. As institutional and retail investors sought more ethical investing options, ESG bonds quickly became essential to corporate debt portfolios.

In a post-pandemic environment, large firms and traditionally higher-risk industries realized that ESG bonds may help them not only raise capital but also rebuild their reputation.

With the advent of a new era of conscious capitalism, where sustainability was valued equally to financial returns, the corporate debt market had pivoted.

(B) Private Debt Markets

The corporate debt market also witnessed a remarkable shift towards private debt, concurrent with the growth of ESG bonds. As uncertainty began to strangle companies, the traditional public debt markets became a nightmare to negotiate. The answer? Private Debt Markets. Companies seeking stability and customized terms of these marketplaces found the funding options flexible and customizable.

It is with the realization that the private debt market, given that it has more personal structures, can provide much-needed capital in ways that public markets just cannot, that this development gathered speed.

(C) Financial Innovation and New Debt Instruments

The most exciting development of all was, in all likelihood, the soaring financial innovation from the pandemic. As the market evolved companies started looking for the emerging debt instruments.

Convertible bonds, which allow the option of converting debt into equity, became popular, especially in industries that are prone to mortality. Green bonds and hybrid securities have also become intriguing substitutes, capitalizing on the rising interest in investing in socially conscious companies.

Challenges and Risks in the New Era of Corporate Debt Markets

ESG Mandates

Post-pandemic, investors are demanding sustainable investments, which are forcing companies to issue ESG-compliant debt, such as green bonds and social bonds. This shift to sustainable operations comes at a cost and may not pay off directly, thereby leading some companies to stress financially. Companies that fail to comply with ESG requirements may lose out on capital.

Geo-political Tensions

Post-pandemic, the geopolitical risks comprising the Russia-Ukraine war, U.S.-China trade tensions, and disturbances in the supply chain have put corporate debt markets in a turbulent state. Companies operating in such sensitive regions face uncertainty and diminished investor confidence.

Regulatory Changes

Government and financial regulators are introducing stricter rules and regulations to prevent liquidity crises, which had already once happened during the pandemic. Stringent regulations may restrict the flow of capital into riskier bonds. This also increases the compliance costs as the companies are required to adjust their financing structures to comply with regulatory standards.

Opportunities for Growth of Corporate Debt Markets

Despite these challenges, corporate debt markets still hold potential opportunities. In fact, some of the challenges have stimulated innovation and new prospects for growth.

Diversification of Investor Base

A larger investor base improves market liquidity and stability. Non-traditional investors, such as retail investors and alternative asset managers are inclined toward corporate debt markets.

The emergence of exchange-traded Funds (ETFs) (focused on corporate bonds) facilitates access to these markets. In addition to that, institutional investors are also exploring emerging segments like private placements.

Digital Transformation of Bond Markets

Post-pandemic, the emergence of digital platforms and blockchain technologies has eased bond issuance, trading, and settlement.

The resultant greater efficiency and reduced costs attract more businesses to the debt markets. Digital platforms allow smaller companies to gain access to capital markets.

Development of Local Bond Markets

In order to reduce dependence on external financing, post-pandemic, many emerging nations have focused on building their domestic bond markets.

The governments and companies are collaborating to strengthen the infrastructure for issuing local debt.

Due to the increased availability of domestic currency bonds,exchange rate concerns were mitigated. Also, international investors looking for better returns are drawn to strengthened domestic markets.

CONCLUSION

The post-pandemic corporate debt market shows resilience, adaptation, and innovation in its evolution. Though the pandemic had caused initial shock waves through financial systems by creating liquidity shortages, a drastic rise in borrowing costs, and panic among investors, governments, central banks, and corporations made it a springboard for recovery. Now, corporate debt markets are stabilizing and transforming to new instruments, such as ESG bonds, private debt markets, and digital innovations. The post-pandemic corporate debt landscape presents ongoing challenges. Geopolitical tensions, regulatory changes, and the need for sustainable finance continue to shape corporate debt strategies. Investors are adopting a more judicious approach, emphasizing transparency, and ethical investment practices.

The post-pandemic landscape of corporate debt is rife with learning. It accentuates the importance of being financially nimble, taking strategic risks, and being able to pivot amidst uncertainty in the post-pandemic era. As the markets keep changing, the ability to adapt will be essential for both corporations and investors in keeping corporate debt a tool for improvement, not a burden.

References:

- Confronting the risks: corporate debt in the wake of the pandemic. (2023, June 26). Bruegel | the Brussels-based Economic Think Tank. https://www.bruegel.org/blog-post/confronting-risks-corporate-debt-wake-pandemic

- Abraham, F., Cortina, J. J., Schmukler, S. L., Development Economics, & Development Research Group. (2020). Growth of global corporate debt. In World Bank & Research Support Team, Policy Research Working Paper (No. 9394). https://documents1.worldbank.org/curated/en/570381599749598347/pdf/Growth-of-Global-Corporate-Debt-Main-Facts-and-Policy-Challenges.pdf

- Surti, J., & Goel, R. (n.d.). CHAPTER 5 Corporate Debt Market: Evolution, Prospects, and Policy. IMF eLibrary. https://doi.org/10.5089/9798400223525.071.CH005

- Wellons, P. A., Federal Financial Institutions Examination Council (FFIEC), Cline, W. R., Madrid, R. L., Dooley, M. P., Beek, D. C., Cohen, B. J., Grosse, R., & Goldberg, L. G. (1982). The LDC Debt Crisis. In History of the Eighties. https://www.fdic.gov/bank/historical/history/191_210.pdf

- Developing corporate bond markets in Asia, BIS papers no 26 https://www.bis.org/publ/bppdf/bispap26n.pdf

- Deghi, A., Seneviratne, D. and Tsuruga, T. (2021) Corporate funding and the COVID-19 CRISIS1, IMF eLibrary. Available at: https://www.elibrary.imf.org/view/journals/001/2021/086/article-A001-en.xml

- Growth of global corporate debt: Main facts and policy https://documents1.worldbank.org/curated/en/570381599749598347/pdf/Growth-of-Global-Corporate-Debt-Main-Facts-and-Policy-Challenges.pdf

- { indicator.label } (no date) IMF. Available at: https://www.imf.org/external/datamapper/NFC_LS@GDD/SWE

- Market data (no date) Climate Bonds Initiative. Available at: https://www.climatebonds.net/market/data/