Bollywood is often celebrated for its songs, stars, and spectacles, but behind the glitter lies a story of economics, finance, and survival. Fuelled by unregulated funds and high-risk borrowing, India’s film industry functioned in the background for many years. It entered the formal economy in 2000 after being granted “industry status,” attracting banks, corporations, and international studios. Since then, Bollywood’s operations have developed further, influenced by changing financing structures, the growing expenses of celebrity culture, and most recently, the digital revolution brought about by over-the-top (OTT) platforms. Following this journey demonstrates how Bollywood evolved from a clandestine gambling operation to a well-organised, internationally integrated business that reflects India’s broader economic narrative of risk, reform, and reinvention.

Evolution of Film Finance

Over the course of several decades, Bollywood’s film financing has experienced a significant transformation, evolving from a highly informal and risky model to one that is more structured and professional. The best way to comprehend this evolution is to examine particular instances that characterised each financial era.

The Era of Unorganized Finance and High Risk (1990s and Earlier)

For decades, Bollywood ran on money that never passed through banks. It was called an “underground business” for a reason. Films were funded by private moneylenders, many with underworld connections. Producers who were eager to start a movie had no choice but to accept interest rates that could rise to 60% annually.

Because the sector lacked “formal” status, banks refused to work with it. Rather, funds entered through unofficial means, frequently black money, making films an easy way to launder illicit funds. It was estimated that this method of financing accounted for almost 40% of all productions by the 1980s and 1990s. The majority of films, predictably, failed before they even broke even. The failure rate ranged from 80% to 90%.

The terms of borrowing were brutal. An Interest of 24-40% was often deducted upfront, and agreements rested on nothing more than trust. Financiers used “hundis”, handwritten IOUs that had no legal standing. If a financier decided to disappear, the filmmaker was simply left stranded.

The “star culture” was also fostered by the system. Famous people demanded outrageous fees, which were frequently partially paid in cash to avoid paying taxes. Filmmakers were forced to risk everything on box office success due to the inflated budgets. However, occasionally a low-budget gem made it through. Produced by T-Series, Mahesh Bhatt’s Aashiqui (1990) became a huge hit driven by its iconic music album rather than star power, demonstrating that quality content could cut through the chaos.

But the dangers of this unregulated world were always lurking. Even Amitabh Bachchan, after launching ABCL, sank into financial quicksand. By 1999, he was staring at debts of nearly ₹90 crore, a reminder that no one, not even Bollywood’s biggest star, was safe from the traps of unorganized finance.

The Formalization and Corporate Influx (2000s)

Everything changed with one stroke of policy. In 2000, the government finally gave the Indian film industry “industry status.” That meant banks like IDBI and ICICI could start lending at interest rates of 12-15%, a fraction of what shady financiers demanded. With that, corporatization entered Bollywood.

Suddenly, the business of making films began to look professional. Film funds and venture capital firms grew, and 100% FDI allowed foreign players to enter the market. To help Indian films attend international festivals and awards, the government even established the Film Promotion Fund, giving the industry a platform it had never had before.

Producers, too, began adopting practices that had long been standard in Hollywood. Subhash Ghai’s Mukta Arts introduced film insurance in 1998 with Taal, a safety net against delays and accidents. Yash Raj Films and Dharma Productions transformed themselves into corporate-style powerhouses, producing multiple films a year to spread risk. By 2007, YRF’s portfolio approach had paid off, and its revenues skyrocketed.

Global giants soon followed. Sony co-produced Sanjay Leela Bhansali’s Saawariya (2007), Warner Bros. jumped in with Chandni Chowk to China (2009), and Disney made the boldest move of all, buying 99% of UTV Motion Pictures in 2011. For a while, it seemed like Bollywood had truly gone global.

Indian movie-watching habits were changing at the same time due to the multiplex boom. Story-driven cinema was embraced by urban, upwardly mobile audiences, and smaller films eventually made it onto theatre screens. However, things changed by the late 2010s. Frustrated by disputes over intellectual property and the exorbitant fees of male superstars, Disney, Universal, and others started to retreat. Their departure created a void, but it also made room for new talent and voices.

The Digital Revolution and Modern Financial Models

The script has been altered once more in the past ten years. This time, the game-changing factor was streaming platforms rather than banks or multiplexes.

Before a movie even opens in theatres, selling the digital rights to JioCinema, Netflix, or Amazon Prime Video has become a surefire way to make money. For a lot of producers, it’s what keeps a project afloat financially. In order to secure returns during lockdown, Shoojit Sircar’s Gulabo Sitabo (2020) premiered on OTT instead of in theatres, further speeding things up.

Now, Bollywood works on a hybrid model. In addition to box office receipts, producers also receive revenue from digital sales, music deals, and satellite rights, all of which spread risk and protect them from possible failures. S.S. Rajamouli’s Baahubali series is one of the best examples of this in a movie. Pre-sales of digital, music, and satellite rights had already brought in hundreds of crores before it was even released. Theatres were reduced to a single piece of a larger financial puzzle.

Bollywood has transformed from a high-risk, cash-driven gamble to a well-organised, globally integrated company in a matter of decades. It is now driven by contracts, data, and strategy rather than handshakes and hundis.

Film Financing in Bollywood: Scripting a New Saga, Screening an Extravaganza

Bollywood is a spectacle-driven industry, but its core is finance, which is characterised by high risk, unregulated capital, and fluctuating revenue sources. Since Indian film financing has historically depended on private investors, family capital, and distributor advances rather than Hollywood’s organised system of completion bonds and guild-backed contracts, volatility has always been a part of the business.

Generally, a movie’s budget is divided into three categories: P&A (prints and advertising), below-the-line (production and technical costs), and above-the-line (star salaries, directors, and writers). Producers of star-driven projects are forced to make a high-risk wager on an actor’s box office success because above-the-line costs can account for 40–50% of total costs. Since opening weekend survival now depends on visibility, marketing expenditures have skyrocketed, occasionally matching production expenditures.

Though this stage is still underfunded in India when compared to the West, financing starts in development. Without doing much formal research, producers frequently make snap decisions based on instinct and star power. Funding for pre-production and production comes from a variety of sources, including distributor advances, small bank loans, pre-sales of music and satellite rights, and, more recently, corporate studios. By providing minimal guarantees that permit recovery before theatrical release, OTT platforms have introduced a new buffer.

The domestic box office used to be the biggest source of income, but its reliance has diminished. Bollywood is less susceptible to a single bad weekend thanks to producers’ diversification of risk through international releases, TV, streaming, and brand tie-ins.

Still, India lacks Hollywood-style financial safety nets, no completion bonds, little insurance, and limited institutional credit, leaving deals to hinge on trust, relationships, and market sentiment.

The Economic Impact of OTT Platforms on the Indian Film Industry

The Indian film industry has been entirely revolutionised by the unprecedented emergence of OTT (over-the-top) platforms such as Netflix, Amazon Prime, Hotstar, and more. These platforms have reshaped the economics of the Indian film industry by introducing new revenue models, diversifying investment flows, and creating opportunities for content creators and audiences alike, far removed from the near past when Indian films solely relied on theatrical box office success.

Traditionally, the box office collections of a film during its opening weekends were used to measure a film’s success; these earnings determined the recovery of investments for producers and distributors. Suffice to say that the Indian film Industry’s main source of revenue revolved around theatrical release. This model made films highly dependent on physical distribution networks, ticket sales, and the star power that could draw audiences to theaters. Given the rise of OTT platforms, this dependency has eroded. This practice of selling digital rights directly to OTT platforms for upfront payments directly benefits small to mid-budget films, which may otherwise struggle to find theatrical release. Furthermore, OTT release also safeguards investor interest against the unpredictability of cinema audiences. Geographical constraints have ceased to confine the viewership as films now reach millions of viewers across India and overseas.

OTT has provided viewers with an affordable, convenient, and accessible alternative to traditional cinema houses, fundamentally changing viewing. The COVID-19 pandemic accelerated the transition to OTT (given the theatre shut downs), pushing even the big budget titles to digital platforms. Entertainment has become more accessible owing to affordable internet and smartphones. OTT has stimulated inclusion of documentaries, independent cinema, regional cinema and experimental films, providing a richer diversity than theatres which usually catered to mass entertainers.

More often than not, nowadays, mid-budget films often skip cinemas altogether, leaving multiplexes to rely primarily on high-budget blockbusters like RRR, Pathaan, or Baahubali for profitmaking. This monumental shift in the entertainment landscape has been especially challenging for theatres and multiplexes which depend substantially on a steady stream of releases across various budgets. As OTT platforms demand quicker digital release, the length of the exclusive theatrical window has also shrunk from several weeks to just about four weeks or less. To entice audiences back to theaters, cinemas are focusing on offering premium experiences such as IMAX formats, recliner seats, and enhanced food packages.

One significant boon brought about by the rise in OTT would be its role in creating employment opportunities within the industry. Writers, directors, cinematographers and editors are highly sought after given the growing demand for web series, original films, and regional content. Furthermore, post-production services such as subtitling, dubbing, and VFX have also grown in importance. Regional actors and independent artists who previously struggled for visibility are increasingly finding recognition on digital platforms. According to Deloitte’s 2024 report, the combined film, television, and OTT sector supports over 2.64 million jobs directly and indirectly in India, demonstrating how streaming has become a significant job generator.

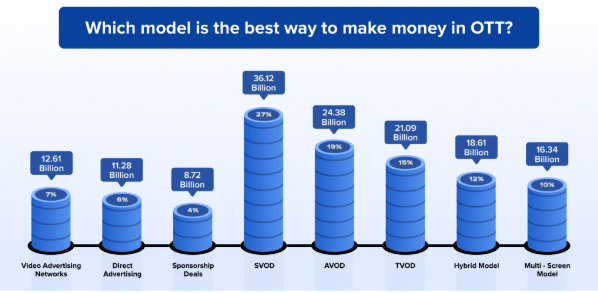

The revenue models of OTT platform operate primarily through two systems: SVOD (subscription video on demand) where users pay recurring fees for content and AVOD (advertising video on Demand) where content is either free or fee is negligible but supplemented with advertisements. These transformative revenue models provide flexibility, enabling platforms to target different market segments ranging from urban subscribers with greater purchasing power to price sensitive viewers who prefer add supported options. Many platforms also adopt hybrid models which combine both the systems, for e.g. Disney+ Hotstar and JioCinema allow users to choose between ad-supported free tiers and premium ad-free subscriptions.

OTT serves as a powerful risk mitigation tool for producers by allowing them to secure upfront payments from platforms even before release, often sufficient to recover production costs. Theatrical releases traditionally carried enormous risk: if a film fails to perform during its opening weekend, producers often incurred heavy losses. Despite limited commercial appeal, smaller budget or regional films now find a lucrative market online owing to the emergence of OTT. Effectively, the financial risk is transferred from the producer to the platform.

Production houses and streaming ventures are largely attracting private equity and venture capital as their role is expanding from merely acquiring finished films to now also directly financing original productions. The financing and investment landscape has also evolved, OTT platforms commission new projects, invest in regional cinema, and create exclusive libraries to differentiate themselves in the market. The industry is centring itself around selling engaging and unique stories hence making a swift change from star-driven entertainment where celebrity fees often inflate movie budgets to content driven entertainment. The surge in investment into regional films also reflects platforms’ strategies to cater to a linguistically and culturally diverse audience.

The Online Curated Content (OCC) sector is projected to show a nearly 14% annual growth through 2029, making it the fastest-growing segment in Indian media and entertainment. Foresight suggests that the Indian film industry appears to be pivoting into a hybrid distribution model with big blockbusters continuing to release in theaters first, maximizing box-office revenues before transitioning to digital platforms, smaller and mid-budget films, however, will increasingly prioritize OTT releases. Meanwhile, platforms will continue diversifying their revenue streams, combining subscription income, advertising, and co-production partnerships.

GULABO SITABO: A CASE STUDY

2020 saw the release of Shoojit Sircar’s Gulaabo Sitaabo exclusively on OTT, following theatre shutdowns due to the global pandemic. The film was sold to Amazon Prime for a whopping 65 crore rupees against its making budget of approximately 30 crore. Speculations suggest that even under a normal theatrical release, the film starring Amitabh Bachchan and Ayushmann Khurrana might not have matched this at the box office. By choosing OTT, the producers not only doubled their investment but also reached audiences in over 180 countries. This case proved that direct-to-digital releases could be more profitable and less risky than theatrical distribution.

To see the contrast between OTT and conventional models, it helps to examine their finance structures. Under conventional film finance, revenues arrived in an order beginning with box office collections, followed by satellite television rights, digital rights, and music rights. This model was quite reliant on opening weekend success and hence was extremely hit-dependent. Marketing expenses tended to consume almost half of production budgets, introducing additional risk. Financing typically originated in studio advances, bank loans, or presales to distributors. Financing was often secured through star power by producers.

Source:https://www.contus.com/blog/how-ott-platforms-earn-money/

In contrast, OTT platforms depend on recurring digital revenues. Their success financially is based on three important metrics: Customer Acquisition Cost (CAC), or the price of acquiring a new subscriber; Average Revenue Per User (ARPU), or the amount of revenue that each subscriber brings in on average; and the rate at which they churn, or the number of subscribers that will cancel within a specific time. OTT players spend heavily on premium content to reduce churn and increase ARPU, hoping that deep libraries will retain users over the long term. For the content producers, this approach is less volatile since platforms compensate them upfront for rights, thereby recovering their money, and the platforms absorb the long-term risk of retaining subscribers. OTT distribution costs are considerably less expensive as opposed to the hefty physical distribution costs in cinema halls.

In effect, traditional cinema economics are event-based and fleeting, subject to the capricious success of their theatrical runs. OTT economics, in contrast, are subscription-based and recurrent, with profitability defined through consistent audience interaction as opposed to fleeting ticket sales. This has enabled streaming services to redefine the fiscal framework of Indian entertainment.

Outside of sheer economics, OTT has also opened the global audience more democratically, opened up more freedom for creators, and diminished the hegemony of conventional star power. Though theatres will always have a place for big-screen events, the wider economic and cultural path of Indian film is more digital by the day. OTT has reshaped not just the manner in which films are distributed and consumed, but also the manner in which films are funded, made, and kept as enterprises in an ever-changing entertainment economy.

CONCLUSION

Bollywood’s transition suggests a sea change in the economic perspective: from a fragmented, high-risk sector reliant on informal and often opaque financing to a more organized, corporate, and financially responsible one. Gaining “industry status” in 2000 marked a turning point as it allowed film production companies access to institutional credit, formal investment options and insurance, significantly reducing financial uncertainty. Corporate funding and strategic partnerships have ushered in a new era of accountability, transparency, and data-backed decisions in film financing. Before this shift, the industry depended greatly on personal connections. Recently, OTT platforms have changed Bollywood’s financial landscape by providing upfront payments and more reliable revenue sources, reducing reliance on box office sales thereby encouraging small and medium-budget productions. This mixed approach to releasing films has not only created diverse income streams from subscriptions, licensing, and advertising, but it has also improved revenue recovery while reducing risks.

In summation, these changes are reflective of Bollywood’s embracement of global practices of financing, digital monetization, and long-term value creation rather than short-term profit maximization, making the industry more resilient. In the broader sense, this transformation is a component of India’s transition towards innovation-driven economic growth.

References:

- Mantha, C., & Rao, P. (2025, May). Economic impact of the film, television, and online curated content (OCC) industry in India, 2024 [Report]. Deloitte India & Motion Picture Association. https://www.deloitte.com/content/dam/assets-zone1/in/en/docs/industries/technology-media-telecommunications/2025/in-tmt-mpa-deloitte-ecr-report.pdf

- [Author n.d.]. Cinematic evolution of film financing in India. Areness – Law & Beyond. https://www.arenesslaw.com/cinematic-evolution-of-film-financing-in-india/ arenesslaw.com

- Oak, A. P. (June, 2023). Film financing and the digital market: future, challenges & hybrid models. ShodhKosh: Journal of Visual and Performing Arts, 4 (1). https://www.granthaalayahpublication.org/Arts-Journal/ShodhKosh/article/download/3822/3443/21677

- Hashim, Hasrul & Zhongyu, Zhao. (2025, June 30). The Economic and Cultural Impacts of OTT Platforms on the Film Industry: A Systematic Literature Review. Jurnal Komunikasi: Malaysian Journal of Communication. ResearchGate Study https://www.researchgate.net/publication/393337062_The_Economic_and_Cultural_Impacts_of_OTT_Platforms_on_the_Film_Industry_A_Systematic_Literature_Review

- Lata Jha, (2020, June 24). Small films, big profits as makers rake in moolah from streaming platforms. Mint https://www.livemint.com/news/india/small-films-big-profits-as-makers-rake-in-moolah-from-streaming-platforms-11592985824640.html

- (2025, September 9). Unpacking entertainment rights in India: Copyright, monetization and regulation. Company360. https://company360.in/blog/unpacking-entertainment-rights-in-india-copyright-monetization-and-regulation/

- Streaming revolution: The rise of OTT platforms in India. (2024, May). TIJER – International Research Journal. https://tijer.org/TIJER/papers/TIJER2405165.pdf

- Cross, M. S. (2019, November 27). How Bollywood Went Underground | The Juggernaut. The Juggernaut. https://www.jgnt.co/how-bollywood-went-underground

- Raghavendra, S. V. &. N. (2006, August 19). Bollywood rakes it in with some help. The Economic Times. https://economictimes.indiatimes.com/bollywood-rakes-it-in-with-some-help/articleshow/1908443.cms

- Wardani, C. K. R. (n.d.). A Bollywood affair. Scribd. https://www.scribd.com/document/517918137/A-Bollywood-Affair

- https://www.cambridgescholars.com/resources/pdfs/978-1-5275-7602-5-sample.pdf

- Admin. (2023, September 12). Cinematic evolution of film financing in India. Areness – Law & Beyond. https://www.arenesslaw.com/cinematic-evolution-of-film-financing-in-india/

- Stage 32 – Stage 32. (n.d.). Stage 32. https://www.stage32.com/blog/film-funding-the-independent-producer-and-the-ppmllc-2854

- Johansen, M. (2025, March 19). Entertainment finance. OneMoneyWay. https://onemoneyway.com/en/blog/entertainment-finance/

- Iamgaurava. (n.d.). Film financing in Bollywood. Scribd. https://www.scribd.com/document/123292447/Film-Financing-in-Bollywood