INTRODUCTION

Microcredit is defined as a relatively small loan, primarily given out to low-income customers to meet short term expenses. It often serves as a quick and reliable source of credit as it doesn’t require any prerequisites like credit ratings. It has existed since the advent of the monetary system. This included most informal forms of credit like family grants/loans and moneylenders. But ‘formal’ microcredit was, by academic consensus, established in the 18th century by Irish author Jonathan Swift, who gave small interest free loans to struggling traders and merchants. After this, regulated microcredit was officially started across Europe and the Americas during the late 19th and 20th century. Microcredit systems like payday lenders have existed since the late 1980s, predominantly in developing or under developed cities and towns. Coming on to Asia, this system was revolutionized by Mohammad Yunus in Bangladesh with the development of the Grameen Bank, a low income borrower network which focused on interest free loans and peer accountability.

BNPL or Buy Now Pay Later is a contemporary extension of payday loans and microcredit as a large, it functions similar to a credit card, with the key difference of splitting the initial payment into terms, generally 4, which are to be paid in the following weeks, with interest and late fees payable on failing to pay for any term.

WHERE THE MONEY COMES FROM

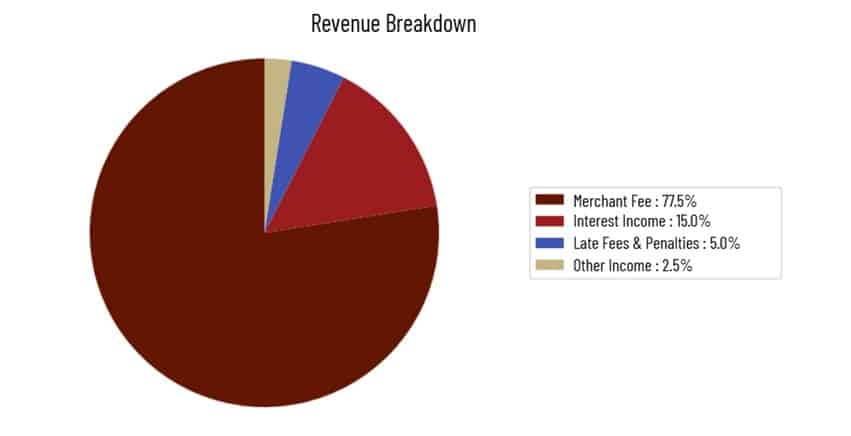

BNPL companies like Affirm and Klarna work as intermediaries. They shift the burden of payment on themselves, and the amount is collected from the consumer within the designated payment window. Even though interest and fees offer higher APR’s as compared to credit cards, their main source of income, contrary to popular belief, are the merchant fees, for example, 57% of Klarna’s revenue was from merchant fees.

Though to a lesser extent, interest rates, late fees and penalties also impact the revenue of this industry. It has also been seen that some companies increase interest rates for longer term ‘loans’. Along with this, brand partnerships also help as these platforms help with advertisement.

INDUSTRY CONCERNS

This industry as a whole has seen significant growth from primarily 2019. Gross Transaction Volume in 2019 was $25 Billion which has grown to approximately $225 Billion in 2025. Klarna itself has seen a GTV of $100 Billion this year.

But high transaction value does not always mean the company has coherent internal functions, Recent events have brought Klarna’s credit management issues to light, causing a $30 Billion loss in its valuation. Debt financing costs rose to $130 million for both Q1 and Q2 2025. But steps are being taken throughout the industry to rectify this problem. Many companies have entered forward flowing agreements to sell customer loan receivables, companies like Nelnet have agreed to buy loan receivables from the top BNPL companies. Also since most of these companies have banking licenses they collect customer deposits, and most of their loans are funded via fixed deposits. Along with this, many other initiatives and systems are in place to reach sustainable levels of debt financing expenses by FY 2026.

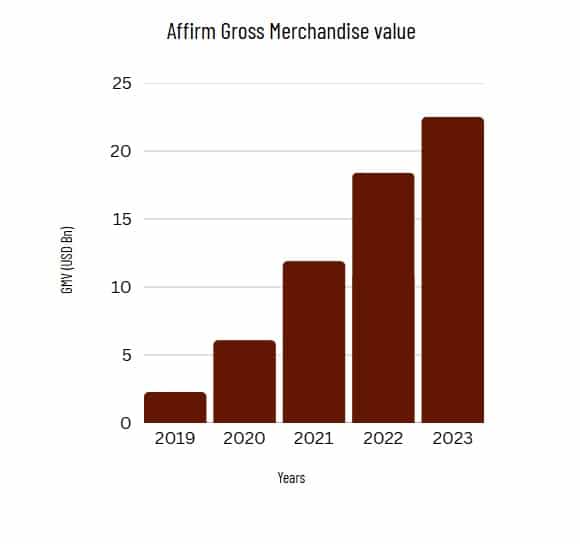

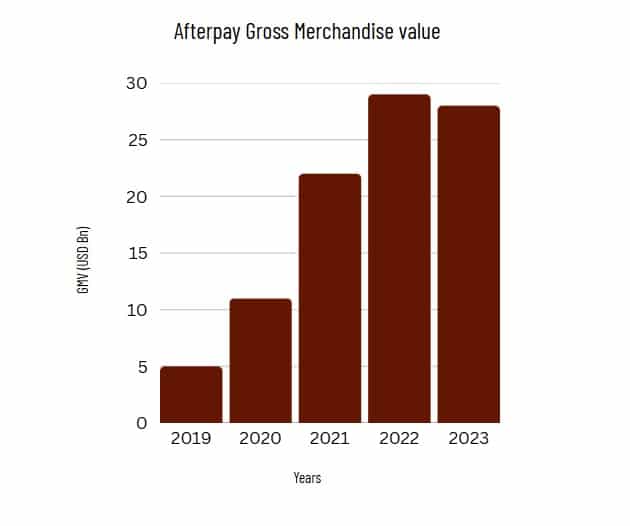

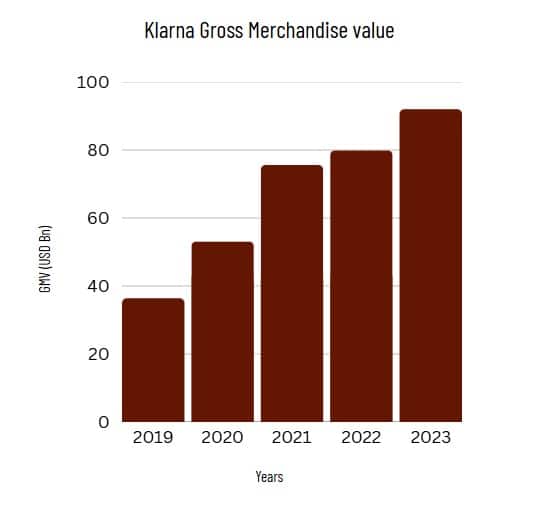

Financial statements of the top 3 BNPL companies (Klarna, Afterpay, Affirm) show promising future outlooks. The figures below show sectoral growth in terms of GMV from 2019 to 2023.

Along with this the projected GMV figures for 2026 are $115 Billion for Klarna, $38 Billion for After pay and $25 Billion for Affirm. For this to be achieved, the industry has started focusing on strengthening risk control systems and expanding merchant/consumer bases. Investment in AI driven internal credit ratings has already started in hopes of regulating their user base.

The growth of Buy Now Pay Later (BNPL) has had a great effect on Access to Credit for consumers, especially consumers who have a limited or poor credit history. However, the ease of obtaining a BNPL transaction and limited credit checks involved in the BNPL process can create a greater risk of consumers being over-indebted, purchasing on impulse, and creating additional financial stress on vulnerable consumers. As discussed earlier, BNPL provides profits to providers mainly through merchant fees, however BNPL users may end up being charged excessive late fees and/or interest if the BNPL payment is not made. With such rapid growth in BNPL usage and the increased calls for regulatory oversight to provide a balanced approach between innovation and consumer protection, BNPL companies are required to provide clear and concise terms and conditions and utilize Sustainable Lending Practices. Thus, BNPL has been able to transform the Consumer Credit Industry by providing new opportunities and potential caution, while also changing the way consumers spend and ultimately affecting the financial health of society.

REGULATIONS AND GOVERNMENTAL SANCTIONS

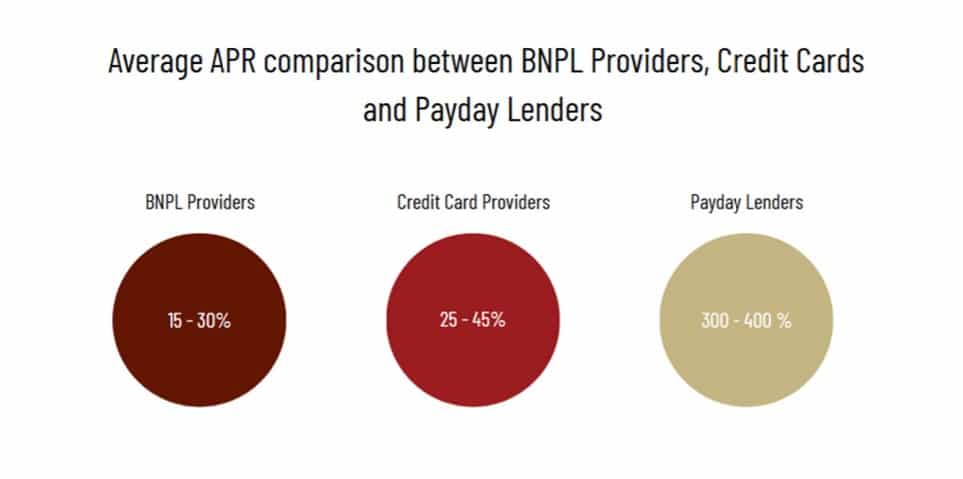

Throughout its existence, microcredit has always existed in a financial grey space due to it not being regulated by any actual institution. Since no actual credit or background checks are made for borrowers, these provide a short term financial source for potential illegal activities. Since BNPL is a product targeted mostly towards people living paycheck to paycheck, these companies charge extremely high APR’s as compared to traditional loans. This practice has caused a lot of criticism for this industry in recent times as industry professionals have called for significant regulatory changes to the industry.

In lieu of this the CFPB (Central Financial Protection Bureau) has implemented some strict directives which include providing BNPL users with the same federal protections as credit card users, which include rights regarding refunds, investigations into merchant disputes and disclosure of all fees during final billing. Sebastian Siemiatkowski, CEO and co-founder of Klarna said “We welcome these changes that the CFPB suggested because they are basically good standards that anyone lending money money should apply, in our opinion, about making sure there’s good consumer protection.” It is important that BNPL products are regulated from the customer, but also from the lender’s side to remove any issues in the lending process. BIll Ready, CEO Affirm stated “BNPL’s growth has outpaced regulatory adaptations, but upcoming standards will balance consumer protection with finance innovation.”

CONCLUSION

In conclusion, BNPL’s rise shows the infectiousness of microcredit. Credit is extremely important for any economy to progress and BNPL helps people who otherwise are not given any credit to contribute positively to it. But at the same time proper management needs to be present to avoid exploitation for the borrowers and implementation of all systems in place for federal control for this industry to achieve its full potential.

SOURCES

- https://externalcontent.blob.core.windows.net/pdfs/WellsFargoSpecial20231204.pdf

- https://www.richmondfed.org/publications/research/economic_brief/2025/eb_25-03

- https://www.afm.nl/~/profmedia/files/rapporten/2025/rapport-marketupdate-bnpl-2025-eng.pdf

- https://www.globenewswire.com/news-release/2024/07/30/2920797/0/en/Global-Buy-Now-Pay-Later-Markets-Report-2024-US-has-the-Largest-BNPL-Market-by-Value-China-is-the-Largest-Market-by-Volume-Sweden-has-the-Highest-BNPL-Penetration-Rate-Forecast-to-.html

- https://www.morganstanley.com/insights/articles/buy-now-pay-later-trends-2025

- https://www.sciencedirect.com/science/article/pii/S2214635023000023

- https://economictimes.indiatimes.com/wealth/spend/credit-cards-vs-bnpl-in-india-which-is-better-for-you-in-2025/credit-cards-pros-amp-cons/slideshow/124108599.cms

- https://www.paymentsjournal.com/nevada-tightens-rules-around-bnpl/

- https://www.nortonrosefulbright.com/en/knowledge/publications/cc8b4fd0/cfpb-takes-steps-to-regulate-buy-now-pay-later-providers

- screener.in